The Downside Risk to the Mid-2019 Macroeconomy

None of the metrics I look at are screaming recession right now. In fact, for the US, some of the data is improving. Nevertheless, there is reason to be concerned about the state of the US economy in mid-2019 – so much so that my base case is for recession by the end of next year. Let me tell you what the downside risks are that I see.

Second derivative metrics

I was thinking about this yesterday. The government’s statisticians do a great job with the tools they have in giving us an accurate read of the US economy. Take the Birth-Death model, for example. This is where the “BLS uses an estimation procedure with two components: the first component excludes employment losses due to business deaths from sample-based estimation in order to offset the missing employment gains from business births.”

That’s how the statisticians explain it. In plain English, they’re saying that small businesses are created and go out of business all the time. The employment associated with these business births and deaths are not properly accounted for in the stats. So, the government uses statistics to fill in the gap. And, in my view, they do a pretty good job of capturing this component and making their monthly jobs numbers even better.

But statistical estimates are difficult to make at turning points in the economy. When the economy is peaking or troughing, the birth-death model is not going to give us an accurate read. The rate of change of these rate of change numbers will be moving either from positive to negative or vice versa. And the birth-death model is going to be going in exactly the opposite direction.

The tell, then, is revisions. When you see numbers get consistently revised up month after month, it’s a tell, not that the statisticians are wrong, rather that the first derivate has accelerated. Analogously, when revisions are repeatedly down. That’s a sign of accelerated and unanticipated slowing.

Right now, that’s where we are. If you look at the jobs numbers, when new data come out, prior months continually get revised down. That’s a bad sign.

Downward revisions

So, likely what is happening at the small business level is an increase in unemployment from business deaths relative to the statistical estimates. And conversely, we should also expect a decrease in employment from new business creation relative to statistical estimates.

This may be the reason the household survey has become more bearish than the establishment survey. It is picking up on the downward shift in employment growth that the establishment survey cannot. My suspicion is that benchmark revisions of the data will show that, while June data looked really good and kept the Fed from cutting 50 basis points, the reality in this economy is weaker than the headline numbers would imply. When the birth-death numbers go from estimate to reality, there will be a downward revision across the board for much of 2019.

Lack of policy and real economy support

None of that spells recession of course. We can just as easily have a mid-cycle slowdown reversing course as bullish sectors of the economy help arrest the troughing. However, right now, there are very few sectors of the economy that are acting as a counterbalance to the broad-based weakness.

For example, residential construction has led the downshift in economic statistics, whereas in 2015 it was fighting that trend, acting as a counterweight. Homebuilding peaked in April 2018, and is down 11% since that time. The same is true for the auto sector, where jobs are being cut. Auto sales have peaked for this cycle.

At the same time, when the headline numbers mask weakness, it means policy support will be less accommodative both on the monetary and fiscal side. And, as a result, we are likely in a period where the troughing process will play out without any sort of stimulus to cushion the shock.

There’s also no support from abroad. We know, for example, that Europe, China and Japan are all seeing a downshift in growth. To the degree that currency and trade wars and weakness abroad persists, that has to infect the US economy. What worries me there is that Japan, where data had been surprising to the upside, reported Machine Tool Orders for June down -38% year-on-year this morning. That’s a new low for this cycle and the worst print since October 2009, according to Darius Dale of Hedgeye.

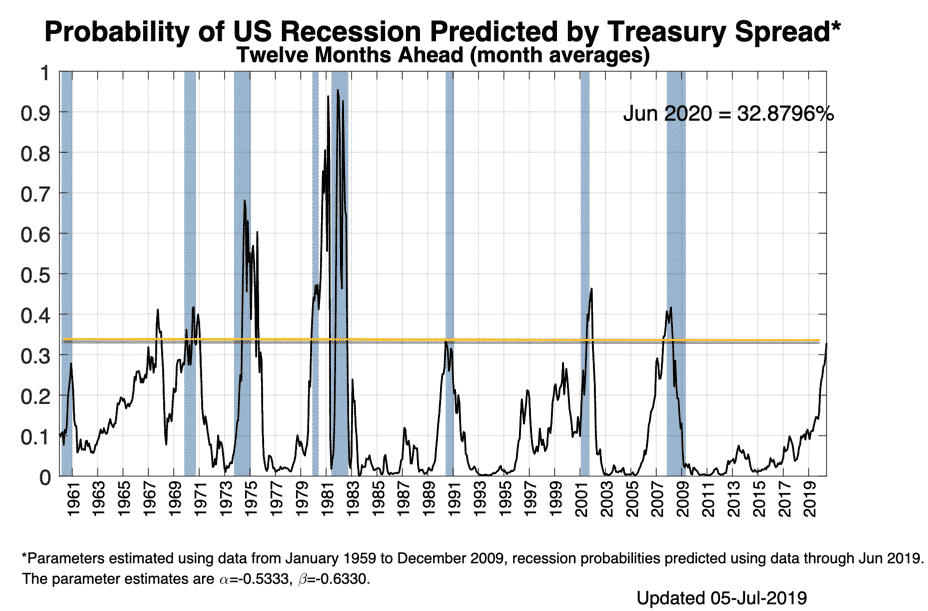

The NY Fed Recession Probability Estimate

So I take the NY Fed’s Treasury Spread warning signs seriously. Right now, it shows levels of curve inversion that, according to the NY Fed’s model, put the probability of recession higher than at any time that did not precede recession.

What the model says is that, if the Treasury Spread is a good indicator, the spread today suggests that recession is coming. The recession probability has never been so high without a recession happening in short order.

Remember, this is the Fed’s own model.

So, what is the Fed to do? What are fiscal policymakers to do? The data suggest that they should be taking out insurance cuts and adding insurance stimulus to keep the economy from falling into a recession. But that’s the data I’m looking at. It’s hard to make that case, though, when the jobs number for June is a net 224,000 added to employment roles.

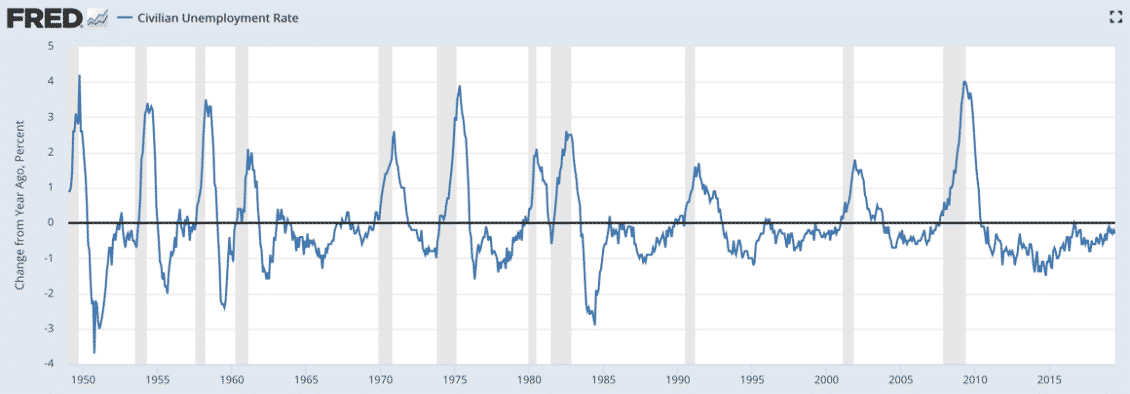

The household survey is telling you a totally different story.

Here, the rate of change in year-over-year unemployment levels are signalling the kind weakness you typically see before recessions. Rate of change levels for jobless claims are not sending a demonstrably different signal either.

Conclusion

So, the downside risk here is an accelerated softening of the US economy that is not being captured in the data or is being discounted by policymakers.And given the lack of real economy or policy support coming, this softening could lead to a recession before policymakers realize what has happened.

That’s my base case, in fact. I expect the data to weaken further without sufficient policy support. And I believe the weaknesses are broad-based enough that it will eventually end in recession before 2020 is over.

That’s bullish for bonds. For equities, the outlook is mixed because it depends very much on the offset between an earnings recession and the lower discount rates of future earnings as bonds rally. The more speculative end of the market will get hit hard though. And the risk of recession leading to credit problems is definitely going to be a big factor as this plays out.

For you and me, it’s not clear yet how bad this downturn could be. But, I do expect any downturn in the US and elsewhere in the developed world to lead to a further radicalization of the electorate and a shift away from the political center.

Comments are closed.