David Rosenberg and the corona crisis as a depression

I know everyone is still talking about President Trump’s contracting coronavirus. But I want to talk about the virus from a different, more economic lens. That’s because I was talking to the excellent David Rosenberg last week about the economic situation that the coronavirus has created. And this video was released on the Real Vision platform today (link here). The video’s title ended up being “David Rosenberg – In A Depression, Own What’s Scarce”. And in the end, it’s that word ‘depression’ which caught my attention. So I want to talk about it.

Framing

Here are the three themes Dave’s analysis brings to the fore:

- Are we in a depression?

- Irrespective, how do you do macro policy now?

- Again irrespective, how do you invest now?

And again, the word ‘depression’ is what stands out here. And that’s because a depression is not the same thing as a recession; it has a more lasting psychological and economic impact. It’s literally life-changing for millions of people.

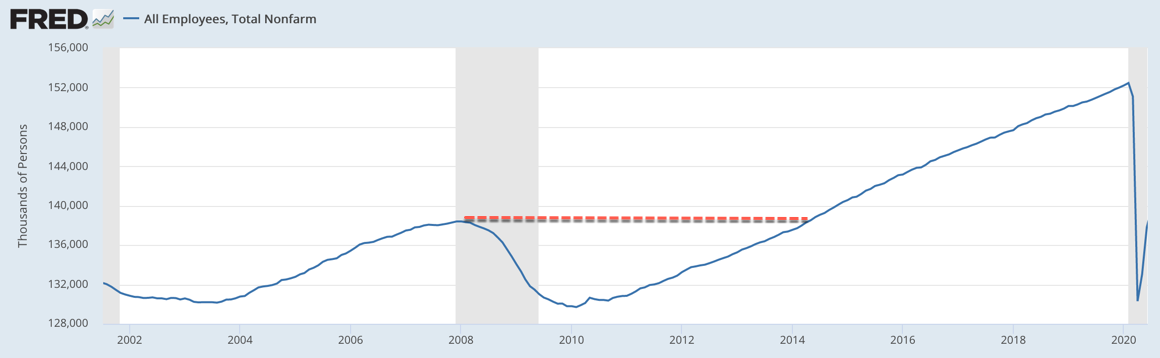

Now, one could argue that the Great Financial Crisis ushered in a ‘depression’ with a small d. And the depression-like nature of that outcome is what led to Trump. But, if that narrative is true, it’s only just barely true. When I gave you my take on the three d’s of depression back at the end of April, what I said is that it was the duration of a depression more than depth or diffusion that made it a different beast. Look at jobs, for example.

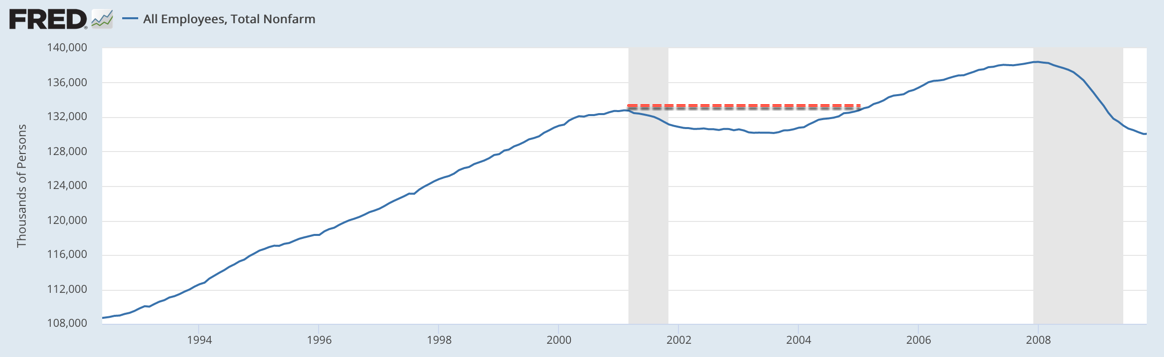

If we look at peak to trough to re-gaining peak from 2008 forward, we’re talking about 6 years. That’s a long time. But actually, it’s not that much longer than the equivalent period from 2001 to 2005.

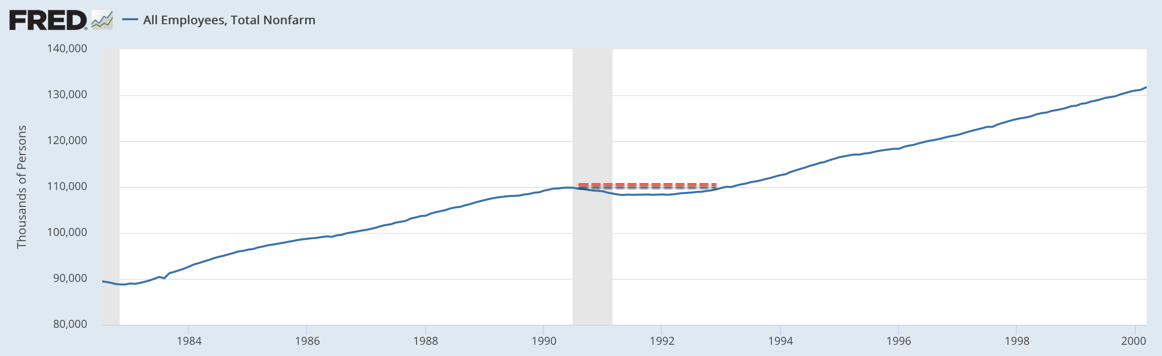

I would point out that it is double the length of recovery of jobs from 1990 to 1993.

So, what you see with the Great Financial Crisis, then is a more meaningful loss of employment than the previous recession which itself saw a more meaningful loss of employment than the recession before it, a time in the US marked by the first ‘jobless recovery’.

The pandemic depression

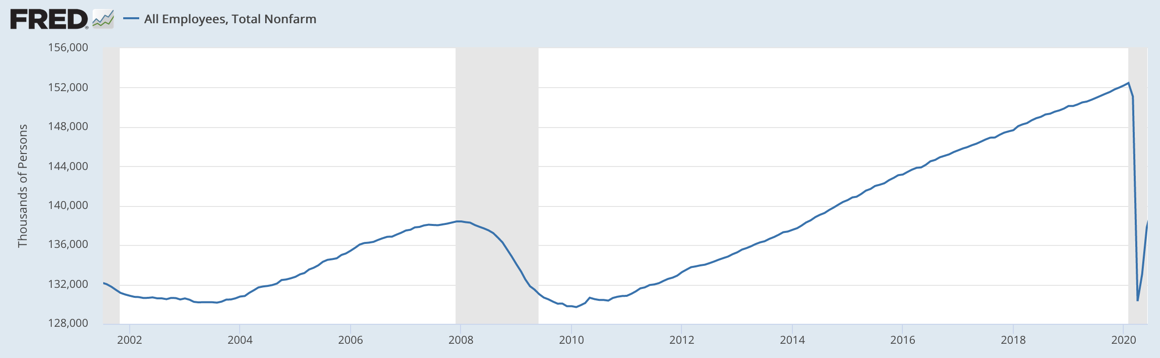

So, look at the area highlighted in grey at the end of that first chart again.

The falloff in jobs is severe and abrupt – like nothing we’ve ever seen before. And while we got a snapback, that snapback was less than half of the original loss. So the question now goes to how long it takes for the remaining jobs to be recouped.

Here’s Dion Rabouin of Axios:

The number of people considered long-term unemployed has made a worrying bounce in recent months, as Friday’s jobs report showed 3.8 million people had lost their jobs permanently in September.

Why it matters: That’s almost twice as many as at the height of the pandemic in April.

What’s happening: When the first waves of layoffs hit in March and April, most of the newly unemployed believed their job losses would be temporary (nearly eight in 10, according to the April nonfarm payrolls report) and reported they were not looking for work.

- The flood of Americans who had just been laid off pushed the percentage of people who had been unemployed for at least 27 weeks to 4.1%, the lowest the rate has been since December 1953.

- But as the pandemic has raged on and the economy has begun to unravel, more people have been sitting on the sidelines for longer.

- Even with an additional 11 million people unemployed than in February, the percentage of unemployed people who have been without a job for more than six months returned to the same level it was at in February.

He thinks many of these unemployed will hit the wall when pandemic assistance programs expire at the end of the year.

I would go one further though. Do we know that the existing snapback is durable? Is the existing job gain going to last? We continue to see high layoff numbers, most recently with Regal Cinemas closing again and Disney laying off 28,000. A second wave of job loss could mean the existing job gains are partially reversed. And even so, we’re still talking about going from 141.7 million to 152.5 million non-farm payrolls. That’s almost 11 million jobs.

If we can recoup an average of 250,000 jobs for 44 straight months, we can get there. But let’s remember that we went from 138.4 million jobs in January 2008 down to 129.7 million and back in 6 years. Even after a snapback, we have even further to go in this cycle. So I don’t see the 44-month outcome as a base case. So, David Rosenberg is right to call this a depression.

Austerity in the UK

I saw the Chancellor of the Exchequer talking about their economic crisis today. And his focus was on fiscal responsibility. It almost sounded like austerity.

“We have a sacred responsibility to future generations to leave the public finances strong, and through careful management of our economy, this Conservative government will always balance the books.”

What does that mean? Is Sunak suggesting the UK will raise taxes and cut outlays even as the second wave of infections hits the UK? I don’t see that working anymore than it worked in Greece as they tried to meet the Troika’s demands during the sovereign debt crisis.

Goldman Sachs thinks that a ‘blue wave’ in the US – where the Democrats sweep the Oval Office and both houses of Congress – leads to the opposite outcome, massive deficit spending. And while they aren’t sure what this means for shares because of tax policies, they think it means great things for the economy.

Would a Trump win mean big deficits too though? And how helpful would those deficits be? I think a Trump win means deficits but not ones that are geared toward the middle and working classes because we have already seen that his supply-side economic policies are geared toward the wealthy and corporates. And even these policies would be meagre because of a Democratic House of Representatives. So, only Congress and the White House in one party is likely to mean anything regarding deficit spending going to people who desperately need economic relief and are, therefore, likely to spend.

My view: in an economic depression with tens of millions out of work in the US and tens of millions in need in Europe and a deadly virus still circulating widely, you don’t want to move toward austerity. You want to offer a social safety net that encourages people to make decisions based on what’s best for their health rather than what’s best to avoid destitution. Focussing on cutting back means more people will choose to risk working while infected or sending kids to school while infected simply to make ends meet.

But, of course, what I think ‘should be’ isn’t the issue. The question goes to what’s likely to happen.

Investing for secular stagnation

As for investing, the biggest macro variable is the weak growth environment. That’s because it means both ultra-loose monetary policy and low, low growth. Effectively, that’s the worst of both worlds for an investor because you get less capital gains from bonds already near zero yield, you get no income from bonds near zero yield, and you get no return from shares when nominal growth rates are weak. What do you do?

David Rosenberg thinks you should get long duration by moving to the long bond, 30-year Treasuries. And if you are brave, take the Gary Shilling route via 30-year Treasury strips, effectively zero coupon bonds with a duration of 30 years. Only then can you get yield pickup with no default risk. If you go out the risk curve you face default risk. Here, you face interest rate risk. Pick your poison.

On the equities side of things, you want growth. And that means you shun value. Why? Because unless you choose the right value stocks, you get no top line growth. And no top line growth, mean no earnings, which means no capital gains unless you expect P/E ratios to go even higher than they already are.

My View

None of this is very upbeat. And if you want my view, I agree with David Rosenberg. This is a depression. Before it is over, it will have a long-reaching impact on our psyche and our economy. Hopefully, that doesn’t lead to military confrontation as the shrinking pie syndrome pits people and nations against one another.

The US election and the inauguration are the biggest near-term hurdles here due to a fractious political climate. If Trump wins, he will almost certainly face divided government in some form. And that means gridlock in the midst of a depression. Economically, that’s not a good outcome. It might be good for long bonds and for the growthiest of growth stocks. But, if we get another recession, more downside risk will materialize.

If Biden wins and the Senate is Republican, we get the exact same outcome, gridlock. Only in the ‘blue wave’ scenario do we see a situation where US politicians will implement one specific economic agenda. And so, we will have to see what that agenda is and whether it leads to positive economic and market outcomes.

My sense is it can do. But now is not the time to make that judgment. And what that means for investing certainly depends on the regulatory environment, taxes and inflation. But, as I see it, the blue wave is the only outcome that avoids gridlock. And so, it is the only outcome that has any chance at creating a positive economic outlook.

Overall then, David Rosenberg is right. Your baseline has to be that this is a depression (with a small ‘d’ for now). It can get worse. But it can also get better.

Comments are closed.