The business cycle and credit, defaults, and bankruptcies

I want to put a little more meat on the bones regarding the section of yesterday’s post on credit, defaults and bankruptcies with some numbers. I would contend that credit cycles lead garden-variety business cycle turns. So, absent a Black Swan event like this pandemic and the lockdowns, we should expect to see recession-inducing financial distress in the credit space before the cycle turns down.

Sequencing recovery versus a double dip

And I think the sequencing and terminology here is important because of the nature of this latest downturn. I am looking at any renewed contraction in GDP and recession as part of a double dip rather than part of a single recession.

The National Bureau of Economic Research’s recession dating committee had this to say about the recession caused by the pandemic:

in the case of the February 2020 peak in economic activity, the committee concluded that the subsequent drop in activity had been so great and so widely diffused throughout the economy that, even if it proved to be quite brief, the downturn should be classified as a recession.

What they are saying is that this pandemic recession was so deep and dispersed, they had to call it a recession even if it ended up being brief in duration.

By extension then, the uptick in GDP growth we saw with the re-opening in the US was similar. They could easily write something like this: “in the case of the June 2020 trough in economic activity, the committee concluded that the subsequent rebound in activity had been so great and so widely diffused throughout the economy that, even if it proved to be quite brief, the upturn should be classified as a recovery”. That perfectly mirrors their recession dating statement and is an accurate reflection of what has occurred.

So, the sequencing is recession in February to recovery in June-ish followed by expansion for an unknown number of months through the present and beyond. If we were to see a downturn induced by a Fall winter coronavirus wave and a lack of fiscal support., the cause of any renewed drop in GDP would be separate and distinct from the first.

The first drop, which predates the lockdown was the result of consumption declines that began as supply chains unravelled and consumers pulled back as the virus took a foothold in the US. A second GDP decline would be due to a separate coronavirus wave and and the attendant policy responses and/or a new and distinct consumption, production, staffing decline due to a lack of policy response or the distinct pandemic wave.

Credit as canary in the coalmine

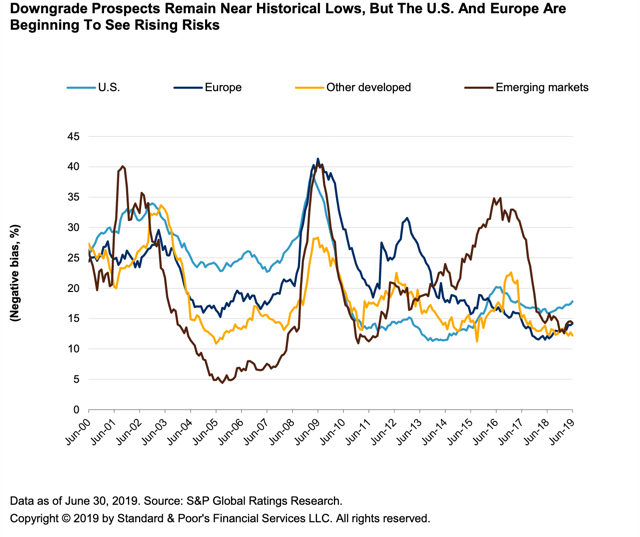

The reason this sequencing makes sense and has to be set out is the credit cycle. In past recessions, credit has deteriorated before the onset of recession. And so, the deterioration of credit conditions was a harbinger of recession. Take a look at the chart from S&P Global below. It shows the global credit cycle from 2000 through 2019.

If you follow the blue line for the US, you can see the downgrade wave rising ahead of the March 2001 recession begin and the December 2007 recession begin as well. The credit deterioration from 2014 to 2016 was associated with the shale oil bust and was localized enough to the oil patch that it ended only in a mid-cycle slowdown rather than a recession. Otherwise, a prodigious uptick in downgrades leads business cycles down.

I would expect the same to be true here again. But credit conditions are already deteriorating because of the first wave. And all we need is an extra nudge for that to metastasize into something worse. So we can look at actual defaults and credit spreads for clues regarding the cycle instead.

The K-shaped credit cycle

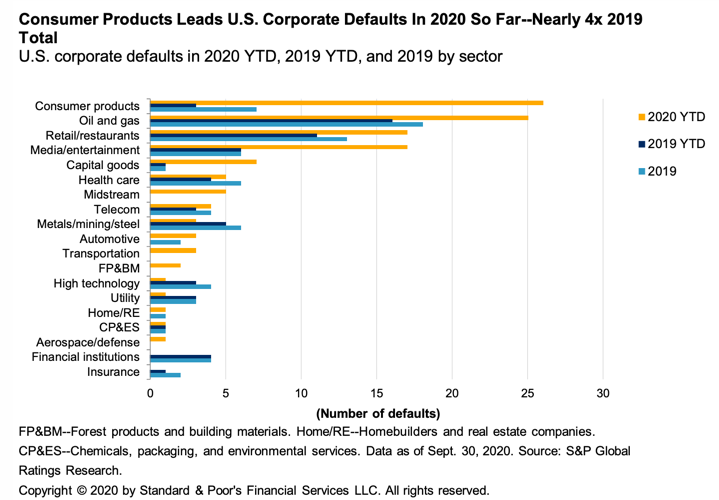

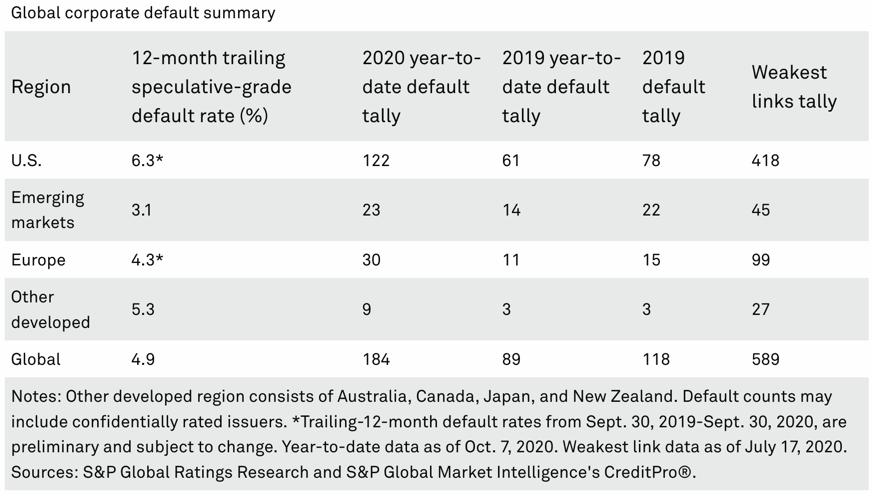

One hypothesis I am working with is the concept that a recession can be gleaned from a K-shaped credit cycle devolving into a generalized deterioration of credit. Take a look at the following two charts, for example.

S&P Global notes two things based on these:

- “The U.S. leads the global default tally with 122, followed by Europe with 30.”

- “About 70% of the U.S. corporate defaults belong to just four sectors: consumer products (26), oil and gas (25), retail and restaurants (17), and media and entertainment (17).”

Translation: the US is a credit laggard. And I suspect this is largely due to the policy response. Europe has kept companies alive with government largess more than the US has. What impact this eventually has on growth differentials isn’t clear to me. But to the degree the same policy responses continue in a Fall/Winter wave, we should expect credit conditions in the US to be worse than in Europe and for this to make the US susceptible to recession.

Another point here is that some sectors are getting absolutely decimated by the pandemic while others are escaping relatively unscathed. Tesla, for example, is on the verge of an investment grade credit rating after flirting with a liquidity crisis due to convertible bonds maturing a few years ago. I would call this a K-shaped outcome. And to the degree the K-shaped outcome converges into a more generalized broad-based deterioration of credit, I would see this as a harbinger of recession.

My view

JPMorgan Chase CEO Jamie Dimon made the following forward-looking statements yesterday after his company released earnings:

- Compared to the first quarter, our reserve build now assumes a more protracted downturn … as we prepare and reserve for something worse than our base case.

- You will see the effect of this recession. You’re just not going to see it right away because of all the stimulus.

What he’s telling you is that JPMorgan Chase is basing estimates for future loan losses on a scenario that has much more downside than the Federal Reserve’s present base case.

What do they know that the Fed doesn’t? They crushed their earnings estimates. And they took a fifth of the anticipated loan loss provisions for this quarter. Yet, they see trouble ahead. From his earnings call statements, I think he’s very much in the camp I am in i.e. sanguine about the near term but concerned about future trends. Dimon said that the only thing holding the economy up had been stimulus and this began to roll off in August. And yet more is due to roll off as we reach year end.

So, right now, the overall credit picture is not that bad. Yes, defaults will spike. But that’s an expected outgrowth of the pandemic. It’s limited to four industry sectors and is mostly priced in. There are plenty of scenarios where that pain remains localized and the K-shaped recovery continues both at the corporate and household level. However, downside credit risk is especially elevated in the US. And to the degree the K-shaped outcome becomes more generalized, we should take that as a sign of increased risk of a double-dip recession.

Comments are closed.