The backside of the coronavirus storm

The eye of this economic and healthcare storm has passed over us and we are just now getting hit with the backside of the storm. And so, as I await the initial jobless claims report at 8:30 Am EDT, the question is: how bad will it be? But more than that, ‘is it priced in’? We won’t get the answer to these questions for weeks. And while I’m not qualified to give a prediction on the first, I can give a qualified answer to the second question; no, it’s not priced in.

Yum Brands and Carnival Cruise Line

Let me give you an example here. A couple of days ago, YUM! Brands, the owner of KFC and Taco Bell, sold $600 million of debt in the first high-yield bond offering in the US market since March 4. They upsized the deal from $500 million because they had $3 billion in orders, so starved were high yield bond investors investors for product.

Now, YUM! didn’t get the deal off without paying a penalty rate. Outstanding paper for the company had a coupon of 6% for a 10-year maturity. This deal was priced at 7.75% for 5 year paper. So, YUM! got its money and investors got some truly high yield paper. Everyone’s a winner, right?

Well, Carnival Cruise Line thought so too. So they came to market yesterday as well. Their parent Carnival Corp was A3 rated by Moody’s. But, it was hit hard by the coronavirus situation and needed money to make sure it had cash on hand if things get worse. So, they went on a capital raising binge, issuing 3-year bonds, a convertible bond deal and raising equity at a steep discount to market prices.

Moody’s immediately downgraded the company to Baa3, proving yet again that the ratings agencies are reactive, not proactive. That’s because Carnival, which paid 1% yield in October, when it borrowed 600 million euros, was paying 11.5% for 3-year debt. That’s almost 4% more than YUM! for a shorter maturity offering, when YUM! is a junk-rated company and Carnival isn’t. And the tell is that demand for the deal came largely from high yield investors.

Even though Carnival upsized its bond deal to $4 billion from $3 billion because of investor demand, the terms for Carnival were horrific across the board. Carnival had to use its ships as collateral, it priced the convert at 5.75% and shares fell 33% to $8.80 as it issued shares at $8.00 a share. The company says it has enough liquidity now to last a full 12 months under all circumstances. But it has paid a steep price to do so.

The investor pain coming

Think of Carnival as the Argentina century bond of 2020. Investors snapped up 100-year Argentine government debt paper in 2017 because of the need for yield and the promise of Argentine President Mauricio Macri. But Macri was a disaster who was booted from office last year, sending the bonds to 54 cents on the dollar from 74 cents the night before the primary election. Now, people are questioning whether Argentina will default again.

That’s how you have to think about Carnival. So, no, it isn’t priced in. Investors are still taking flyers on companies like Carnival;, simply because the magnitude of this downturn hasn’t sunk in yet.

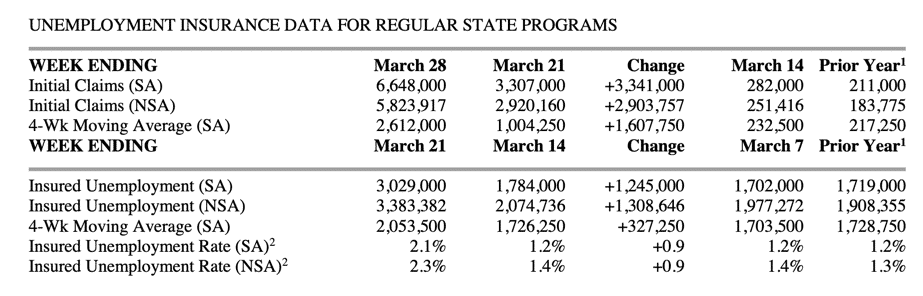

Meanwhile the latest jobless claims number was released. It was a seasonally-adjusted 6.65 million initial claims, up from an upwardly-revised 3.3 million. This was higher than even the highest estimate of 6.5 million. So, the number was horrifically bad.

Ev en so, should we even use the seasonal figures at this point though? They’re basically meaningless. The actual figure was 5.82 million.

Dow futures are up in the wake of this print. That tells you what you need to know. The equity market is oversold. The market isn’t moving based on data. It is moving based on sentiment and technicals. But when the data start to sink in as earnings crater, markets will react.

My view

I am keeping this ultra short today.

It’s clear to see that the bad data have now arrived in spades. And the markets are acting like they knew it all along, despite the fact that much of the data is worse than anticipated. I see this as a sign that markets will move down in the coming weeks as the real economy impact sinks in.

Moreover, going forward, as things start to get rough, I see the Fed making additional moves to shore up liquidity, but not into equities or high yield. And that will leave these markets exposed. Along with emerging markets, which are dollar short, these are the markets to watch for another leg down.

Comments are closed.