Continued high jobless claims, no stimulus and coronavirus

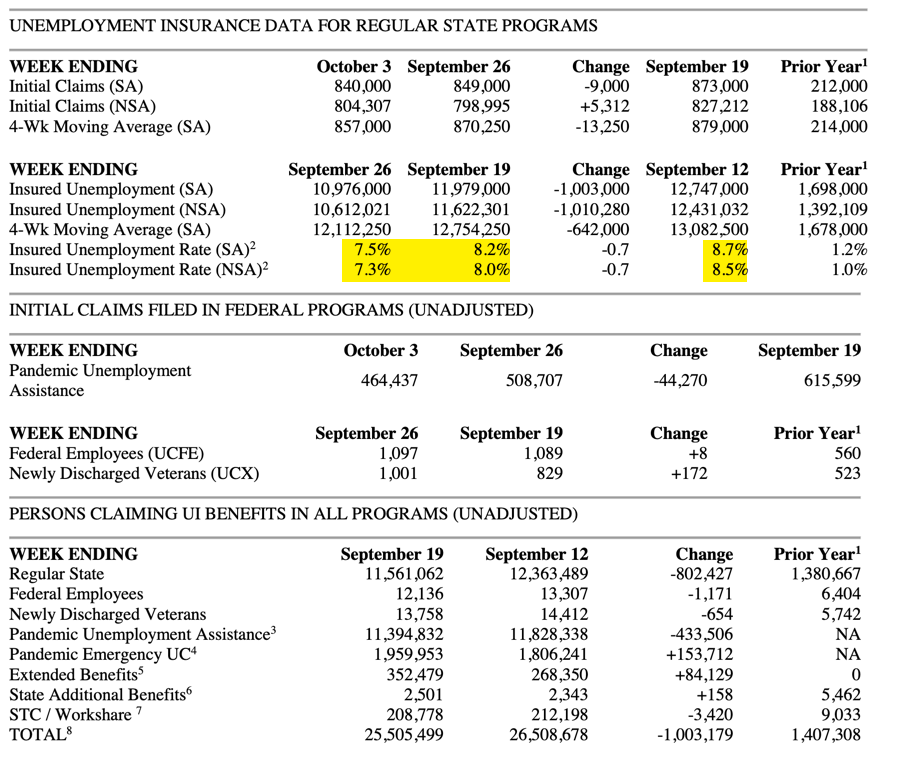

The jobless claims series came out again this morning showing 840,000 initial claims plus a modest revision upward of last week’s number to 849,000. These numbers just aren’t coming down fast enough. And we know from the last recovery that elevated claims coincided with a rising unemployment rate. But the economy avoided a double dip because of stimulus. This go ’round we are seeing a halt to stimulus but the unemployment rate has declined. What gives? I am going to try to unpack this below.

Asset markets and stimulus

Before I get into the data, let me remind you that we are still within the band of the two-month period I had said would be critical for this recovery. I first flagged this period in June, when I wrote that the recession is over. And my thesis had been that forward looking uncertainty would be mostly lifted by that timeframe. We would get a confirmation of the rally in shares and junk bonds or the rally would stall on the back of poor economic data.

And while we have been getting a significant number of negative surprises, including today’s initial claims numbers, the data are just good enough for investors to continue to feel optimistic about the near- and medium-term economic outlook. For Treasurys, shares, and corporate bonds, it’s also a big deal that the Fed’s got your back. Even if there’s no fiscal stimulus, we know that there will be a monetary offset to try and sustain economic momentum, making the policy mixed heavily skewed toward monetary policy. And that’s seen as bullish for asset prices.

So, after a correction in the Nasdaq and large pullbacks in other market indices, we have been off to the races. And price action yesterday in shares, commodities and Treasurys tells me the same narrative is still at play. Therefore, I don’t anticipate another swoon in asset prices in the near-term even in an election chaos scenario because that outcome is largely ‘priced in’.

Now, I am looking out further for when stimulus rolls off enough to elevate initial claims and eventually consumer spending and corporate defaults. We aren’t there yet. But the recent increase in downgrades of the junkiest of junk bonds is a potential precursor.

Jobs

As for initial claims, we remain at relatively elevated levels. And I continue to believe this will eventually cause the unemployment rate to tick up rather than cause people to leave the labor force as was the case in September’s jobs report, bucking the trend.

Just after the beginning of a recovery people should begin to re-enter the labor force. Moreover, the huge drop in participation rates leaves the US economy well below (a downward-sloping) trend line. So, last month’s jobs data was anomalous in that it bucked the trend toward reversion to trend. Either that’s a bad sign going forward or we will see the unemployment rate tick up as I expect.

Having said that, notice that the insured unemployment rate is ticking down, based on the roll off of the number of people collecting traditional unemployment benefits. I have highlighted those numbers in yellow in the latest report released today

But, that should not necessarily translate directly into a falling headline U-3 unemployment rate. For example, in the last cycle, the insured unemployment rate peaked at 5 percent in May and June of 2009 and fell steadily from there. But the U-3 rate of unemployment kept rising until October 2009 due to the large number of initial claims not being offset by hiring. And this is even as the labor force participation rate declined continuously through 2015 during a historically weak recovery.

The bottom line here is that there are a lot of moving parts. It’s still unclear to me what the pattern is. But, overall, job loss remains elevated enough – it’s at levels in excess of peaks of all prior cycles – that I expect job loss to be a drag on consumption and GDP growth. And I do not anticipate re-hiring to make up for that drag given an expected wave of bankruptcies and coronavirus-related local restrictions in the fall and winter.

In the end, labor force participation trends and the elevated nature of initial claims tells you to expect a weak recovery. And that’s going to worse because of a lack of fiscal support.

My view

So, now I am in the uncomfortable position of being relatively sanguine about the near term but concerned about future trends.

The US economy was more resilient than expected all throughout the last cycle despite the historically weak nature of the recovery and the declining labor force participation rate. Perhaps monetary stimulus had something to do with that. The jury is still out.

But, that means we can take heart regarding resiliency now, especially as the economy has begun moving through my September/October timeframe with more momentum than anticipated. And we know the Fed will take extra measures this time too just as it was forced to do last cycle because its dual mandate forces it to provide a monetary offset when fiscal policy doesn’t kick in.

If Biden wins and the Democrats sweep Congress, as is becoming more likely, we are going to see major fiscal relief. And I think that’s bullish for the US economy because it will eliminate outlier worst case economic scenarios that are proliferating now under the gridlock of divided government trench warfare.

The worst case scenarios are where the lack of fiscal support causes the US economy to downshift and roll over into recession under the strain of a large fall and winter wave of coronavirus. Expect the wave to be large and for economic distress to pick up at the household and business level.

I am, therefore, taking a wait and see approach, watching for signs of credit distress or a surge in jobless claims. Yesterday, I focussed on the risks. But absent those two outcomes – credit distress and a jobless claims surge – I now lean towards believing Q4 2020 will see a ratcheting down of numbers but not end in a negative print. The biggest variable for the advanced economies is the next wave of coronavirus and consumer and government policy reaction to it, in the US and in Europe.

Comments are closed.