Six topics I am following which will impact economy and markets (part two)

As I write this, the Dow is down about 450 points. And from what I can tell, people are still framing why the markets continue to slide as being about trade. I don’t think trade is the issue at all. It’s just an excuse for jitters. This is a market that is worried about the direction of the economy and the Fed’s reaction to that direction.

And so, as I start part two of my daily missive, the partial yield curve inversion is top of mind.

Just to remind you where I left off, I had six topics that the news flow was yielding where I saw downside risk:

- The Cold War 2.0 with China

- US trade with China/NAFTA

- Monetary policy

- Earnings and IPOs

- Regulation of big tech

- Brexit

Right now we are half way through the third, having covered Canada as leading American monetary policy into standing pat.

Curve inversion, rotation into government bonds, and downbeat demand suggested by oil and commodities

Yields are down again today. The benchmark 10-year US Treasury is trading at 2.87%. That’s down almost 40 basis points from the level that began market volatility in early October. And the curve remains partially inverted today, with both 2- and 3-year yields higher than 5-year yields.

Think of this as a risk-off move as recognition grows that people are underweight Treasuries and overweight risk as the credit cycle turns down. If you look back to what people were saying during the last bout of volatility, it was that we are were entering a secular bond bear market. Ray Dalio was saying it, Jeff Gundlach, Bill Gross and even Alan Greenspan. I never bought into that narrative. And now we see why.

What’s happened is that the economy accelerated mid-year. And the Fed became more aggressive in tightening, eventually raising both short- and long-term Treasury rates. But now, the risks of this tightening derailing the economy have become palpable. And everyone is ducking for cover, buying back into safe assets after having loaded up on risk.

Now, Fed officials keep talking up the near-term economic outlook. In the last week, Clarida, Powell, Quarles, and Williams have all made bullish comments about the economy. And I think the numbers for Q4 should hold up well. The Atlanta Fed’s GDPNow tracker is running at 2.7% for example.

But, there are lots of signs of flagging demand, not just in housing and autos, but in market prices of oil and all the other commodities. The Thomson/Reuters CoreCommodities CRB Index peaked all the way back in May.

And while we got a secondary lower top as October began, not only did we fail to see new highs, but the bottom basically fell out. We are now at the bottom of the 52-week trading range. That doesn’t speak to a robust global supply-demand backdrop.

Earnings and Equities

The curious thing here is that earnings have been solid. But, according to Bloomberg, Goldman is saying that “slowing economic growth, shrinking central bank balance sheets and continued bouts of volatility will help make 2019 another poor year for risk-adjusted investment returns, with few obvious havens”. Goldman’s point: “Expect better but still low returns in 2019”.

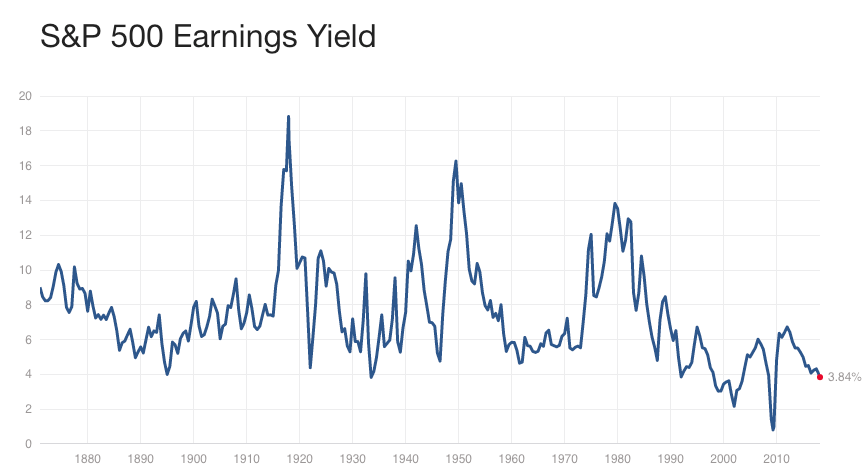

I would be sceptical of this, since sell side strategists are notoriously bullish. They never call a bear market. Still, a lot of the downdraft recently has been multiple contraction, with the S&P500 trading at 21.74 times trailing 12-month earnings, compared to 24.97 times as the year began.

Ostensibly, that decline has been predicated on rising rates. But with the 10-year down 40 basis points in the last two months, it isn’t clear what the future path will be. That uncertainty is driving volatility.

Leverage and IPOs

I would also note here that corporate leverage is high. And while corporate leverage is high, it is much higher in the speculative spaces (where oil and gas companies play). Just looking at my former industry, high yield, Moody’s recently noted that there are an “alarming” number of private equity-backed companies with poor balance sheets. 40% of junk-rated companies have been rated B2 or lower.

For PE-backed debt issues, it’s much, much worse. 90% are B2 or lower, with year-to-date debt to EBITDA figures averaging 5.x. By way of comparison, the post-bust decade-low was 3.8x in 2009. But, in 2007, the average debt-to-EBITDA figure was even higher at 6.1x.

Caveat Emptor.

Does that make it a good time to release an IPO? I think so, because time is running out on this bull market. And Lyft’s announcement that they plan an IPO after the last $15 billion valuation seems well-timed to me. According to Reuters, Lyft’s IPO will happen sometime in the first half of 2019. It will be interesting to see how it goes.

Facebook sucks

Speaking of tech, Facebook is running into a heap of trouble. The UK Parliament seized cache of Facebook internal papers. And they found Facebook discussing ways to cash in on user data without users knowing. And I see this as a critical point where, basically all trust in Facebook has eroded and regulation is going to be seen as the only way to neutralize their threat to privacy and competition.

Look at the things Facebook did:

- Facebook targeted competitors like Vine by limiting access to Facebook data (anti-competitive)

- Facebook considered collecting text message and phone log data (privacy)

- Facebook considered accessing phone logs without a ‘permissions dialogue, potentially making users unaware of the data suck (trust)

- Facebook monitored competitors with its ‘security’ VPN app Onavo (anti-trust)

- Facebook gave specific companies like Netflix and Lyft special data access (privacy)

The list goes on and on. The company is a menace. Basically, they want as much of your private data as they can get. And when they get it, they want to make as much money off of that data as they can, whether through advertising or giving third-parties access to that same data. There is really no privacy on Facebook. They know more about your private life than the government.

The blowback on this is going to be big – and not just for Facebook. It will affect all of the big tech companies, which are mostly American. And we can expect other countries to lead the way n this battle, as they have no allegiance to Facebook. In fact, taking Facebook to task is something that will build credibility with the electorate in Europe.

Brexit

And since we’re talking about the UK, I have to mention Brexit – if only in passing. I found this from the Conservative Home website interesting:

It is far from certain that there is or will be a majority in the Commons for the abandonment of Brexit – the real aim of the second referendum campaigners. But it is increasingly possible to imagine that there might be, and that this Government would then seek both to postpone the leaving date and to enact just such a referendum. Theresa May is in breach of so many previous positions that for her to follow the impulses of an instinctively pro-Remain Commons would be a logical next step…

At any rate, our latest survey results are a reminder that any such grandmother of all U-turns would have very serious consequences for the Conservative Party, outside Parliament as well as within in.

Nine out of ten party activists are opposed to a second referendum. If Downing Street or CCHQ thinks that these members would all meekly turn out to campaign for the Party in the wake of any push from the leadership for a second referendum, they might want to think again. Certainly, many of them would turn out against Jeremy Corbyn in a general election. But not all. The immediate aftermath of a U-turn would be torn-up membership cards, cancelled subscriptions, less money and fewer boots on the ground. And as both the 2015 and 2017 elections demonstrated – positively and negatively in turn – having campaigners in the right places counts. Some of these disillusioned Tories might cast around for a new, credible UKIP. Most would simply sit on their hands.

Marshall Auerback sent me the following article in the Guardian titled: “I drafted article 50. We can and must delay Brexit for a referendum“. Here’s the key bit:

This week the advocate general of the EU’s court of justice published advice to the court about the revocability of the UK’s withdrawal from the EU under article 50 of the EU treaty. He has confirmed that we have an absolute right to change course and take back our withdrawal notification without paying any price – financial or political.

I admit this is something of a specialist subject for me: I was secretary general of the European convention that drafted the article. I have always believed that nothing in it restricted our rights as a full EU member to change our minds, stay in and keep all our current rights, privileges and opt-outs: Margaret Thatcher’s budget rebate, John Major’s exemption from joining the Euro, Theresa May’s opt-in to the European Arrest Warrant and Europol.

My view: This is headed toward the UK revoking its use of Article 50. The ECJ has said they can do so. And within the UK and the conservative party, there is no deal that will satisfy enough people to pass the House of Commons, who have a right by British law to vote on any deal with the EU.

So what I think will happen is that the deal Theresa May made will fail, whether by formal vote or delay, it doesn’t matter. But afterwards, the UK would be sent crashing out of the EU with no deal unless it pulled the trigger on revoking Article 50. And the risks are too great. Too many people are against a ‘no-deal’ Brexit. It won’t happen. And, of course, there are a lot of downside risks here.

Last words

So that’s my news scan. There are a lot of things going on right now. And uncertainty surrounds all of it, from China-US trade and NAFTA to the economy and monetary policy to regulation and Brexit. I think there is more uncertainty surrounding these issues than is usual. The downside risk for each of these scenarios individually and collectively is considerable. And, this has made markets jittery.

2019 is going to be a big year because this is when the end game for this cycle will become clearer. But I believe getting to that clarity will be tumultuous. We are just beginning to see that.

Comments are closed.