The Fed basically has to cut now

The latest jobs report out of the US was relatively poor. While the comprehensive U-6 unemployment rate went down to the lowest since 2000, other data points suggested the labor market is topping. And with bond markets already predicting a need for two cuts this year, the Fed has to cut this summer or face huge market volatility, likely followed by a recession – for which it will be blamed.

The jobs numbers in context

Per the report, nonfarm payrolls (NFP) rose by just 75,000 in May. That’s well off consensus expectations for 175,000 to 185,000. That means that, in the first five months of 2019, the US economy added an average of only 164,000 jobs, down from the average 223,000 for 2018.

Meanwhile wage rates fell unexpectedly. And while the year-on-year increase in average hourly earnings is still a robust 3.1%, the data are weak enough to give the Fed a green light on rate cuts. Implied forward rates for Fed funds show a 78% probability of a first rate cut in July, with the chance of another cut in December now at 60%.

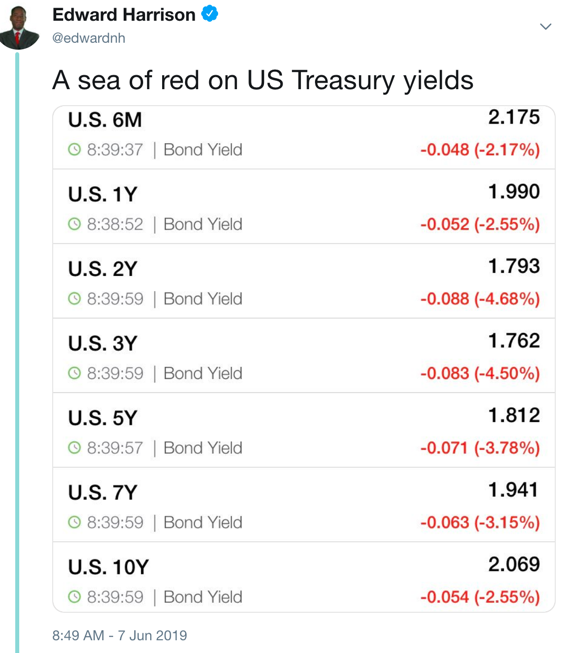

In the bond market, we have over 50 basis points of inversion, even as the yield at the short end of the curve dips in anticipation of cuts.

But, it’s not just bonds pointing to downside risk. Copper prices are down from early year highs. Crude oil is now in another bear market as inventories pile up. The economic deceleration is real.

Meanwhile in equity land…

The sentiment in equities is very much at odds with what we see happening elsewhere. We’re getting a nice rally in shares today due to the likelihood of a Fed rate cut.

Some tidbits:

- Shares of Barnes & Noble rose some 30% after it was reported that Elliott Management was interested in taking the company private.

- Beyond Meat shares rose more than a quarter after it beat expectations for its first quarterly earnings report that followed its IPO this winter. That’s because the loss-making company gave guidance that showed revenue more than doubling this calendar year. People are still favoring growth over value.

- According to investing.com, “Advancing issues outnumbered decliners by a 4.49-to-1 ratio on the NYSE and by a 2.46-to-1 ratio on the Nasdaq.”

- And they also say that the “S&P index recorded 95 new 52-week highs and no new low, while the Nasdaq recorded 65 new highs and 27 new lows.”

The bulls are back!

My view

As always, I have to stress that I continue to see the data as not pointing to recession in the US. So, all of the bond market angst we see is anticipatory. And it is very much at odds with the equity markets. Equity markets see a growing economy with low unemployment and decent wage gains that will be bolstered by rate cuts. Bond markets, on the other hand, see risk from Fed inaction in the face of decelerating growth and trade uncertainty.

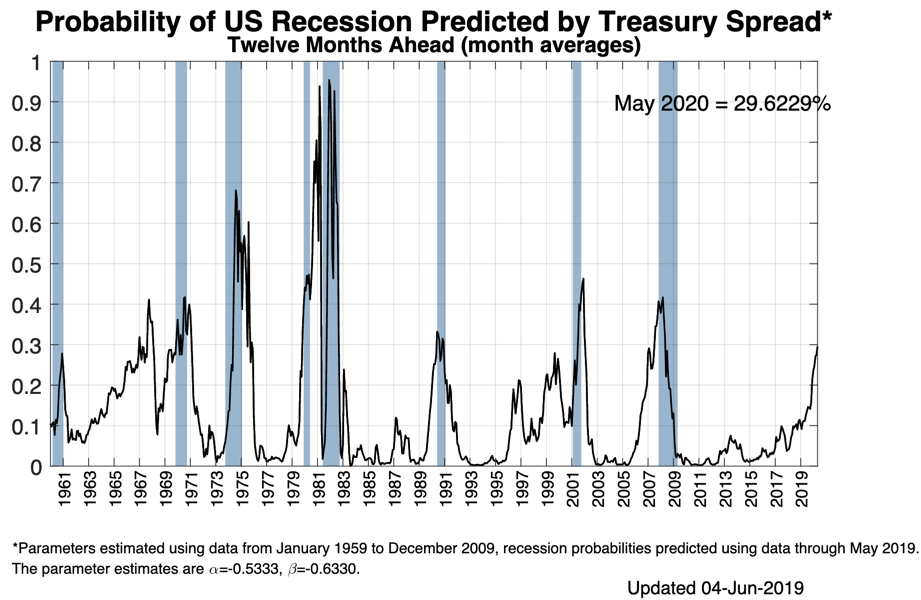

I am a bond guy. So, of course, I am worried. As I mentioned earlier in the week, my base case is now speculatively for recession by the end of 2020. Only once has the probability of recession as predicted by the yield curve been as high as it is today without a recession following. And that was way back in 1967 and 1968.

Source: NY Fed

The Fed needs to heed this warning. Yield curves are just indicators. They are warnings of the prospect of Fed over-tightening, not ironclad markers of imminent recession. So, policy has a chance to catch up here.

For me, the big problem, though, is not the Fed. It’s on the fiscal side, where all the bullets have been shot and the gun chamber is politically empty. In fact, with Trump talking about tariffs left and right, you could make the analogy that the gun chamber does have a bullet or two in it. But the US is now pointing the gun at itself.

Comments are closed.