The stall speed US economy and fireworks in Europe

Stalled out

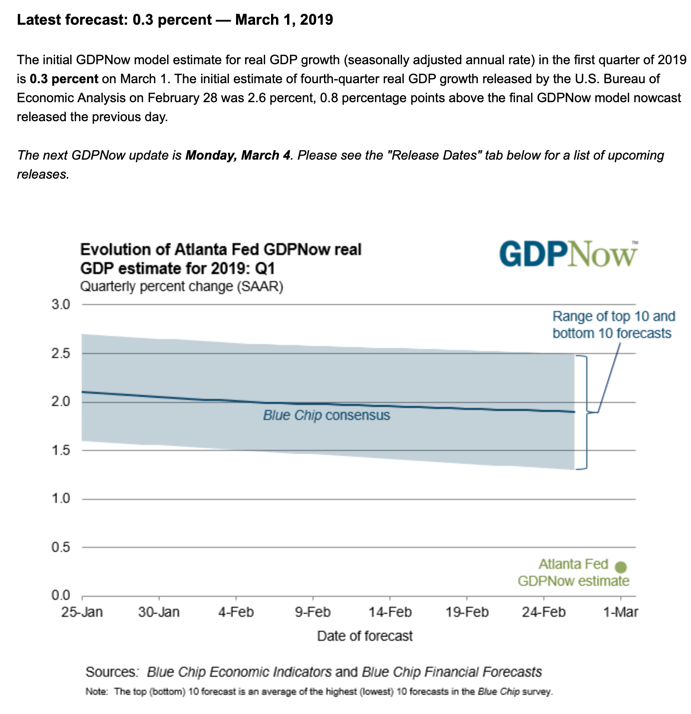

You probably saw this but the Atlanta Fed came out with its first Q1 GDPNow estimate. And it’s starting at a 0.3% level. Here’s the chart.

GDPNow is a nowcast. So it can change dramatically. And it isn’t always very close to the eventual GDP growth number. But, 0.3% is about as low as you can get outside of recession. I think my characterization of the US as being at stall speed makes sense here. Specifically, after the surprise Q4 number I wrote this:

Overall, my expectation is for Q1 GDP growth to decelerate from the Q4 2.6% figure toward a 2% stall speed level or lower. And then, we’ll have to see where we are.

Jay Powell’s about-face

It’s meaningful to note that as this deceleration is ongoing, the Fed has paused. Fed Chair Jay Powell, in remarks to Congress on Tuesday in Wednesday, said that the Fed is not just going to pause rate hikes, it is also thinking about pausing its quantitative tightening campaign…

…And so, to the degree the economy continues to slow, that will be a cushion.

Mid-cycle pause?

So, there is still a possibility here that we see re-acceleration. I’m not here to pillory the Fed even though I’ve previously said that it may come to view the December hike as a policy error. I simply don’t think the Fed was prepared for the economy’s deceleration, and was forced to u-turn very aggressively. The pivot has been so aggressive, in fact, that many people are accusing Powell of being led by markets, denting Powell’s and the Fed’s credibility.

From a cyclical perspective, a Fed on hold gives this economy room to breathe as GDPNow flatlines at 0.3% and jobless claims rise on a year-over-year basis. I mentioned that Goldman has been making the bull case here. So here’s a snippet of that via Business Insider:

The global economy may already have hit a bottom, just as popular attention turns to focus on a slump in growth around the world, economists from Goldman Sachs said this week.

Two of Goldman Sachs’ most senior economists, Jan Hatzius and Sven Jari Stehn, wrote in a note Tuesday that while global growth “remains soft,” there were “some signs that we are moving past the bottom.”

The pair added: “Some green shoots are emerging that suggest that sequential growth will pick up from here.”

The biggest indicator of this possible bottoming is that the bank’s current activity indicator — a measure of global economic activity — stands at 3% for February. This, it says, is “slightly above the downwardly revised December/January numbers.”

And this isn’t just the US. I am hearing some analysts talk of Europe’s growth also bottoming. The problem with that thesis from a US market perspective is that it seems mostly priced in. If you look at the US stock market, the rise in 10-year yields, or the fall in high yield spreads, they all show overbought conditions in risk assets and a rotation out of safe assets – perhaps boosted by quasi-momentum ETF strategies. So, when the economy really does falter, we should expect those same ETF strategies to amplify the move down.

I am still looking at Europe though

Despite all of my recent focus on the US and the UK, the real action is elsewhere. In some measure, it’s in Canada and Australia due to their unique vulnerabilities to a downturn. But, for me, it’s the institutional fragility in Europe that I have a problem with.

I have tangentially been caught up in Italian Twitter ‘swarms’ on two separate issues – one pro-EU and one anti-EU. In the first, it was my tweeting of a German study purporting to show Italy was the ‘biggest loser’ in the eurozone. See here.

The pro-EU camp saw the story as fatally flawed and saw any promotion of it as “an attempt at misleading readers and generating fake news!”. And a swarm of pro-EU Italian twitter people started attacking my tweet. I blocked a prominent pro-EU Italian economist on Twitter as a result.

Later, I saw the negative response to a seven year old tweet of mine about bail-ins from Claudio Borghi, a Lega member of Italy in Tuscany, who I follow, being prominently retweeted. I suspect it’s because Lega forces are now actively railing against the bail-in mechanism Brussels has instituted. And, yes, it is deficient. See my follow-up tweets from the last tweet in the thread here.

But, the way I got caught up in this discussion tells me that the way thus is playing out in Italy is combustible. The present bail-in mechanism is unworkable in a country like Italy that has a fragile banking system because the lack of a pan-European backstop for deposits or government debt makes contagion via bank runs or exploding interest rates a real problem. Mario Draghi’s “Whatever it takes” quip was improvised. It’s not a policy. Europe will be tested again.

And the crazy thing here is that it’s Deutsche Bank, a German institution, which is most obviously suspect regarding capital adequacy among large systemic institutions. The Germans have already bailed out NordLB, in potential contravention of the bail-in rules regarding state aid. And now they are talking about merging Deutsche Bank with Commerzbank to form an even bigger and systemically weak institution. It smacks of hypocrisy and greatly mirrors the Japanese approach to a banking crisis.

The Italians see this and are justifiably enraged. And now it’s playing out on Twitter in such a strident way that even I, as a non-Italian speaker, am getting caught up in. To me, that spells trouble down the line. So if this isn’t a bottoming process, Europe remains where you should be watching for fireworks.

Comments are closed.