The end of global co-operation among liberal democracies

I am back from my beach vacation. So, let me outline what my thinking is after a period of reflection and how it has changed or stayed the same.

I last posted more than a week ago right before I left, regarding my frustration about policymakers’ unwillingness to act directly to improve the lives of working and middle class citizens. The timing was right because, in the intervening week, there has been a spate of commentary about exactly this, particularly around the impotence of monetary policy. Larry Summers’ comments come to mind. But there have been many others too.

It’s a long overdue discussion, this back and forth about the efficacy of monetary policy to improve the lives of everyone, especially society’s most vulnerable. And that’s because, for too long, the prevailing ideology has been that ‘market forces’ were paramount in importance, and everything else was creeping socialism — which is bad. But, the rich and politically-connected have used this hands-off approach to tilt the playing field in their favor. And the end result has been widespread disenchantment in developed economy middle classes that has descended into an us-vs.-them circle-the-wagons breed of nationalism and identity politics. I suspect it will get much worse before it gets better.

So, as heartened as I am that we are having this discussion, I am alarmed by the political backdrop that shapes it.

Recession

When I woke up this morning, I checked the bond market data. And the numbers weren’t good. The 2-year yield was trading above the 10-year yield by 5 basis points. And now, even the 30-year yield is trading below the 3-month yield. In short, the yield curve is unmistakably inverted. And while that’s not a ‘predictor’ of recession, for me, it’s a signpost that we should consider a recession our base case in 2020, as I have done for the past two months.

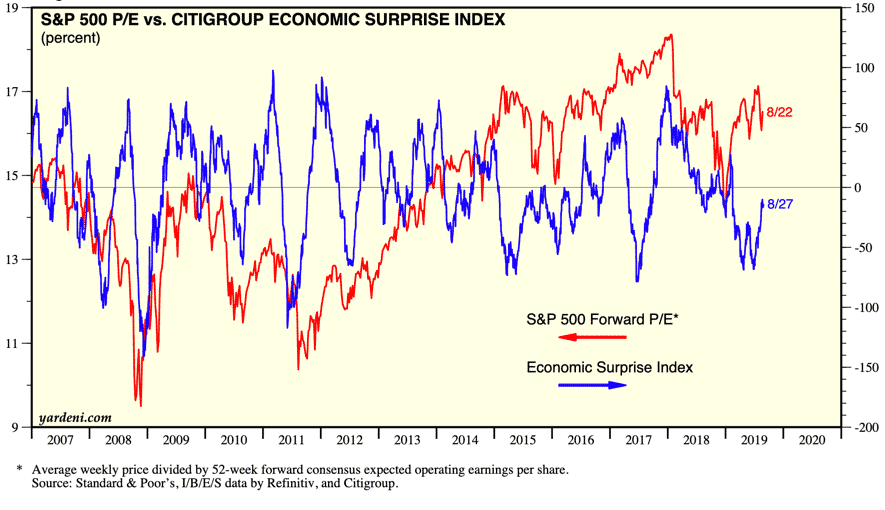

Now, the economic data have been pretty good of late. I know Germany is likely in a recession. But a lot of that owes to their export-oriented, manufacturing heavy economic model. If you look at the US data, it’s still good. And the headline numbers — 3.1% growth in Q1, 2.1% growth in Q2 and a Q3 GDPNow read of 2.3% – speak to resiliency. Citi’s economic surprise index has actually turned up after a long downward move from late 2017.

Source: Yardeni Research

From a purely data-driven perspective, it’s probably too early to predict a recession. It’s simply not there in the data.

But, the policy backdrop is downright frightening, with the US-China trade war, a likely US-European trade war, and Brexit staring us in the face over the next several weeks. The potential for policy error is so high that I believe recession-inducing policy errors are essentially unavoidable. The inverted yield curve is simply a signpost that this outcome should be your base case.

The end of global co-operation

The G7 meeting was the signpost that the age of liberal democracies acting in concert is over. Global co-operation has been superseded by nationalism and beggar thy neighbor. G7 host Emmanuel Macron tried to diminish the look of failure by announcing upfront there would be no G7 statement. But that didn’t fool anyone. The veneer of cooperation was wholly absent, with Macron inviting the Iranian foreign minister to the G7 meeting city and Trump advocating for Vladimir Putin’s rehabilitation as a member of a G8.

But, it’s the US – China dust-up that makes it clear we are entering the age of nationalism. For me, this article from Bloomberg outlines what is really going to happen there:

Perhaps nobody was more surprised to hear that China had called President Donald Trump’s administration to restart trade talks than the government in Beijing itself.

After a weekend of confusing signals, Trump’s credibility has become a key obstacle for China to reach a lasting deal with the U.S., according to Chinese officials familiar with the talks who asked not to be identified. Only a few negotiators in Beijing see a deal as actually possible ahead of the 2020 U.S. election, they said, in part because it’s dangerous for any official to advise President Xi Jinping to sign a deal that Trump may eventually break.

[…]

While officials in Beijing are still willing to engage in trade talks, they are concurrently girding for a decoupling from the world’s biggest economy — an effort made all the more acute when Trump “ordered” U.S. companies via Twitter to look for alternatives to China. After trade talks broke down in May, Xi renewed calls for China to pursue “self-reliance” in key technologies and even called on citizens to join a “new Long March.”

“A gradual decoupling is happening de facto because companies have to make alternative plans when there’s so much uncertainty,“ said Tim Stratford, chairman of the American Chamber of Commerce in China and a former assistant U.S. trade representative.

Meanwhile, in the US, Trump is losing his base as the trade war bites. Farmers are turning against him. And that’s going to create panic and policy errors.

European economic disintegration

It’s not just Trump driving this though. You see the same dynamic playing out in the UK where Prime Minister Johnson is poised to suspend parliament from mid-September in order to minimize the time the opposition has to thwart his Brexit plans.

A No-Deal scenario is the base case for France and Germany, with the EU threatening the UK on trade over the size of a No-Deal divorce settlement. If you cool heads will prevail and a best-case outcome is still possible, you should still prepare for a worst-case outcome, which deepens recession in Europe.

In Italy, the former coalition Five Star Movement and Matteo Salvini’s League are at loggerheads, with snap elections looming. Five Star would lose 114 of its 216 deputies in the lower house were elections held. And that could propel the League to uncontested victory and confrontation with Brussels.

In Denmark, a second bank has decided to pass on the central bank’s tax on excess reserves to large retail savings account.

Sydbank A/S, Denmark’s third-biggest listed bank, will follow Jyske Bank A/S and place a rate of minus 0.6% on retail deposits larger than 7.5 million kroner ($1.1 million), according to a statement on Wednesday.

This is an ominous sign. Denmark’s monetary policy and currency closely tracks the ECB and the euro. So, when the ECB meets next month, if they lower their base rate even further, the Danish will be forced to do so as well. And that means more deposit tax passthroughs – not just in Denmark but right across western Europe, where the weak banking system is in serious danger. We are close to this leading to a crisis in my view.

All norms thrown out the window

All of this is happening against a backdrop in which the us-vs-them mentality has meant throwing all political norms out the window. Johnson’s gambit in the UK is certainly in that vein, and risks a constitutional crisis there. As one economic analyst I follow put it:

If your constitution relies on norms rather than rules and those norms start to break down, you have a problem.

A written (or codified if you prefer) constitution has always seems a bit of a niche demand in the UK. Suspect that begins to change now.— Duncan Weldon (@DuncanWeldon) August 28, 2019

In the US, Donald Trump has shattered all norms. And a written constitution hasn’t stopped that from becoming a problem. For example, just recently the Justice Department head William Barr has booked a private holiday party at Trump’s Washington DC hotel, claiming all other venues were booked. The right thing to have done was to cancel the event if he couldn’t find somewhere else to host it. But, in a world in which Trump can continue to use his presidency to steer business toward his hotel chain without repercussion, this makes sense. Norms don’t matter. Corruption can hide in plain sight.

That’s certainly a major reason Trump has floated the idea of hosting the next G7 at his Doral Golf Resort, something Fox News hosts have defended.

The biggest norm just broken though was by the Fed. Former NY Fed President Bill Dudley penned an astonishing opinion piece at Bloomberg, which essentially advised the Fed to thwart Trump’s economic agenda and his reelection by keeping monetary policy too tight.

This can’t be undone. The message is now out there. As Former Minneapolis Fed President Kocherlakota put it in response:

Going forward, the public will always wonder whether the Fed was using its monetary policy tools to create a recession so as to drive the current President from power. There is no way that the Fed could – or should – survive if this becomes a major part of its deliberations.

The Fed is now permanently tainted. In a world rife with conspiracy theories because of the power of the Internet to bring like-minded people together, Bill Dudley’s piece has eviscerated any credibility the Fed ever had as an apolitical actor. Therefore, as the 2020 election approaches, with the yield curve inverted, we are entering a new dangerous age of politicized monetary policy. Expect the same in Europe to occur in due course.

Here’s the thing though; once you have eroded norms, identity-focused and nationalistic leaders of powerful countries are free to use any means necessary to shore up their base of support. That could mean enacting emergency war powers for an extended period as a pretext for just about anything domestically and geopolitically.

This is a very dangerous period in history.

My final thoughts

So I come back from holiday more alarmed than ever. My alarm is not about the economy though. I wish it were. Instead, the feeling I have is that we are living in a world where almost anything goes. Anything is possible politically. And that’s not a good thing. Bad actors will use this freedom to support their own narrow interests. And everyone else is going to pay the price.

I am off to Germany and London tonight. I will have more thoughts on the German situation after that trip. I apologize for having to write these apocalyptic notes. But I’m just trying to call it as I see it. And right now it doesn’t look good.

Comments are closed.