A reckoning in the EU and more on US yield curve steepening

Two separate issues here today. The first is on the yield curve in the US. And the second is on the slow vaccine rollout in the EU and its impact on the economy.

The three yield curve outcomes

Let’ start with the yield curve. We began the year in the US with the overnight rate at 0% and the 10-year Treasury around 0.90%. Due to the reflation trade, in mid-January I began talking about three distinct potential curve outcomes. The trajectory we were on then and remain on is the most worrisome. As I put it in that January post:

Scenario #1 is the one we were on until now where the yield curve was steepening before the bullish economic outcome had crystallized. If that trajectory continues, that’s a situation where you could have weak economic and earnings data juxtaposed to rising yields and discount rates. Eventually, this is kryptonite for growth stocks because discounted cash flow models of their earnings are heavily weighted into the future, making those higher yields and discount rates a headwind.

If we stop the steepening but economic growth remains robust, that would be the best outcome:

Scenario #2 is where the yield curve steepening is arrested, stopped in its tracks as we await further progress on vaccination. And more steepening occurs only when its clear that we are at or near the end of the tunnel with pent-up demand actually a fact and not a rumour. That’s a scenario where the steepening is occurring because of an economic uplift that boosts earnings. And so, it shouldn’t hit shares as a result.

The worst outcome is where – perhaps due to viral mutation infections that cause the US economy to roll over under a fourth coronavirus wave – demand growth is tame despite vaccination. I know this scenario seems less and less likely due to the precipitous drop in cases. Nevertheless, I think it is still one of the higher probability outcomes. I summarized it this way in January:

Scenario #3 is the one I mooted above, where the market susses out that true inflation is nowhere and the lack of consumer demand means weak economic growth and earnings. The yield curve there flattens, making discount rates lower and only potentially buoying the shares of companies that can benefit in the slow growth environment (if any). The risk in this scenario is that earnings multiples more generally contract as it pops the bubble in reflation hopes.

Where are we now?

We are still on the ‘excess’ reflation track, meaning we are seeing yields vaulting higher. For example, overnight, thirty-year rates hit 52-week highs, with the 30-year now at 2.17% and the 10-year at 1.38%.

Back on February 12, I wrote that:

I will be watching the 10-year today. If it closes above the 1.1425% level, I will take that as a sign that steepening will continue and that we need to hedge against that outcome.

The 10-year is up nearly 20 basis points since then. And so, I see the hedge against rapid steepening up followed by a crash down in yields as more necessary now.

Again, the framework I am using is the stair step one from 2018 where yield curve steepening is a threat based on both absolute yield levels and the pace at which those levels are attained. Back then, what was threatening at 2.75% early in the year became the lower bound of a trading range as the yield breached that level and 2.85% became the target. And this continued all throughout 2018 as the Fed tightened policy until yields reached up toward 3.25% and the market cried uncle.

Right now, we are rapidly heading toward the first bogey at 1.50% where I expect market jitters to increase. Depending on circumstances, we could easily consolidate above that level and move to test the next range higher at 1.75% or 2.00%, depending on your support levels. Eventually, we will reach a limit as we did in 2018. And high yield, leveraged loans, mortgages backed securities, and equities will all be subject to volatility.

Since the Fed is not signalling a need for this steepening, I consider this the market looking for a level that draws a policy response. And potentially, the pace of rate increases on the long end won’t stop until we either get that response or until market volatility forces it.

For me, the yield curve’s steepening is the critical financial market event right now for 2021.

European problems

In the real economy, globally, we are seeing China outperform the developed economies, and in the west, the US outperform Europe. And the dichotomy between the US and Europe can also help retain the bid for US equity markets.

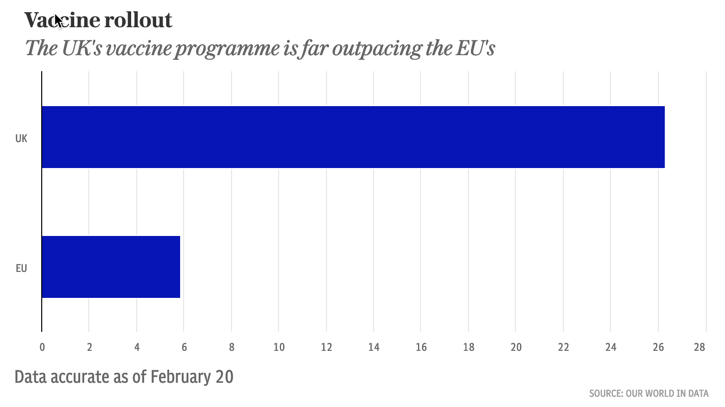

Part of this can be explained by the coronavirus outbreaks in Europe and the subsequent lockdowns. South African and UK mutant strains of the virus are circulating widely and may play a part in the current outbreak. But, if we look forward, it’s the slow rollout of vaccination in Europe which is worrying for the economy.

On Thursday, I started a Twitter thread on Europe’s poor response. The Wall Street Journal’s Bojan Pancevski outlined an article he co-wrote about how Europe’s vaccine rollout was not just slow but also marred by disinformation and fear about the vaccines. The issue is the Astra Zeneca vaccine, which was the subject of an EU-UK dispute and reports of ineffectiveness in South Africa

Thousands of healthcare workers are refusing to take the Astra Zeneca vaccine in Europe after politicians like French President Emmanuel Macron denigrated it. Macron called it ‘quasi-ineffective’. And that plus reports of side effects from the vaccine is leading to people wanting to choose which vaccine they receive. It’s gotten to the point where some officials in Germany are going to allow queue-jumping for those less vulnerable to prevent spoilage of the Astra Zeneca vaccine.

Meanwhile, in Scotland, data released show “the Pfizer and AstraZeneca vaccines were found to reduce the risk of hospitalisation by up to 85% and 94% respectively.” So, while European vaccination lags, UK and US vaccination moves forward. And that will definitely have negative economic implications for the EU. The difference to the UK is especially stark.

Source: UK Telegraph

Ambrose Evans-Pritchard at the UK Telegraph has it right:

That could prove to be an expensive upset at a time when the British B.1.1.1.7 variant is rapidly taking over. France is already where the UK was in early December just before when the epidemic went parabolic. The variant was 36pc of all French cases late last week, reaching 54pc in some departments. The South African and a Brazilian variants are more than 10pc in four departments.

French epidemiologists say the apparent stability in new cases is an illusion. There are two separate epidemics: the old one is declining with the current partial restrictions; the new B.1.1.1.7 epidemic is relentlessly rising. The numbers seem to knock each other out for a while until the variant reaches an inflexion point and goes wild.

My view

This is the same foot race between vaccination and the mutant strains I see epidemiologists in Canada and the US talking about in their populations. And the EU looks especially poor here because of a combination of a slow vaccine rollout and the advance of mutant strains. Let’s also remember that while the Astra Zeneca vaccine was less effective against the South African variant in studies there, it did stop severe sickness, hospitalization and death, which is what we care most about.

So, not only is the double dip for Europe already baked into the cake, now we also have to fear another wave because of the poor policy response. And this is happening against a backdrop of massive deficit spending in a currency area where governments have no monetary sovereignty.

It may seem like deficit spending can proceed apace in Europe because of the special situation afforded by the pandemic. But it cannot. It is contravention of the rules.

Europe will decide whether to extend the suspension of its rules limiting budget deficits and debt, known as the Stability and Growth Pact (SGP), in coming weeks, the Commissioner for Economy Paolo Gentiloni said on Monday.

As the slow vaccine rollout risks public health in the EU, a reckoning on the fiscal front is coming for Europe as well.

Meanwhile watch the 10- and 30-year Treasury rates as well as the 30-year fixed mortgage rate in the US. That’s where the potential for market volatility resides in the US.

Comments are closed.