US: Declining savings and deleveraging leads to releveraging

This is a quick post to go along with my twitter rampage from just a few minutes ago. The US released its economic data and it showed personal consumption outstripping GDP growth and income growth. I believe this trend is worrying. Below are some reasons why.

First, here are the relevant seasonally-adjusted data. Real US GDP grew 2.4% on an annualized basis in Q1. This growth was underpinned by strong consumption growth as consumer spending grew 3.4% on an annualized basis. That’s what we heard from the US Department of Commerce this morning at 8:30. What we also know is that the US Department of Labor reported real average weekly earnings growing only 0.8% between April 2012 and April 2013.

I would summarize the US macro picture by saying that consumption growth is outstripping GDP growth which is outstripping wage growth in an environment of relatively weak job growth and rising asset prices.

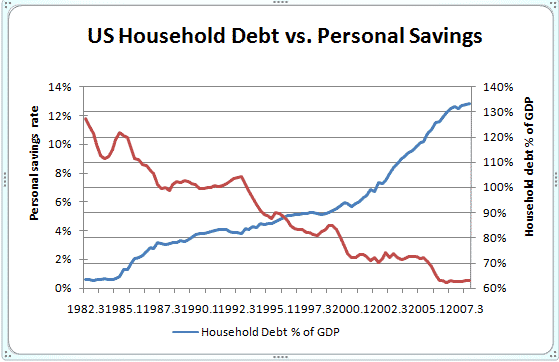

Five years back as the financial crisis was reaching a critical state, I posted a chart which encapsulated my macro view on the US household credit binge over the past few economic cycles.

When I see this chart, I see a secular trend created by asset price inflation. What I am seeing is asset price inflation allowing a general household leveraging and lower savings due to wealth effects. This all came to an end when the housing bubble popped as cautionary savings and deleveraging started.

On that front, the precautionary savings has reversed trend while the deleveraging one has not. Savings peaked at about 6pc of GDP and has since declined to less than 3%

On deleveraging on the other hand, household debt is still declining. In Q1 2013, it reached 2006 levels:

“Household debt fell to $11.2 trillion in the first quarter compared with a peak burden of $12.7 trillion in the third quarter of 2008. Consumers reduced debt by $110 billion after increasing their borrowing by $31 billion in the fourth quarter of 2012, while delinquency rates fell “across the board,” the Fed district bank said in a statement. Student debt bucked the trend, rising to a record $986 billion.

“Household deleveraging has resumed its previous trajectory,” Wilbert van der Klaauw, a senior vice president and economist at the New York Fed, said today in a statement. “We’ll look to see if this pace of debt reduction and delinquency improvements will persist.””

I don’t see how the household deleveraging trend can continue in an environment of lower household savings rate and still weak income growth from combined job and wage growth. Likely, the lower savings rate presages a releveraging. And I see this as a dangerous possibility.

What I am saying is this: economic growth predicated on wage growth is sustainable. However, economic growth predicated on asset price inflation-fuelled consumption is not sustainable. I am very concerned that the US policy mix is bringing back the asset-based economy and that this will end in a nasty deleveraging-wracked recession. Housing is fuelling this. And while you can’t call a 10% rise after a 30% drop a bubble, people like economist Dean Baker, who called the last bubble early, are seeing trends that look unsustainable.

Economic growth is good. But what we want to see is job and wage growth to complement the asset-price growth. Without this catch up on the job and income front, the economy is on an unsustainable course.

Comments are closed.