Positive thoughts on my return from Germany and London

I was in Cologne and London last week, two places I know quite well. And as I went out, my trip down memory lane was greeted by the eternal progress of human endeavour. Whether riding the frequently behind schedule Deutsche Bahn by the former Ulrich Haberland Stadion or the S-Bahn through relatively newly-built stations in downtown Cologne or walking along the Thames near Borough Market and the Shard, I marveled at the transformation.

Both the UK and Germany are supposed to be in a recession right now. And the UK is in the midst of a great political upheaval. The mood on the streets of Cologne and London were buoyant, totally unaffected by the gloomier political and macro backdrop. That’s as it should be.

You could say the same about DC, where I live. Despite huge political upheaval, people’s day-to-day lives continue as usual. And the building here both in the downtown areas and along new transit corridors like the coming Purple Line light rail is frenetic.

So, for me, it was a good trip. It reminded me that the doom and gloom of inverted yield curves and recessionary manufacturing data is only a small part of the picture.

But the data?

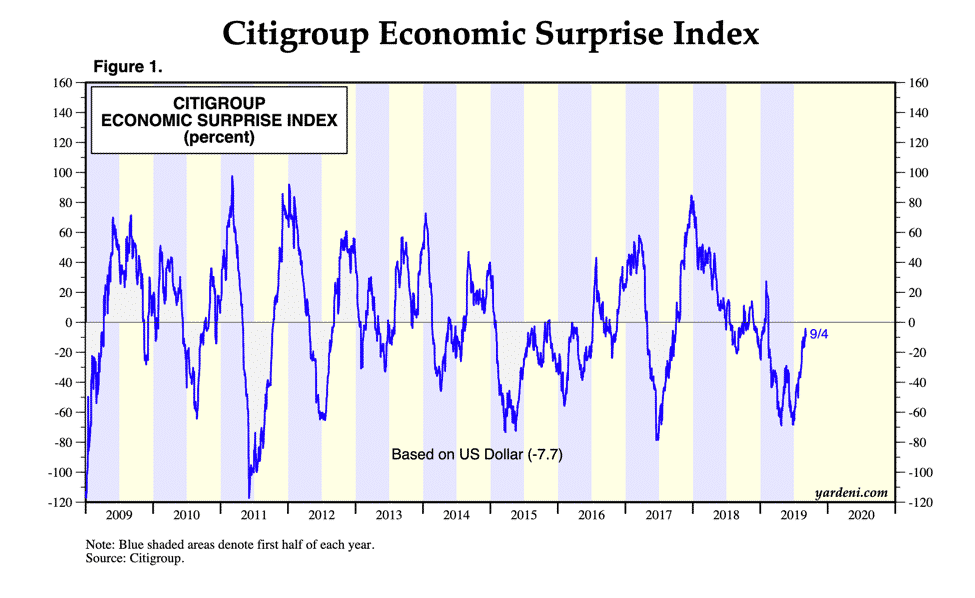

Having said that, I still want to talk about the data. Of late, the negative surprises have lessened and the positive surprises have increased. The Citigroup Economic Surprise Index for the US is almost at a breakeven point, after a massive down move from late 2017.

Source: Yardeni Research

That’s telling you that, relative to expectations, the data releases are improving. Moreover, as I mentioned last week, “[f]rom a purely data-driven perspective, it’s probably too early to predict a recession. It’s simply not there in the data.” So both the absolute level of US data and the trend tell you the expansion will continue.

And yet, there’s this:

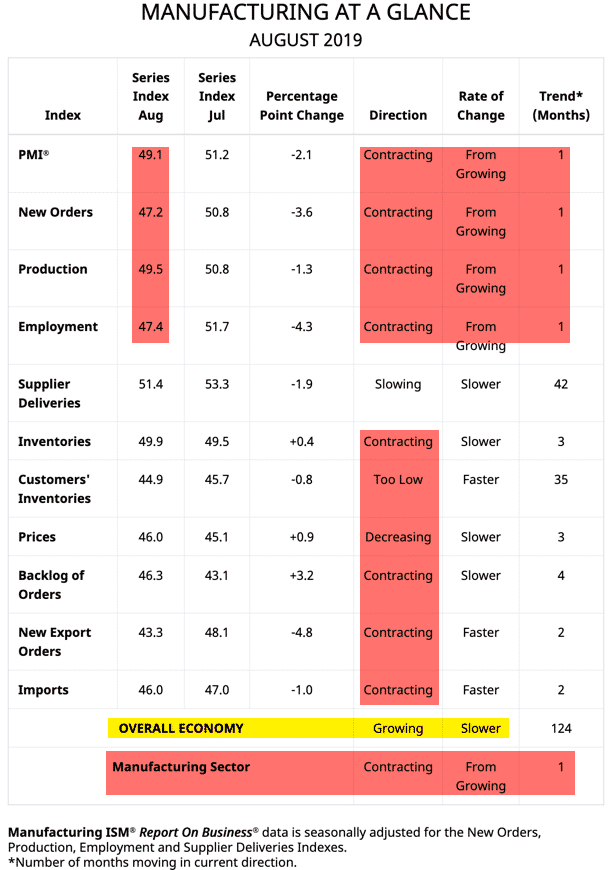

The US manufacturing sector is now contracting. I wouldn’t say it’s in a recession because the main numbers highlighted in red show that this is only the first month of contraction. But the numbers beyond the first three main sub-indices are even worse than the headline number and the three main sub-indices.

Where is this going then? The optimist in me looks at the analysis below and sees hope for a turnaround – especially with the Citi Surprise Index powering upward.

Lowest ISM Manufacturing readings w/ no recession w/in 2 yrs…

Dec 2015: 48

Apr 2003: 46

Dec 1998: 46.8

Jan 1996: 45.5

May 1985: 47.1

Apr 1967: 42.8— Charlie Bilello (@charliebilello) September 3, 2019

But, it isn’t clear where this is headed. I believe policy errors are going to be a big part of whether we see this turn around or degenerate into a manufacturing and general recession.

Market data

A lot of people are focussed excessively on the yield curve right now in looking for economic signposts, simply because these are market-driven data points.

What’s the yield curve saying?

- The front of the curve from fed funds to 5 years is inverted, suggesting market anticipation of further cuts in fed funds rates.

- And while the curve is deeply inverted from 3 months to 10 years, the curve is no longer inverted from 3 months to 30 years or 2 to 10 years though.

According to the NY Fed’s model, the probability of recession in the next 12 months is 38%, a level that has nearly always meant recession was a lock over the next 24 months, including in 1967 when it moved lower, only to surge again into recession in December 1969.

So, my read, then, is that recession is likely over the medium term out to two years, though not necessarily imminent in the next six months.

As someone who once plied his trade in the high yield world, I tend to look for market based signs of distress there. Here’s what you see:

investors in corporate bonds were unperturbed by talk of a recession.

“The markets are caught between two stools, as the bond market is rallying on slowing global economic data, while the risk markets are not reacting in similar fashion,” said Sean Simko, head of fixed-income portfolio management at SEI Investments, in emailed comments.

The yield premium that investors demand in return for owning a basket of benchmark bonds over risk-free Treasurys, or the credit spread, stood at 4.13 percentage points on Sept. 2, up from around 3.93 percentage points on July 26, a day before President Donald Trump imposed 10% tariffs on all remaining untaxed U.S. Chinese imports, according to an index provided by ICE Data Services.

That’s well below the post-crisis average of around 4.81 percentage points, according to CreditSights. Wider credit spreads can reflect when investors are less willing to take risks in search for yield.

[High Frequency Economics chief economist Jim] O’Sullivan said the recession probability in the next 12 months based on high-yield credit spreads stood at 14%. On the other hand, the New York Fed’s recession-probability model, which looks at the yield spread between the 3-month bill and 10-year note, estimated a 41% chance of an economic downturn.

And remember, high yield default rates are still very low. There is almost no sign of distress in this ‘canary in the coalmine’ market. Which market-based signpost should you believe?

I lean toward the high yield side. A 14% recession probability is too low, but the 41% probability is too high. But I shade toward the 14% figure. Until we see distress in high yield, I will remain sceptical that the US economy is headed toward the cliff.

Hopefully, tomorrow I can also provide you some brief thoughts on European High Yield and what that says about the economy there. For now, keep your tin foil hats to the side. The sun is still shining.

Comments are closed.