Thinking about the blowoff top

Oh, how the world has changed!

The threat of a mutant-inspired viral wave and lockdown still lurks in the background, yes. Even so, the balance of risks is now completely tilted to the upside in the US economy. And that means we have to explore those upside risks. What a change this is.

Risk balance framing

When was the last time we had a sustained bear market in the US that wasn’t fueled by an economic downturn? That’s a serious question because I know my economic and financial market history pretty well. And I can’t think of any cyclical bear markets that happened outside of recession that weren’t erased in short order.

I ask that question because that’s the most important one in terms of framing. So let’s start there.

I told you back in June when the US economy re-opened that the recession was over. And, with the aid of hindsight, I would now say that’s undeniably true. So, absent a shutdown-induced double dip, we’re nine months into a new economic cycle right now.

And, increasingly, I question whether a new shutdown could even induce a double dip given how we’ve acclimated to the virus economically. The second revision of Q4 GDP growth released today confirmed that the annualized pace was over 4% despite shutdowns in December. The second estimate did tick down marginally to 4.1% from 4.2% annualized. But that’s not a meaningful change. The reality is that the US economy acquitted itself well through a rolling lockdown.

That’s telling you we’re in the clear. Double dip is not the base case by a long shot. The risk is completely on the other side.

Some numbers

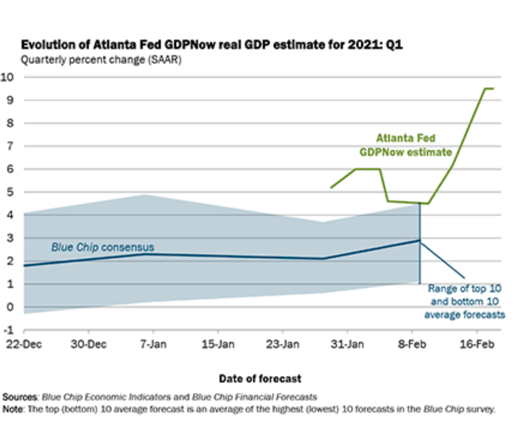

I was talking to a group of economic and financial market analysts in a Webex during lunch yesterday. And my friend Marc Chandler of Bannockburn Global Forex reminded us that analysts are busy ratcheting up Q1 growth forecasts. He mentioned 6% as a target. I checked the GDPNow nowcast and saw the latest figure tracking at a gargantuan 9.5% annualized.

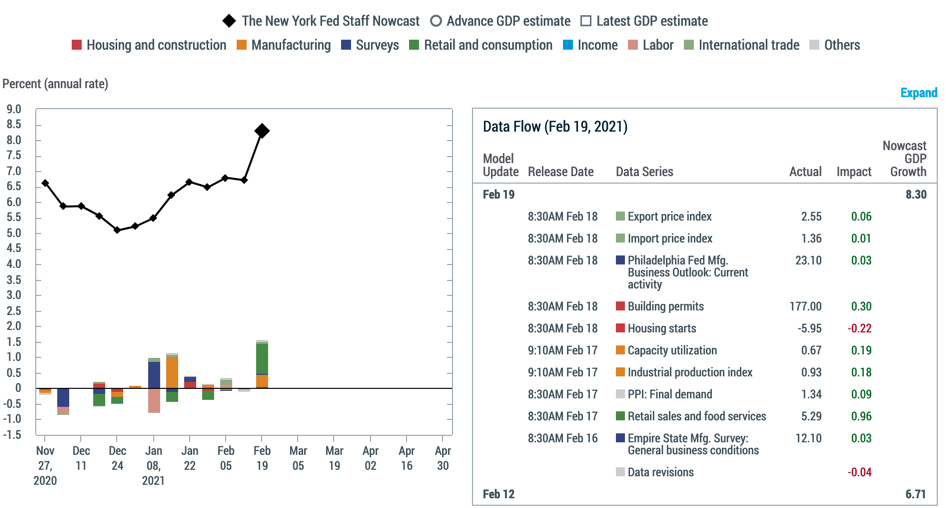

I am waiting the inclusion of today’s upbeat durable goods figures to see how the number is adjusted. But, the Blue Chip consensus the Atlanta Fed is using is only at 3%. That’s a lot of gap to close. Moreover, the NY Fed is talking about the Q1 releases having GDP track 8.3% annualized.

And this is before any new stimulus hits the economy. Taking that into account, PIMCO is talking about the whole of 2021 coming in at 7%.

????”Pimco, one of the world’s largest fixed income managers, said in a research note that the additional stimulus could ‘contribute to 2021 real GDP growth of over 7%,’ a level not seen since “the great inflationary episode of the 1970s-1980s.” https://t.co/wZb6zkOKOR

— James Pethokoukis (@JimPethokoukis) February 25, 2021

These are very big numbers.

The bond market

So as I assess what all of this means – especially in the face of a US equity market that looks overvalued – I find it hard to see a lot of downside for equities. Despite the overvaluation on most traditional valuation metrics, the reality is that we are in a recovery that is likely to be goosed by an additional $1.9 trillion in stimulus shortly.

And Deutsche Bank is saying that the stimulus checks associated with that stimulus could cause inflows of $170 billion into markets, as respondents to a survey estimated they would drop 37% of their stimulus checks into public-market investments. You don’t get durable equity bear markets during 7% growth with new money pouring in.

That’s the backdrop for the selloff in the bond market. As I wrote yesterday, the outcome I am expecting is a stair-step move higher in global yields until one of three things occurs.

- Policy makers could start to move against the higher yields. The ECB is jawboning. But yesterday, the Reserve Bank of New Zealand doubled down on its stimulus pledge as forward guidance. And the Reserve Bank of Australia has already re-started bond purchases to hit target yields.

- Yields could also move so high that they destabilize markets. But, as I wrote in August when laying this thesis of “Momentum stocks as a long duration secular stagnation play“, “It’s not necessarily a down market per se. You could see a rotation out of growth into value due to a reflation-associated rise in inflation expectations and rates. That means bear steepening in bond markets and increasing nominal and real GDP growth plus increased earnings growth due to GDP and operating leverage.”

- We also could have another major wave of coronavirus from the mutant strains that causes bear flattening. Increasingly though, I am discounting this outcome as a tail risk at this point.

More and more, the outcome I see for the interplay of bonds and equities is a combination of outcomes 1 and 2. You could even see another virus wave (outcome 3) that fails to unmoor the curve steepening trend (outcomes 1 and 2) because we are so advanced toward a full re-opening.

Right now, yields are moving so high so fast that we are likely to see them take a breather. Resistance around 1.50% is the next level to watch. If we break through and consolidate above that level, we can go higher still. I am increasingly thinking of this rise in global rates as a policy frontrun of global nominal GDP growth. And policy makers have to decide how they will react.

My view

So, for those of you making comparisons to 1999, you might have to re-consider. It certainly feels very late cycle in terms of the speculative nature of markets. but it’s not clear to me that the end is nigh so to speak. We could hit an air pocket due to the rise in yields. But unless that spills over into an end of the credit cycle, I think this is just a temporary setback which will have the aggressive Millennials and the passive investors buying the dip.

The risk here is a blowoff top a la 1999. Can a blowoff top induce a cyclical change in credit and the real economy? I don’t know. But, that’s really the only way we get stopped out on our way higher now. PIMCO is right to think about 7% growth for 2021. And that’s a bullish backdrop for risk assets, which are already incredibly extended.

Comments are closed.