The numbers

Now, about the jobs numbers, here are the headline numbers:

- An increase of 312,000 in December in non-farm payrolls based on the business survey. That is well in excess of the consensus estimate for 178,000.

- Revisions of +58,000 to October and November payroll data, bringing the net up to +370,0000 for this month’s business survey

- An unemployment rate of 3.9%, up from 3.7% based on the household survey. That compares unfavorably to the anticipated 3.7%.

- An increase in the Labor Participation rate to 63.1% from 62.9%, based on the household survey. That is what caused the unemployment rate to increase.

- An increase in average weekly hours to 34.5 from 34.4 the month prior. That is in line with expectations

- Average hourly earnings up 0.4% on the month, bringing the year’s gain to 3.2%. That’s above the expectation for 0.3%

- An increase in manufacturing payrolls of +32,000, above the expectations for +20,000 and assuaging worry about yesterday’s Manufacturing ISM survey

What I think about the numbers

These are good numbers. +370,000 is the baseline number to focus on. And that’s more than double the expected payroll gain. It tells you the US labor market is still not just robust but robust enough to add lots and lots of new jobs. And while that number doesn’t speak to the quality of the new jobs, the 3.2% gain in average hourly earnings plus the slight bump in hours worked show that people are making more money.

People will tell you that jobs are a lagging indicator. But I have found that this isn’t strictly true if you look at job gain trends or at jobless claim trends. It’s not the absolute number but the trend, the change in the number that matters. And right now, we are adding more jobs, year-on-year.

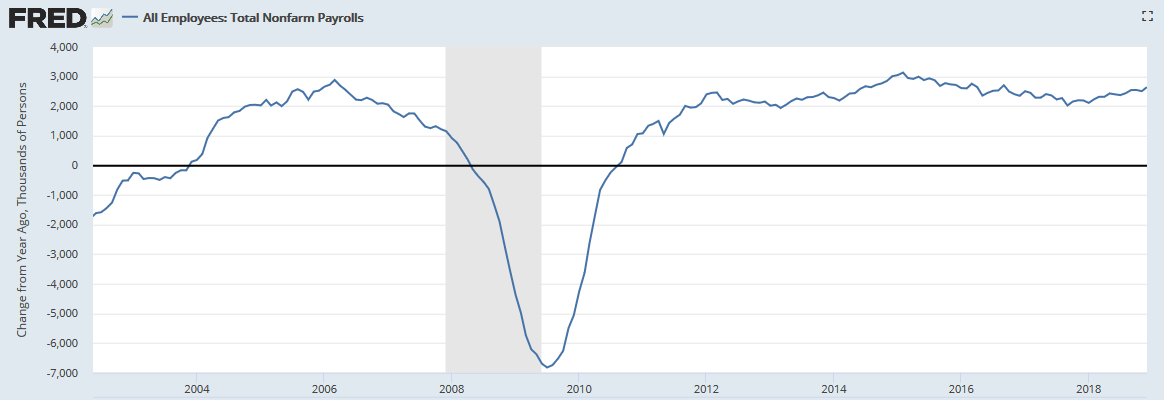

Source: St. Louis Fed

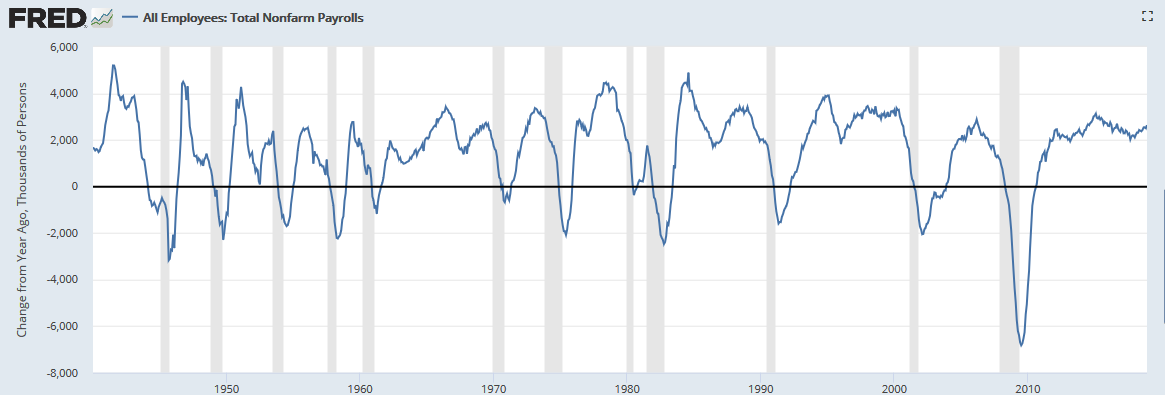

Source: St. Louis Fed

The gain is 2.64 million in the past 12 months, the best number we’ve seen since September 2016. And historically, year-over-year job gains are falling when recessions hit. See the long view below.

Notice that the number has turned down before a recession hit every single time. Now sometimes, there has been a peak and then a smaller secondary peak right before recession as in 1953, 1970, 1990, and 2001. But, as yet, we have never seen a recession while year-over-year job gains are rising as they are now. Never.

We have also never seen a secondary peak higher than the first peak. So I believe we are not likely to surpass to the February 2015 peak of 3.13 million. More likely, year-over-year job growth will begin to stall soon. And soon afterwards, recession will take hold. That’s my baseline.

And so I am looking for year-over-year job growth to peak some time in 2019. In that sense, this particular data series is backward looking. If we look ahead, we see the numbers peaking soon and then declining.

The market

The market’s reaction was over the top in that context, both for stocks and bonds. I will have more to say about that in a post to Gold members later. But the gist here is that we what we saw today was yet another big relief rally. Everything now is about volatility until it’s clear we are headed to a recession at the end of the cycle or into another mid-cycle pause.

Jay Powell’s comments today on the market helped calm investors who were scared the Fed would push the economy over the edge. So that’s a big part of why markets reacted as they did. Notice that Treasury yields went way up today, with the long end of the curve selling off more than the short end. This isn’t a story of more interest rate hikes feeding through into the long end of the curve. It’s a story of the market believing the Fed will be moderating its approach going forward and sending yields up and making the yield curve steeper on the premise that this business cycle has legs.

That is a clue to you that higher rates and a steeper curve can actually mean positive things, where lower rates and a flattening curve are ominous.

Overall, I am a lot more sceptical about where both the Fed and the economy are going for the rest of the year. But, at least we have some bullish real time data to contend with. We should be thankful for that.

Comments are closed.