Entering the third phase of recession

Last week, a friend from business school who I met up with in New York in early March told me she had taken an antibody test for coronavirus and came back positive. Her first thought was about donating blood, whereas my first thought was about whether I had contracted the virus. So I am consulting my doctor tomorrow about next steps.

Immediately after I returned from New York in March, I went into quarantine for two or three weeks. I didn’t go to the store. I didn’t see anyone socially. I didn’t go for my usual group bicycle rides. I just stayed at home. At some point in that time period, I was overcome by a period of unusually extreme fatigue and my immediate thought went to coronavirus. I took my temperature. Nothing. All was well. And eventually the fatigue subsided. On Saturday, I even went out for a 100 kilometer solo bike ride. It was amazing.

Could I have had the virus? Maybe. My friend told me she had eerily similar mild symptoms. I will find out either way. I do know, however, this puts me in a different mindset as US states consider re-opening their economy.

Re-opening isn’t ‘re-opening’

In South Carolina, Georgia and other states where lockdowns are starting to ease, residents are slow to resume pre-pandemic routines—indicating the nation is in for a slow rebound. https://t.co/A66rodanzj

— Edward Harrison (@edwardnh) May 3, 2020

Knowing what I know about my contact with coronavirus, I’m not going to the malls anytime soon. Sure, I might be immune. But, then again, I might not. And unlike me, most people in the US haven’t had a contact tracing text telling them they might have had the virus. Why would they go to the shopping mall? Maybe they’re fearless. Or maybe they’re just clueless.

South Carolina’s post-lockdown experience tells you that a lot of people are still afraid though. And I think there’s good reason for that. Moreover, Apple data shows us that people will continue to shelter-in-place whether governments say so or not. It’s consumer behavior leading governments, not the other way around.

The US is a testing laggard. And it was a lockdown laggard too. From everything I know about controlling the Covid-19 outbreak, the chances of a second wave in the US are high relative to countries like Germany, Denmark or New Zealand. People know that. And that informs behavior.

As I wrote last week:

The best case scenario is that R0s do not rise above 1 and that re-opening can proceed in a step-wise manner. In the most prepared economies like New Zealand or Denmark, maybe we get to 70-80% levels by the end of the quarter with deficit spending bringing us up to the 80-90% level.

That’s best case. Goldman Sachs has come to similar conclusions. Here’s the Economist on their modeling:

Measures to control the virus while either keeping the economy running reasonably smoothly, as in South Korea, or reopening it, as in China, are associated with a GDP reduction in the region of 10%. That chimes with data which suggest that if Americans chose to avoid person-to-person proximity of the length of an arm or less, occupations worth approximately 10% of national output would become unviable.

And Ireland, for example, shows us that there will be a lag in ramp up. The Irish Times reports that “the State by Chambers Ireland are reporting a 60 per cent-plus fall in revenue as a result of the Covid-19 restrictions.” Soon, this will change. But they warn that “cash shortages affecting SMEs and the challenges they face in reopening when restrictions are lifted.”

Most expect some recovery in the second half of the year but a majority still expect revenues to be down more than 50 per cent this year.

[…]

Half of those surveyed said it would take two weeks to fully reopen and 25 per cent felt it would take over one month.

A minority in seasonal sectors, such as tourism, do not expect to reopen until 2021.

What happens next then?

With all this fiscal and monetary stimulus in place, there has been a collective sigh of relief. For a while, it had even seemed like markets thought the worst was over. But reality is hitting now – the third phase of recession. As I framed it in mid-April, there are three phases. In phase one, you have the initial downdraft and potential liquidation of hedge as well as Ponzi investors.

The government response ushers in a stabilization and hope that the worst is over. That’s phase two, the hope stage of recession. But, that’s always followed by the ‘discover’ or ‘real economy’ phase, what my colleague Raoul Pal calls the ‘insolvency phase’. It’s where illiquidity and insolvency diverge. And the truly insolvent are found out. And that’s when we get to see how bad the damage is.

We’re there now. The insolvency phase is beginning and markets are reacting negatively already. If you didn’t adjust your investment portfolio to mitigate downside risk already, now is the time to do so because I believe we will be re-testing the lows.

Two weeks ago, I suggested we look at Sweden to understand what a post-lockdown world looks like since their light-touch approach is similar to where we would be headed. Here’s how I framed it then:

Sweden, which has had one of the softest lockdowns so far, could show us what the economy looks like post lockdown. There, bars and restaurants are open and social distancing is suggested, not mandated. That’s the world we are likely to have after our lockdowns finish. So I looked to see what’s happening there economically.

And what I saw was mildly positive. I said “Sweden shows us there is some room for optimism. It may not be V-shaped recovery optimism. But it is optimism about the ability to prevent a Great Depression.”

Here’s an update from Swedish business newspaper Dagens Industri though. I have translated it into English:

Hotel rooms are empty and restaurants try as best they can to operate within the limits of the Public Health Authority’s restrictions and recommendations. During the first three weeks of April, a total of 183 companies in the industry went bankrupt.

Worst hit is Stockholm where 54 companies, active in the hotel and restaurant industry, crashed during the period. This represents an increase of 286 percent compared to the corresponding weeks last year. The Stockholm Chamber of Commerce recently describes it as “a dark and destructive month”.

“We are in a serious financial situation right now and many companies are struggling for their survival. Unfortunately, we can see that many companies are not successful, ”says Stefan Westerberg, economist at the Chamber of Commerce.

Perhaps even more telling for the serious situation is the number of people who lost their jobs as a result of the bankruptcies in Stockholm County. During the same period last year, 44 people became unemployed as a result of bankruptcies in the industry – this year there are 696 people.

Sweden is seeing mass bankruptcies. And this is just the beginning. For small businesses, it will get much worse before this is over. The message to economies leaving lockdown is that there will be a snapback in output after lockdowns are eased. But, it won’t get us to anywhere near norm.

Looking through the post-lockdown bounce

What we should expect instead is a second wave of unemployment filings as the bankruptcies Sweden is recording hit en masse in post-lockdown economies. The Financial Times sketched this out in an article yesterday (link here). Their take was that it may take 6-12 months before this second wave of unemployment is fully accounted for.

The question then turns to the epidemiology unfortunately. I don’t have a voice there because I’m not a scientist. So, I can only frame this in terms of best, base and worst-case outcomes based on the size of second and third wave outbreaks.

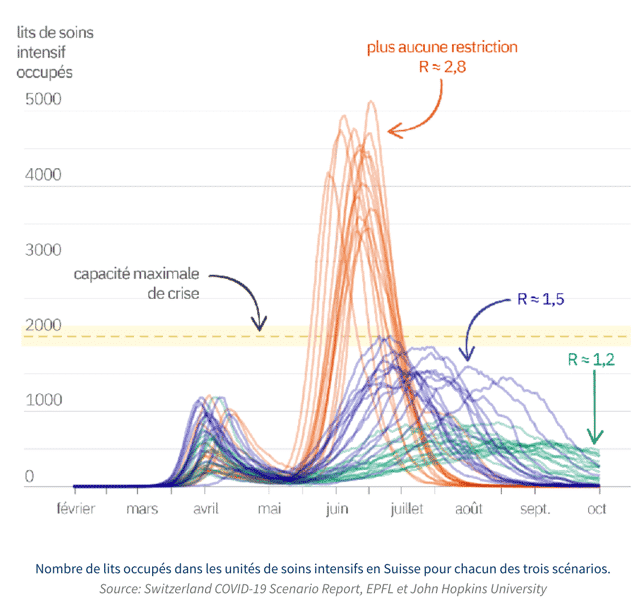

The frightening non-best case outcome is the one I read presented in Le Figaro last week. The headline “In Switzerland, the lockdown relaxation raises fears of a more deadly second wave”.

Here’s the graphic for Switzerland, showing R0s rising well above 1.0 and causing a second wave larger than the first.

How realistic is this though? Here’s the translated text on the answer:

Even a slightly more optimistic scenario, with an R0 of 1.2, would be brutal. It would imply a very high peak with some 800 people in intensive care between July and September, 5,000 to 15,000 dead in total, and 2 to 5 million people infected. “Unfortunately, this is a completely realistic scenario,” says Professor Jacques Fellay, of EPFL, who supervised the study. The doctor, who specializes in the relationships between infectious diseases and human genetics, is a member of the scientific task force set up by the Federal Council. “It is not by banning only a few festivals during the summer that we will be able to keep this R0 below 1.2.”

Fellay implies we will need much more robust social distancing protocols going forward to even keep the R0 down to 1.2, which is still a scenario in which you get exponential growth in infections.

That’s worrying to say the least. Irrespective of what governments do, human behavior will shut things down as people, frightened about the risk of contagion and death, will go back into a shelter-in-place mode. That will mean going from a 50-60% economic scenario up to a 70-90% one followed by a retreat back closer to the original 50-60% output scenario. This is the infamous W-shaped recession.

My take

Over the past week, I have really expanded my data sources. And I have done a ton of reading regarding what governments around the world are doing and what their economies look like. I am trying to synthesize all of that data into a coherent mental model of outcomes.

The conclusion I come to is that we are not headed for a V-shaped recovery or even a U-shaped one. The best case outcome is an L-shaped or W-shaped recovery. And that’s best case. That’s what I would call a slow ‘jobless recovery’ made possible by continued and constant support from fiscal deficits and monetary liquidity.

The base case is a global depression with a small d, where the post-recession scale of joblessness and bankruptcies is so severe, it would be hard to think of it as a recession but more like a depression. Here, government policy easing might prevent worst case outcomes. But that won’t save all those small businesses from hitting the wall.

Moreover, as governments step in to save big businesses, the moral hazard of supporting both poorly managed firms with their better-run brethren will sap the economy of its vitality over time. You can see this beginning with the deal coming into form to rescue the over-indebted Norwegian Airlines.

Worst-case outcomes involve very high second and third waves of the virus forcing the economy into freefall and governments unable or unwilling to stop the attendant financial distress from hitting the financial system hard. That’s a Great Depression outcome because it leads to a stricken financial system which creates a vicious doom loop of insolvency.

I wish I had something more uplifting to say as the week begins. But, you can see the bad news in the news flow – markets down in Asia and Europe, oil down, Warren Buffett hoarding cash, jettisoning airline shares and not buying anything new. It all speaks to this last bounce in risk assets as driven by hope and not fundamentals.

As this insolvency phase heats up, I expect a re-testing of the lows. And so, I am hoping for a post-lockdown bounce that ends the recession and leaves us in an L-shaped slow grind-it-out recovery That’s the best case.

Comments are closed.