Coronavirus and initial claims bogeys ahead of schedule

The US is moving quickly toward a double dip recession despite the prospect of vaccines being administered as soon as next month. The question is not whether growth forecasts ratchet down. It’s about how much they come down and what the consequences are for individuals and individual companies. The data out today on Covid-19 deaths, hospitalizations and on initial claims confirm this downbeat assessment.

Mea Culpa?

Am I too bearish for you?

I have to call it as I see it. I recognize markets are in a euphoric state, with the Dow Jones Industrial Average hitting 30,000 this week and high yield bond spreads plunging to unprecedented lows. But that’s exactly why risks are weighted to the downside.

The juxtaposition between the euphoria in asset markets and a pandemic that is shutting down economies and killing tens of thousands daily is terrifying. Those two have to be reconciled at some point. And the preponderance of evidence says they will meet somewhere in the middle – which is a fancy way of saying asset prices will come down to meet the much less robust real economy.

I’m not saying that the pandemic or its effect on the economy is permanent. And I’m not saying that there is a dark future economically awaiting on the other side. But I am saying that the pandemic matters – and that asset prices are not reflective of that.

So, this post is not a mea culpa. It’s just the opposite. I am doubling down on the notion that Europe is in a double dip recession and that the US is likely to follow. As I told you yesterday, the G4 economies’ flash PMI is now at 51.2. That’s on the verge of recession globally. And the momentum is to the downside. Asset markets will need some serious reflation to resist that momentum.

My first bogey: claims

I had to write the forgoing because an economist friend of mine was telling me how reminiscent the atmosphere today is to 2007. That’s when people like us were telling you bad things were going to happen because of the US housing market. And we were getting shouted down. Disbelief was all around — until the bottom fell out.

Is the bottom falling out now? No, but the data aren’t good. That’s for sure. Let me give you an example.

I told you the following on November 4 as initial jobless claims were plunging:

I believe we will see significant hospitalization and death rates as the fall and winter continue. And this will put a chill on economic activity, necessitating some level of government support to prevent a double dip recession.

[…]

And I expect to see this show up in jobless claims data by early December. Until then, I am still expecting the economic outlook in Europe to deteriorate into recession. The US is hanging on by a thread.

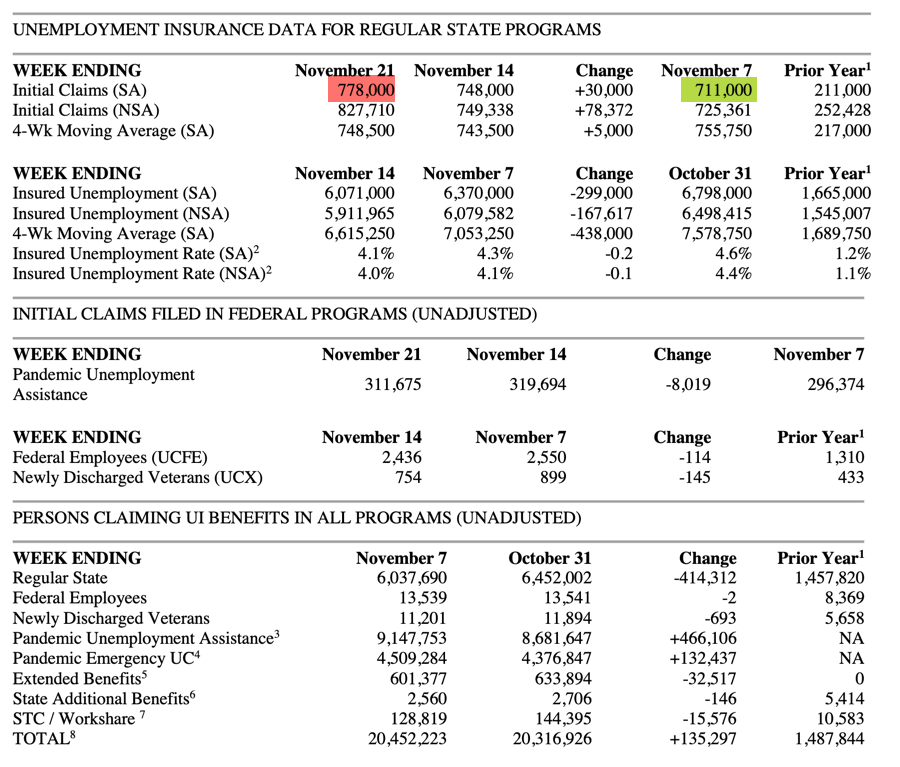

The data out today confirm this. It’s only two weeks’ data of increased claims. But look at the increase – 67,000 claims in just two weeks.

All the way back in 2008, I told you that when claims rise by more than 50,000 and stay elevated over a period of more than a few weeks, it has always meant recession. And back then, I was looking at year-over-year data because I was concerned with the income shock of a consistently higher level of unemployment. But, now the same thing is happening in warp speed because of coronavirus infections and economic rollbacks and shutdowns. The same income shock will occur, but it will be much more acute – and just as we are heading into the holiday shopping season. The timing could not be worse.

My second bogey: coronavirus deaths

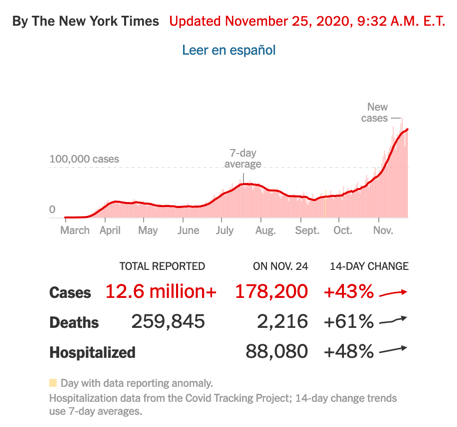

This is all driven by a poor policy response to the coronavirus epidemic. I told you on November 12 that we were likely to reach 2,000 daily deaths in the US by Thanksgiving, leading to hospital overload. We’re there now.

The 14-day change in daily case, hospitalization and death numbers is increasing too. That means the coronavirus situation in the US is still worsening, with hospitalizations setting new records for 15 days straight now. As we should expect the Thanksgiving weekend to be a massive super-spreader event with an average lag of about three weeks from infection to any deaths, I expect these numbers to go higher right into the Christmas and New Year’s holiday weeks.

These are levels that rival the epidemic levels of the Spring. And so, I expect more severe and widespread economic rollbacks and shutdowns. That means rising joblessness and business bankruptcy. Leisure and hospitality companies and workers are already seeing the negative effects. It will get worse.

My take

The questions now are as follows:

- How bad will the pandemic get before this wave can be arrested?

- How severe an economic brake will have to occur to get the virus under control?

- What short- and long-term impact will this have on businesses?

- What can and will policymakers do to mitigate downside risk and prevent worst-case outcomes?

- How will all of this feed through into asset markets?

The prevailing narrative has been bullish across these five questions. I was pilloried on Real Vision’s Daily Briefing a few weeks ago for predicting the severity of the pandemic that we are now seeing. Few people expected wide-scale economic rollbacks when I’m telling you they will get more severe. And the impact will be more severe than people expect because many businesses were already on the brink from the first wave.

My real worry is regarding questions 4 and 5 because all indications are that policymakers will be hamstrung. Look at what outgoing Treasury Secretary Mnuchin is doing to tie Janet Yellen’s hands. That’s a warning regarding the political limits of the policy response.

And finally, there is the euphoria in asset markets. People are piling into shares and high yield names indiscriminately, when there is considerable variation in the exposure to downside risk across the economy. My bet is that some of that variation is made plain in the coming weeks and months, resulting in a major sell off in the high yield bonds and equities of individual names. You don’t need to see defaults to profit from this. But where there are defaults, equity can go to zero and principal recovery for bond investors will be catastrophically bad because of covenant lite loan terms.

An all-encompassing high yield and equity drawdown is a distinct risk. And that’s not a scenario where bonds will save you unless you are super maxxed out on duration.

If you asked me, I would say I have been relatively well-balanced in speculating on outcomes because there is downside risk all around us. And that risk is now crystallizing. Am I too bearish for you? No. If anything, I haven’t been bearish enough.

Comments are closed.