Epidemiological tail risk in an era of missing price signals

The title of the post is supposed to marry what’s happening on the pandemic front with what’s happening in financial markets. The gist is that, in a world where unexpected levels of economic resiliency has been the norm, we should wonder why it makes sense to think too much about downside risks. I am going to try and frame the picture without making too overt a case for thinking about so-called tail risk. But downside risks are always something that occupy my mind.

The pandemic mutations

Let’s start here:

Mutated versions of the coronavirus threaten to prolong the pandemic, perhaps for years — killing more people and deepening the global economic crisis in the process.

This is a view that I have been hinting at for some time. See my post from January 13 and the one from January 21 for the longest-form expositions. So I might as well make it explicit; there is a non-zero probability that the mutant viral strains of COVID-19 that are circulating now will set back our efforts to eradicate the deadly virus for months if not years.

We already know of three more infectious variants first detected in the UK, South Africa, and Brazil. Two of these variants have spike protein mutations that make it possible that present vaccine configurations are less effective against them. The UK variant has been detected in numerous countries now. The Brazilian and South African variant have as well.

What’s notable about the South African variant, one with spike protein mutations, is the following report from January 28:

South Carolina officials disclosed the first two cases in the United States involving the B. 1.351 variant, and the patients’ lack of travel or connection to one another suggests the variant is spreading in the community after an undetected introduction.

If two unrelated cases of the South African variant have been discovered in South Carolina in patients with no history of travel, you know you have massive community spread already. It’s only a matter of time before this variant is everywhere. Likely, these more virulent mutant variants will spread worldwide within weeks and months.

And then the question is what happens next.

Mutation tail risk

The most plausible outcome is that we have a foot race between vaccination and mutated viral spread. The goal is to vaccinate as many people worldwide as possible to make viral spread less deadly so that we can leave this state of siege we have been under since March. Maybe we will need a booster shot to deal with the new mutations. And the new normal won’t be like the old normal. We might even still wear masks in many public places for years to come. But, after the mass vaccination, in this scenario, we can return to offices, schools, airports and vacation destinations without being overly concerned about infection and death.

There are other outcomes though. And for the time being, let’s consider these outlier scenarios, what financial professionals like to call tail risks because they reside in the extreme left-hand end of a distribution of outcome probabilities. This post on a virologist’s blog hints at those outcomes. The question: The coronavirus is mutating. Will our vaccines keep up?

The likely answer is long:

Even if these new strains remain highly susceptible to the vaccines we already have, their emergence suggests that SARS-Cov-2 has the ability to mutate enough that it could, over time, evade a vaccine.

That means several things. First, the virus is never going away. Even if it could be eliminated from the human population, it can infect other mammals, mutate in them and then jump back to humans.

Second, the more people infected, the more opportunity the virus has to mutate in a direction that creates problems. So, it is in the self-interest of wealthy countries to get vaccines distributed worldwide to limit those opportunities.

Third, covid-19 will become much like influenza, requiring year-round, worldwide, surveillance of new strains and regular updating and administration of vaccines. We may not need a new vaccine every year, but we will need new vaccines, nonetheless.

There is one other answer. Scientists must search for parts of the virus that remain stable amid mutations and still generate an immune response. With influenza, scientists have made progress toward this. For both viruses, that’s the vaccine we need. That is now the holy grail.

Conclusion: here is a non-zero probability that the mutant viral strains of COVID-19 that are circulating now will set back our efforts to eradicate the deadly virus for months if not years.

Economic outcomes

So, let’s say John Barry is right about the outcomes, that the virus is never going away. What does that mean economically? In one potential future, we could have a new normal largely similar to the old normal because of vaccines. And then we would learn to live with the increased mortality from coronavirus mutant strains.

But, in another potential future, that risk of increased mortality would be enough to alter behaviors, in effect bankrupting large swathes of the economy impacted by that change. This is the economic tail risk. I call it a tail risk because we’ve seen time and again how resilient the US and global economies have been in the face of calamity. Yes, we’ve had a difficult stretch ever since the Great Financial Crisis. But it has yet to be anything like the Great Depression. And I would say that is in large part due to the overwhelming policy response designed to prevent that outcome. I expect these measures to continue. And while they won’t be pretty and they won’t be perfect, if they continue, they will prevent a Great Depression.

Price signal distortions

But, the collateral damage of all of this intervention, particularly on the monetary side is the distortion of price signals. John Plender had an interesting piece in today’s FT on this. He pointed to passive investing as one distortionary actor because the dominance of index-related investing makes markets less sensitive to fundamental value. If you add in zero and negative policy rates and central bank asset purchases, it’s hard to know what the market is ‘telling you’ based on a financial asset’s price. Is it a reflection of liquidity, low interest rates or fundamental value? No one knows.

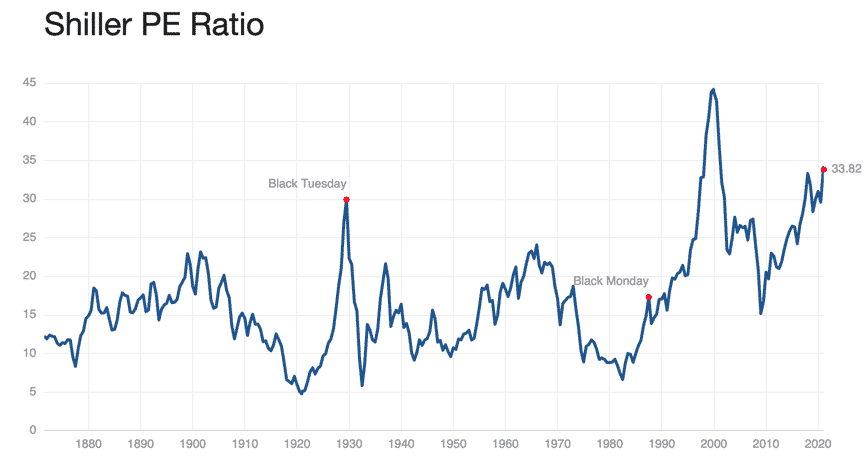

And this is why the GameStop saga makes sense. Right now, financial markets are completely divorced from underlying economic fundamentals. It’s not just GameStop. Tesla is a company that barely makes any money and has a small share of its market, yet has a market capitalization of $752 billion. And the overall market has a Shiller P/E ratio higher than at any time outside of the Internet bubble.

If you’re a retail investor, of course you’re going to pile into GameStop. Of course, you are. Valuation doesn’t really seem to matter anymore. And look at the returns. Is that not a risk worth taking?

I noticed that American Airlines saw an opportunity out of this and quickly raised $1.1 billion in new equity capital on Friday. Like AMC, who did the same early, after the short squeezes these past couple of weeks, American Airlines can live to fight another day. And even if their business model is compromised for 4 or 5 years as the Axios article I cited at the outset suggests, they have $1.1 billion more money to fight against that.

My View

Of course, this is a misallocation of resources. American Airlines is a company that has treated customers shabbily for years. It could get away with that because regulators allowed it to combine with US Airways, which had combined with America West before. And like the other US airlines, on many air traffic routes, there was scant competition.

With the major shift in business travel ushered in by the pandemic, American Airlines is on its knees financially. That’s why there was so much short interest in the stock. This gift from retail bets on the airline will help it stagger along as a zombie company whose operating income doesn’t even cover interest payments until it either recovers or goes bankrupt.

But this is a side show, the real risk is that investors have piled into these bets, not only because valuations don’t matter when price signals are distorted.; they’ve piled in because they believe the Fed’s got their back. When all is said and done, the Fed will prop up financial markets, if only to prevent a Great Depression. That’s the belief. If that belief is mistaken, the big tail risk is that epidemiological tail risk crystallizes financial market tail risk.

Comments are closed.