Bullish ISM data and some thoughts on stall speed

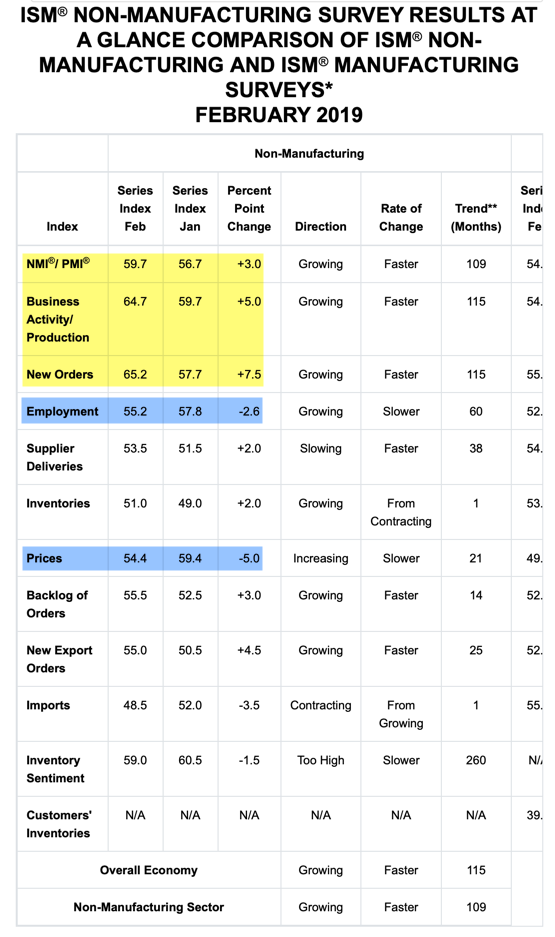

The February 2019 Non-Manufacturing ISM data were very bullish. Both the headline and the major subindices showed a lot of strength. And for me that indicates the 0.3% number on the Atlanta Fed GDPNow tracker will move up markedly as more data become available. Some expanded thoughts below

Is this re-acceleration?

Here’s the chart of the data.

The big question the data force is the one about the US economy bottoming. Goldman says GDP growth in Q1 will still come in at 0.9%. And they call it a “GDP pothole”. That’s for three reasons: “residual seasonality, the government shutdown, and tax refund delays.”

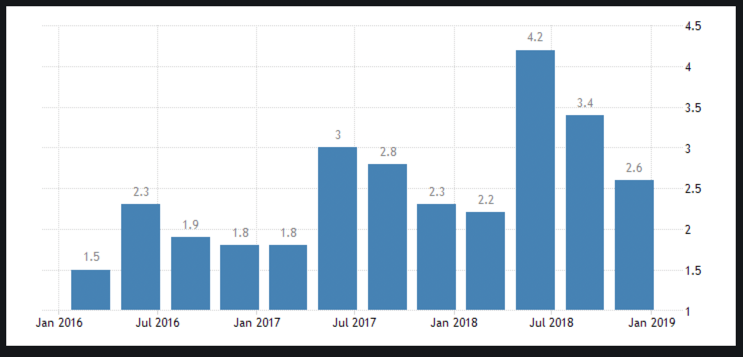

I mentioned the seasonality issue last week, saying “there may be some residual seasonality in the figures, with growth rates declining every quarter from the April-June quarter in each of the last three years.” This chart shows that:

Source: Trading Economics

However, we also know that the shutdown dampened growth. And so the February ISM NMI data could be showing a big snapback due to that factor. Honestly, we won’t know until midway through Q2. And so, it stands to reason that the Fed will be on hold here until then, even if we get more bullish data. However, if this is re-acceleration, the Fed would have a green light to move off the fence and make good on its existing rate hike forecasts.

What is stall speed?

And that last point gets us to the issue regarding what constitutes a faltering economy that the Fed should pause for. I have been saying that 2% growth is a stall speed threshold. And the 0.3% Atlanta Fed GDPNow print seems to confirm that. If we were growing at 2%, yet printed 0.3% due to the exogenous shock of a government shutdown, it says that 2% is low enough to tip the economy into recession due to shocks. But is it?

After I wrote yesterday’s piece, Tim Duy told me he takes issue with that framing. His point is that trend growth has been 2% since the Great Recession. And that’s true. We only hit 2.9% last year because of the Trump tax cuts. And arguably, the impact is already dissipating. So, “stall speed” can’t be 2% if trend growth is 2% – especially given the fact that we have been at that trend for the entirety of a long business cycle.

Tim says we need to get comfortable with the idea that GDP growth might tip into negative territory on isolated instances — even outside of recessions. He also says that the amplitude of GDP growth variation has been relatively high since the Great Recession, though it’s been lower in last few years. In his view, it is probably going higher right now, with the first quarter perhaps one of the weakest since the Great Recession. He also pointed out that we have had three quarters of negative growth since 2010. Before now, that hadn’t happened outside of a recession.

So, I need to re-think the concept of “stall speed” and its utility as a way of looking at susceptibility to recession. Having said that, I would point out that the ISM data showed both employment and inflation pointing down, even as the other subindices moved well into bullish territory. Something doesn’t add up there. And I continue to see employment as showing weakness that could prove the economy’s Achilles Heel.

The bottom line, though, is that the data coming out of the US are still some of the best in the advanced world. And there’s no firm indication that this will change abruptly.

Comments are closed.