Two alternative takes on the recession and on coronavirus

Real quick here as I want to highlight two other analysts’ thinking. This morning, I saw two novel ways of conceptualizing what’s happening during this pandemic that I wanted to run by you because I think they add value. It’s not necessarily how I’m thinking about issues. But these are framings I am going to incorporate into my thinking.

The 2020 recession

Let’s start with the recession first. As you know, I’ve been claiming that the recession is over and that we could be in the midst of a durable upturn. The way I have framed it is as a definite recession start and end in the first half of the year and a recovery that may or may not end in a double dip. And as I spelled it out yesterday, the genesis of any double dip would be economically distinct from the genesis of the first dip in the first half of the year. That’s why I am looking at credit markets for warning signs. See my post here for that framing.

Well, David Rosenberg has a different take. And his framing could make sense. So I will quote it here (paywalled material; link to free trial). Here’s what he wrote this morning:

let’s not fool ourselves —organically, the economy is still in recession. And recessions only end once the government’s training wheels are taken off the bicycle.That is still quite a long time off —and why real personal income EXCLUDING government transfers is one of the four cornerstones ofhow the NBER defines the contours of the business-cycle call.And, yes, the stock market hasdone well —except for the fact that the sectors geared for the economy to remain in a “stay-at-home”state is the only reason for this… most cyclical stocks are still in varying stages of pain.

[..]

…what I’m trying to stress here is that we only know when recessions end well after the fact, and what is needed is follow-through.So all this talk of recovery after a quarter of massive fiscal stimulus and re-openings is likely premature.The bottom line is that every single recession in the post-WWII era, all ten, saw at least one quarter of GDP rebound. In fact, the mode, median and mean aretwo quarters of positive sequential GDP readings in the recession. Keep that in mind.

So, what Dave is stressing is that it’s only government largesse keeping the economy afloat. There is no organic recovery. In fact, during the 600 a week PUA period, government transfer payments caused incomes to actually rise despite tens of millions out of work. That’s an enormous make good from Uncle Sam.

In truth, I don’t think our macro views are that dissimilar even though I am calling the recession. I fully recognize that stimulus is keeping the economy afloat. But when I think back to 2009, I think of fiscal stimulus then as having kept the economy afloat too. And the NBER still ended up dating the business cycle from mid-2009.

So I leave open the possibility that we are in a sustainable recovery. It certainly doesn’t help that more and more make-good from Uncle Sam is rolling off. But the latest retail sales numbers today were a massive beat at 1.9% versus the expected 0.7%. And this came after the rolloff of the $600 per week PUA payments.

“The stronger than expected retail sales growth in September may have reflected a rebound from depressed back-to-school spending in August, as well as a boost from the disbursement of the $300 supplemental unemployment benefit provided by executive order.”

Any way you slice it though, that’s a massive beat. And it says we can’t count the American consumer out yet.

The Coronavirus pandemic shutdown response

Now, here’s something slightly more contentious. It’s on coronavirus and some comments economist Jens Nordvig recently made on Twitter about the pandemic policy response.

Let me start this out with my view first though. If you recall, early on in the pandemic Sweden was an outlier in social distancing and policy response protocols. And there was a massive loss of life there as a result. For me, the discrepancy to other Nordic countries in terms of human suffering makes clear the Swedes botched the inital response.

As I was going through the logic of policy responses in April, the shutdown was about preparedness. Here’s the logic:

…what if your own testing is inadequate i.e. you can’t test everyone, only those who want or need a test? Then, unless you rely on herd immunity, you have to start to restrict freedom of movement.

First, the science says that an infectious disease will multiply out of control unless you identify carriers and isolate them. So to the degree you have substantial doubts about who a carrier is, you are forced to restrict the movement of everyone until you can either ascertain who is a carrier…

…the sooner you shut things down, the less the virus will have already spread before shutdown. If the virus has an R0 of greater than one, it means that every second, every hour, every day, every week you delay in restricting movement is a second, hour, day and week the virus has to spread exponentially. And that means greater disruption and also greater death.

…psychology tells you that people will not self-regulate enough in a non-perfect testing environment to prevent the disease from spreading wildly. Every instance I have seen, from Miami beaches to Nashville bars to Swedish streets tells you that policy makers must, at a minimum, mandate stay-at-home orders to get compliance that will limit the disease spread.

So, the second conclusion is that in a non-Utopian testing environment, you must mandate movement restriction and do it as soon as possible. The earlier you do it, the less likelihood you have for exponential contagion. And, as a result, the sooner you should be able to lift restrictions in a non-Utopian testing environment without risking a second wave of exponential infection.

Put in this light, the shutdowns make sense. Countries were caught out by the pandemic. They were unprepared and didn’t have adequate testing capabilities to figure out who was a carrier and who wasn’t. So, caught out without the right preparation, the logical response was to shut everything down to prevent massive loss of life. Countries that didn’t do this or delayed in doing so, saw the highest death rates in the first wave. And that includes Sweden

The go-forward approach

This is where Jens Nordvig comes in.

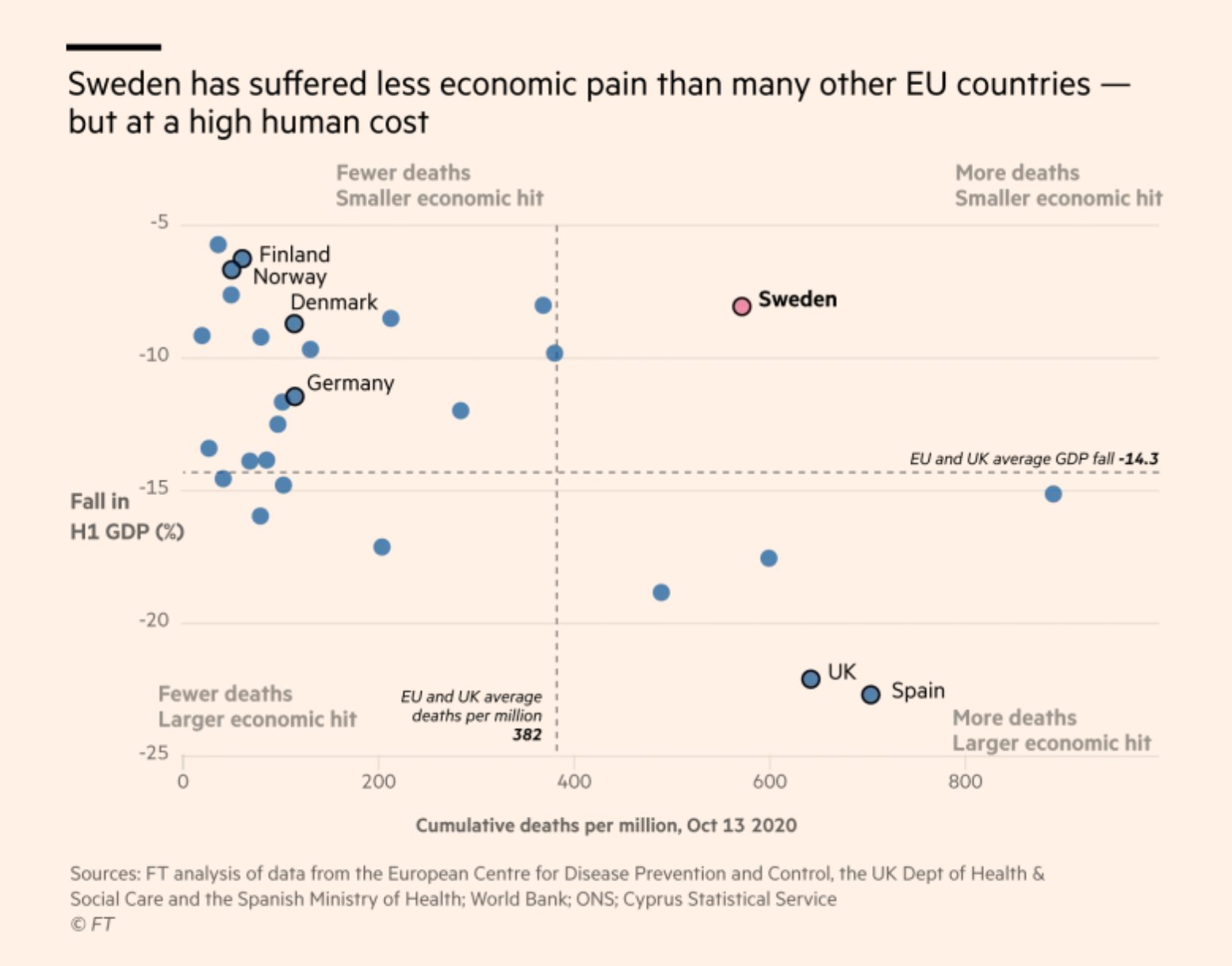

Adam Tooze tweeted the following with a chart headlining the human cost in Sweden due to their approach to the virus.

Looking at this scatter plot of Covid mortality and GDP loss across EU, rather than a trade off, you might be tempted to say that there were simply some countries that handled the crisis well and others that did not. https://t.co/O7ju9NOQXn pic.twitter.com/DVJGu5zYm3

— Adam Tooze (@adam_tooze) October 16, 2020

Makes sense.

Jens Nordvig responded, writing:

I think better to do these charts from May. The initial toll was mostly ‘an accident’ as nobody was ready, and the virus surprised. The action taken in March-April, that drove cases/fatalities after, is the real test of policy. (I can try to make it…)

— Jens Nordvig (@jnordvig) October 16, 2020

He went on to say:

I think that is fair, so look at Feb-April as a measure of ‘preparedness’ and ‘May-to now’ as quality of reaction, they will provide different and more nuanced answers than just lumping them together (there was also ‘luck involved’ in the 1st wave for some countries)

— Jens Nordvig (@jnordvig) October 16, 2020

And I think Jens is right. Sweden erred in its initial response. But in a world in which coronavirus is hanging around for the long term, their approach now makes more sense. And mortality in Sweden has not spiked the way it has elsewhere (yet). I think this is a direct result of the easier habituation from a more sustainable new normal in Sweden than elsewhere. That’s the controversial part here. I am basically saying that, since April, the Swedes have been doing it more right than we have.

Bringing this together

Where the first part and the second part of this post come together is in this self-quote from the April 24 edition of Credit Writedowns:

The latest I am hearing on the coronavirus front is that irrespective of a lockdown relaxation-induced wave, we should expect a Fall or flu season recurrence of this virus. And that means we either get better prepared now or risk death and shutdown again this Fall and in the Winter of 2021. To me, that speaks to the likelihood of a longer-term impact of the pandemic on social patterns and economic activity. And, therefore, it points to the strong possibility of L-shaped outcomes.

The Fall/Winter wave I mentioned six months ago is now happening. And what that tells you is that it was entirely foreseeable – since even I told you six months ago it was likely to happen. But, what was also foreseeable is that countries would be caught out – again. And so, that raises the possibility of negative economic outcomes as governments scramble to react and the economy takes a beating. How will Sweden fare?

More generally, will the government fiscal offset that David Rosenberg is pointing to continue to hold things up? In the US, for example, that offset is rolling off and will continue to roll off even more. In the UK, for example, we are about to see some pretty large scale regional lockdowns. What kind of government offset will that require to keep the economy from cratering?

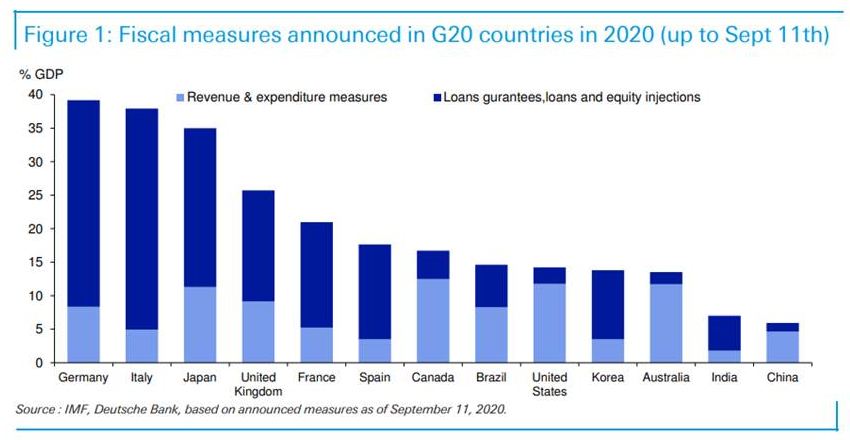

And if you look at what Deutsche Bank’s Jim Reid has calculated, we’ve already seen some massive fiscal outlays.

Italy is at 40% of GDP and they have restrictions coming as a second wave bears down on them. Germany can get away with spending 40% of GDP to prevent the coronavirus from crushing their economy without the bond vigilantes coming to tear down their house. Can the Italians spend 40% and then go back to the well for more in a second wave? And how does the ECB prevent Italian yields from spiralling upward if the bond vigilantes question Italy’s solvency as a non-sovereign Euro currency user?

These are all important questions to ask. And I suspect we will have an answer in due course.

Comments are closed.