No stimulus, no problem?

The calls for fiscal relief by the Federal Reserve have apparently fallen on deaf ears, as US President Trump pulled out of negotiations for a stimulus package last night. Asset markets were all over the place as investors digested the news. But, there doesn’t seem to be a sharp reaction quite yet.

I don’t think the lack of fiscal stimulus in the US is a death knell for the recovery. If we don’t get fiscal relief, there will be some serious downward revisions to Q4 2020 GDP. But there are a lot of moving parts here. So, below, let me break down how I’m thinking about this.

Tactics

When you look at the numbers being bandied about for fiscal packages today, you hear about numbers three times as large as the stimulus that Barack Obama signed off on after the Great Financial Crisis. And if you recall, back then there was a lot of debate about sizing with the likes of Christine Romer, who argued for a larger package losing out to those like Larry Summers, who thought a larger fiscal package was a non-starter politically.

I think we need to remember this because, while the situation today is even more urgent than it was back then, there are still political limits to how much deficit spending one can undertake. The Democrats are willing to go for massive fiscal relief now because of the pandemic. But, my understanding is that both Nancy Pelosi and Joe Biden are fiscally conservative.

Pelosi believes in Paygo, a rule where any new spending proposals by the House of Representatives must be offset either by tax increases or budget cuts. And Biden has talked about ‘paying for’ fiscal programs via tax hikes on corporations and the rich. So, in the eyes of establishment Democrats leading their party, this spending is necessary, temporary, and will likely later be partially offset by tax hikes or spending cuts.

On the Republican side, you have to ask yourself whether you have the votes for more deficit spending. Mitch McConnell has a lot of fiscal hawks to contend with in his ranks. And, likely, he has told Trump that he can’t get a fat fiscal package like the one the Democratic-led House of Representatives has recommended through the Senate.

So, Trump simply pulled out of talks. It’s a negotiating tactic, not necessarily a hard and fast position. Will it have an impact though? It’s hard to say because so many variables are at play with the US election on our doorstep and Covid-19 very much on everyone’s minds. But, as I have stressed repeatedly over the past few months, outcomes without fiscal relief for the US are reasonable worst case scenarios if not base case outcomes.

Economic situation

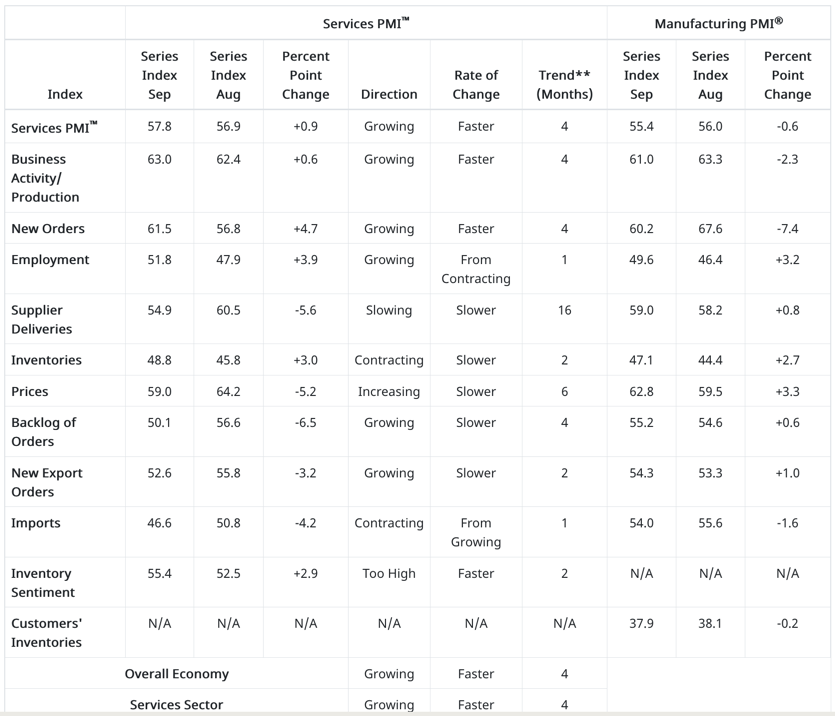

From an economic pre-condition perspective, we are still in an acceleration phase. While many aspects of the jobs picture and the manufacturing rebound have cooled significantly, there is still a decent amount of follow-through in the services sector overall. Monday’s Services PMI from ISM for September was well above expectations for 61.0 at 63.0. And this was above the 62.4 month-prior reading for August.

Significantly, production, new orders and employment sub0indices were all gathering steam.

So, I would say that we are in a relatively good place overall. But, there are already signs of deceleration that suggest the recovery is not 100% self-sustaining. I would go so far as to say a negative print for Q4 GDP is a reasonable worst case scenario. At a minimum, we will see GDP growth forecasts ratchet down from here.

What we need to remember is that the $600 per month weekly checks for the unemployed are long gone. And Pandemic Unemployment Assistance expires at the end of the year. There is a very large fiscal cliff on December 31, then. And that means that the US risks another recession as a reasonable worst case scenario.

K-shaped economic diffusion

The reason to focus on downside risk here has to do with the K-shaped economic outcome matrix, where some households and businesses are doing better than ever. And others are getting absolutely crushed by Covid-19.

For example, Axios’ Dion Rabouin reported the following this morning:

A new survey from Alignable finds that many small businesses are growing more worried about “a severe cash crunch,” with 42% saying they could collapse by the end of the fourth quarter…

[…]

…analysts at S&P Global say… “negative outlooks are at historical highs both for nonfinancial corporates (37%) and banks (30%) globally, pointing to more rating actions ahead.”

- “Since the outbreak of the pandemic, credits at the lower end of the scale (‘B’ and below) have represented over half of the downgrades, while 90% of defaults were from credits in the ‘CCC’ category.”

- “We forecast the speculative-grade corporate default rate to double by June 2021, from the current 6.2%, to 12.5% in the U.S. and from 3.8% to 8.5% in Europe.”

So, the FAANG stocks might be doing well, and corporate lawyers are doing well too. But, a lot of businesses are just hanging on. And a bad Covid-19 fall and winter combined with a lack of fiscal relief will be the end for them. Liquidation, not Chapter 11 bankruptcy is what we should expect in many cases.

This will hit retail and commercial real estate especially hard. Axios mentioned New York in that vein today, saying “only 12% of New Yorkers have returned, according to the latest numbers from commercial real estate firm CBRE, which manages 20 million square feet of office space in the city.”

Interestingly, they also say that,”in the city’s suburbs, return-to-work rates are around 33%, per CBRE.”

My View

So, the K-shaped recovery is a real and present danger to the economy. Aggregates mask serious pain and financial weakness in many different important sectors of the economy and in different regions of the country in the US. Moreover, without support at the federal level, states and municipalities will be in a world of hurt. And households will be made to feel this pain via job and service cuts or tax hikes.

I also see the fall and winter as a time where the US needs to prevent people from making an ‘economic health or physical health’ tradeoff because the coronavirus has been shown to be especially virulent when temperatures are lower and people are indoors. What that means is that we are likely to see a large coronavirus wave in the near future. And this wave will be exacerbated by people choosing economic health over physical health because of the severity of the economic crisis in a K-shaped recovery without fiscal relief.

Do not be caught unawares. This is what’s coming. And the question now is not whether the lack of fiscal support causes the US economy to downshift. The question is how much downshifting we do and whether that shift means the economy rolls over into recession. The reasons are clear: sub-aggregate level data show significant cliff-edge economic distress. And a lack of fiscal relief in a situation where we should expect the public health crisis to spike will send many businesses and households over the edge, while the public health problem will freeze consumer spending.

It doesn’t have to be this way. But, likely, it will be this way.

Comments are closed.