Surging markets, low volatility, and fake liquidity

As I note today how the upcoming Uber IPO tells us that equity investors are still quite bullish, I also realize that this particular bull market is unique in its absence of volatility. There have been a few hiccups a long the way, including the Feb 5th, 2018 purge of XIV punters. But that’s been the exception, not the rule. The question is why and what does this mean for the future. I have a few thoughts I want to share on that score below.

Let me say first, though, that this is one of the occasional free Credit Writedowns posts I write. If you like what you read please consider subscribing to the newsletter at the link below.

My own bullish views

Let me start with my own bias here. In the wake of the financial crisis, I called the market bottom fairly early to general disbelief, so much so that I wrote a whole post on confirmation bias causing people to miss the rebound. Even so, I was sceptical of the recovery. I called it “the fake recovery“. And for a long time, I expected it to peter out by 2013 at the latest.

Somewhere along the way, I changed tack. In retrospect, I would put it about 2011, when I was writing about municipal bonds – defending them as not likely to melt down because of the resilience of the economic expansion. And even though I have warned of downshifts since that time – with good reason in hindsight – it has always been predicated on my sense that the Fed was getting ahead of itself and overtightening as it did in 2018.

The Fed has finally realized it overtightened though. And I think there are good odds this recovery continues through 2019 and beyond as a result. So, my bias is bullish, as it has been for most of the last decade.

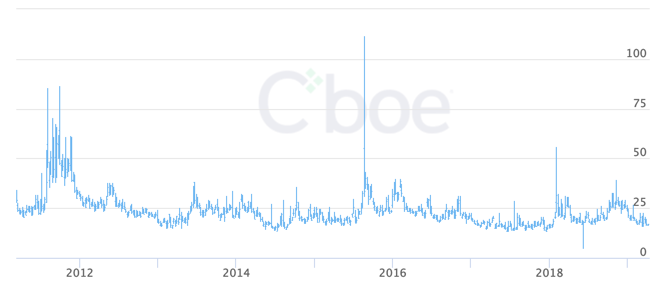

Low Volatility

But this low volatility regime leaves me with a sense of foreboding. EVERYTHING is showing low volatility as all risk assets are being bid. It doesn’t matter if you are talking about equities, high yield, or leveraged loans; volatility has been absent.

Take emerging markets , for instance. I remember sitting on an EM trading desk during the Thai Baht meltdown in 1997 and a high yield desk in 1998 during the Russian default. And these events seemingly came out of nowhere. And this was after the so-called ‘Tequila Crisis’ in 1995 and the Treasury meltdown in 1994 on the heels of the jobless recovery of 1991-1993. Volatility was always around the corner. But the CBOE Emerging Markets Volatility Index shows you volatility today is short-lived.

Compared to past business cycles, this cycle is remarkable in the ability of central banks to tamp down on negative sentiment and keep all markets moving up and to the right. That’s great for the likes of Uber, which lost $4 billion on $7.9 billion of revenue in 2017. But for how long?

Fake liquidity

One thing that concerns me greatly is what I would call fake liquidity. And a lot of it is driven by the passive investing, exchange-traded product craze. You have markets like the high yield market, which are inherently illiquid. And at last count, there were 58 ETFs based on that market. And these ETFs are absolutely ripping.

So let’s tease out how this works in a down market – not a blip correction like December, but a genuine bear market. Imagine, for instance, that defaults begin to rise, signalling a potential end of the credit cycle. High yield would get hit hardest there because it represents the riskiest companies. In that case, credit spreads would begin to rise and the market would begin to sell off. People would begin pulling money out of high yield ETFs.

But eventually, you would run into a liquidity problem – meaning while the ETFs themselves are liquid, the underlying market is not. When LTCM happened, for example, even though bid-ask spreads widened tremendously in European high yield, the bids were just indicative levels. No one was willing to buy at that level. And liquidity seized up even though this market had zero to do with Russia. What happens to the high yield ETFs in that event, when people are redeeming shares and ETF managers are forced to sell? I would suspect they sell what they can, not what they want. And so the good will go down with the bad.

Moreover, market structure now is such that broker dealer inventory has dwindled significantly, while high frequency trading has increased demand exponentially. In a down market, that lack of market-making liquidity will be severely tested. And again, the risk is that it contributes to a gapping down of prices, purely because investors become panicked when they realize they have been accustomed to ‘fake liquidity’.

The Fed’s about face

I think the Fed realized this in December. A lot of people are asking why the Fed turned from hawkish to dovish so aggressively. And the undertone to the questioning is the concept that the Fed knew something we didn’t. The result was a deep inversion in the middle of the Treasury yield curve that was practically pricing in a recession.

So what did the Fed know that we didn’t? Perhaps the Fed understood that the biggest risk to the economy is not an interconnected banking system as it was during the mortgage meltdown last decade. Maybe the Fed’s worry in December and January was the now-$52 trillion shadow banking world, which poses the greatest risk to the economic expansion.

Bond ratings agency DBRS says, “A sharp rise in rates would impose sizable mark-to-market losses and diminish fund returns.” I would make a different point – that a sharp and durable drop in the value of markets tied to ETFs would impose sizable mark-to-market losses on the shadow banking industry. And that is the Achilles heel this go round.

For me, a strong dollar is the key stressor in this. Even though the Fed has turned dovish, it has done little to diminish the attractiveness of the US dollar. Other central banks are equally dovish – more so even, because the US economy remains relatively strong on a global basis. Japan and Europe, for example, are much weaker. And Europe is where I see trouble brewing in the developed economy world.

That dollar strength puts a lot of stress on dollar debtors which do not have enough dollar revenues to cover their dollar repayments. And in a world of uneven or slowing growth, this spells volatility. The Fed, perhaps, senses that. And so, it has turned dovish.

I don’t see recession around the corner for the US. The US slump in the winter could have just been residual seasonality and the impact of the shutdown. So, we might even be in a re-acceleration. Meanwhile, US equity investors are ready for Uber and Pinterest and a whole gamut of loss-making unicorn IPOs. So, for now, the mood is bullish. Let’s see how this pans out.

Caveat Emptor

Comments are closed.