Bullish news on the US jobs front

Real quick on this Good Friday

The US jobs report for March was superb. We got everything we wanted to see except an improvement in hourly earnings. In my view, this report bolsters the case for upside risk for the economy and inflation and mitigates lingering doubts about downside risk in the near term. That’s bearish for bonds. The impact on equities is less clear.

As for the numbers, here are the ones I care about:

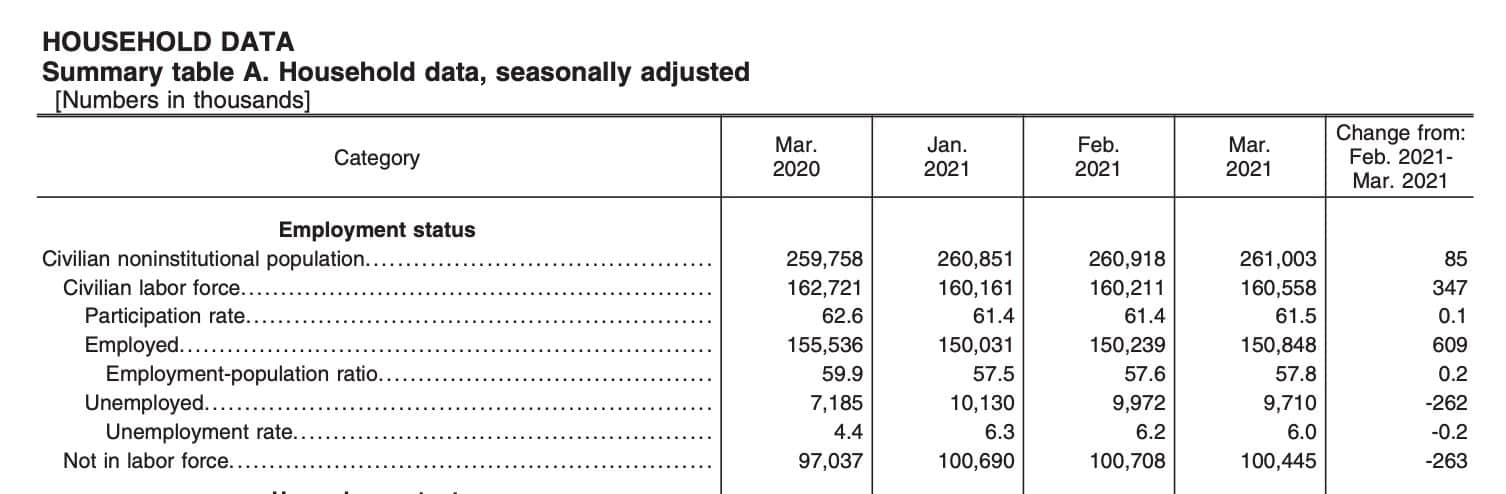

- 916,000 jobs created in March in the US versus 647,000 expected and the 517,000 private sector payroll addition from ADP on Wednesday

- January and February revised up by a combined 156,000. That means we saw a combined 1,072,000 jobs added to payrolls in this report

- Headline U-3 unemployment rate fell to 6.0% from 6.2%.

- Higher labor force participation (inched up to 61.5%, 0.1%)

- Employment-to-population ratio was also up (57.8% versus 57.6% in February)

Things that are bad:

- The overall labor force participation rate is still more than a percentage point below pre-pandemic levels

- The number of people not in the labor force is still 3.4 million higher than a year ago

- The labor force participation rate for the prime working-age population (25-54) is STILL lower now than it was in June

- The March 2020 unemployment rate was 4.4% and we are still at 6.0%

- Average hourly earnings declined 0.1%

My view

The US labor market still has room to add jobs. The question now is about the pace of that addition. We have been on a reverse radical course, with a V-shaped bounce off the pandemic lows when we re-opened in the summer of last year. However, since then progress has been slower and more halting, in part due to repeated spikes in virus infections. This report shows you that you can add a lot more jobs when the economy is not hobbled by viral infection and when there is significant stimulus goosing the private sector’s net financial assets via deficit spending.

We are about to enter hopefully the last big wave before the vaccination process protects the majority of Americans. 3 million people are being vaccinated per week now. So it’s not long before we have near so-called herd immunity. But, judging from healthcare system overloads in places like Michigan, we will not escapee the mutant virus wave unscathed. It will likely be worse in Canada, which is slower in vaccinating.

My expectation is for the pressure on bonds to continue due to economic news of this ilk. We made a run for 1.75% on the US ten-year but are trading almost 5 basis points below that level now.

In a Goldilocks scenario, we continue to churn at these levels before the full re-opening and that supports the reflation trade including companies with the majority of their discounted cash flow earnings further out into the future like technology and growth stocks. But I think we push higher due to the Fed’s insistence on not admitting it can and will raise base rates due to the economy’s improvement. The market will force the Fed to react. That’s my expectation. And so, I continue to expect value to outperform growth.

In a reasonable worse case scenario, inflation perks up enough to push yields up such that Q2 adds to Q1 in terms of pain for Treasuries. Q1 was the worst quarter on record in that market since 1980. And two consecutive bad quarters would assuredly mean a hit to growth stocks, enough to cause the overall market to fall. The Nasdaq is leveraged to growth stocks. And the S&P500 is leveraged to the FAANG stocks, which in a reasonable worst case would take the whole S&P down with them, as yields bite.

Great report. Keep it coming

Comments are closed.