The awful news coming out of Germany

Quick note here before I get into the post: I am going to start posting these pieces on both Credit Writedowns and Patreon to flesh out who is getting all of the emails. If you are only getting one of these, please email me and I will look into what is going on. Now, onto the content.

Yesterday, I highlighted Germany as the country to watch in terms of downside global economic risk. The principal reason is that we are experiencing a manufacturing- and trade-led deceleration in global growth. And Germany is the most prominent large industrialized developed economy leveraged to both of those arenas.

Today, I want to dig a bit deeper and also discuss the problems at Deutsche Bank and the German criticisms of the ECB.

The German data

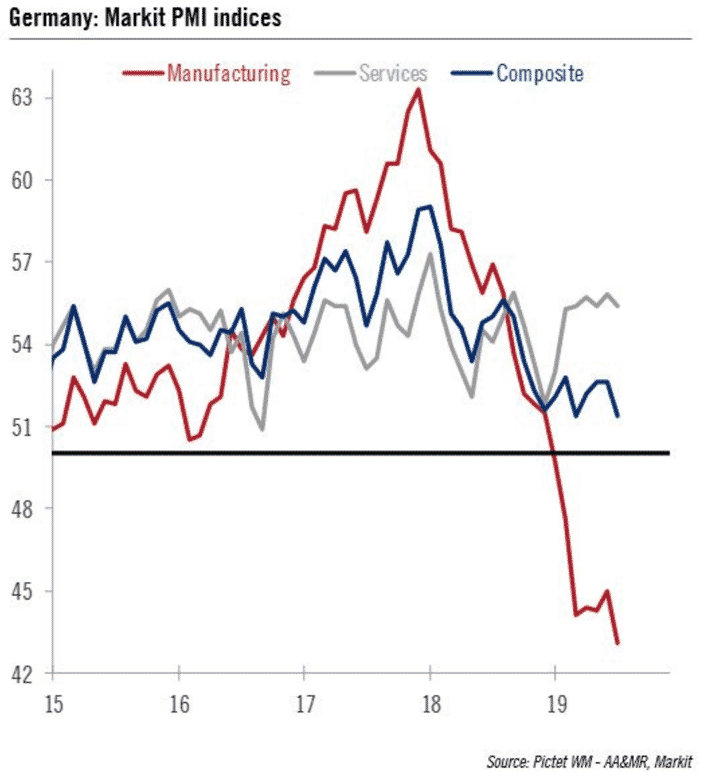

You saw the German data yesterday was pretty bad. But, what I highlighted in yesterday’s post was that it was really only manufacturing sector awfulness. Look at the Markit ISM chart again.

That big black horizontal line at 50 is the demarcation separating expansion from contraction. And you can see the manufacturing sector is hurting. But also notice the grey line has shifted up in 2019, meaning the German services sector was actually accelerating in the winter and has remained elevated in the spring. And even in Germany, services are more important than manufacturing. So, the composite view has to be that Germany can avoid worst case outcomes as long as the services sector does not give way.

German manufacturing companies report industry ‘in freefall’ https://t.co/UWWvIRKTDL

— Edward Harrison (@edwardnh) July 25, 2019

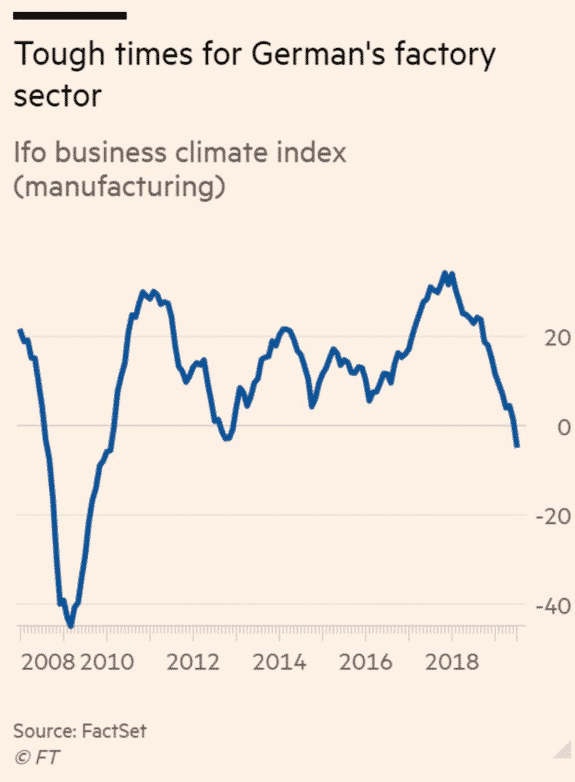

That’s not just based on the numbers but also on sentiment. Here’s the chart of Germany’s Ifo business climate index

Two things here. First, the numbers are below zero and the worst in this economic cycle. That tells you that manufacturing in Germany is the worst its been since the Great Financial Crisis.

Second, notice how much worse the numbers from 2008 and 2009 were. That gives you a sense of the magnitude of the crisis in German manufacturing and the German economy back then. It also gives you a sense of the vulnerability of the Germans to their export- and trade-led economic growth model. Sure, things are going well domestically in Germany. But, we can see that when external events play out negatively, Germany feels it much more acutely than the US because they are so dependent on external demand for growth.

The Deutsche Bank backstory

And it’s not just manufacturing that is plaguing the German economy. They are overbanked. And, as a result, Deutsche Bank, the largest German lender, is legitimately in jeopardy of failing.

The backstory is this. In the early 1990s, as plans for the euro were being formed as a counterweight to the US dollar, European policymakers also encouraged European banks to bulk up to take on their US brethren. Investment banking services had come to be dominated by the US institutions Goldman Sachs, Morgan Stanley and Merrill Lynch. And that was fine for a while because – even more than now, where Europe is still overbanked – there wasn’t a huge securities market that required huge investment banking services. Banks simply made (relatively low profit) commercial loans and kept them on their balance sheets.

But when the US bank behemoths like Citibank, JPMorgan, and Bankers Trust entered the fray, they used their balance sheets as an entree into European banking by giving bridge loans and the like to clients and then issuing bonds. The US institutions then started to dominate a crucial area of profit growth in the European financial services market.

I came onto the scene about that time, recruited by Morgan Grenfell, the British merchant banking offshoot of the House of Morgan that was divested under Glass Steagall in 1934. It had recently been bought by Deutsche Bank as the European banks desperately tried to get into investment banking by buying up British merchant banks. There was SBC Warburg and Dredner Kleinwort Benson as well as ABN AMRO Hoare Govett and ING Barings, to name a few of the European-British combos used to fight off the Americans.

When I arrived at Deutsche in London in 1997, it was just beginning to transform into an American-style investment banking-centric behemoth, having recruited Edson Mitchell at huge cost from Merrill Lynch to head the Global Markets division. He brought in all of his guys from Merrill, with Anshu Jain, one of the Merrill guys eventually becoming co-head of the bank in 2012.

I was in the leveraged finance arena, where I used my German-language ability to spearhead the move toward taking German corporate clients off of loans on the balance sheet and into high yield bonds, freeing up capital for DB and making them more money since high yield deals gave the underwriters 3%. We even did bridge loans to help get this business done, just as the American banks had done. Everything I saw was very much in the mold of the American banks. And that only increased once DB bought Bankers Trust, in particular for access to its leveraged finance group.

Deutsche Bank today

That backstory is important because Deutsche Bank is exiting this business. All of the other big German banks were stung by the global financial crisis and have retreated. Dresdner, Commerzbank (which merged with Dresdner), and West LB have vanished from the investment banking league tables that they sought to climb in the 1990s and 2000s. Deutsche Bank is the last. Having fired their Anglo-American investment banking oriented heads, they are now returning to their roots, commercial banking.

But, that’s a big problem. First, Deutsche Bank has a lot of hidden legacy liabilities. It has a huge derivatives book to unwind over time. And during its international rampage, it had such lax controls, nearly every scandal in banking has involved DB in some way, even the Epstein case.

SURPRISE: Deutsche Bank played a role in Jeffrey Epstein’s financial dealings in recent years, according to people familiar with the matter https://t.co/At68EsPAEL

— Edward Harrison (@edwardnh) July 23, 2019

There are going to be huge fines associated with these scandals. And I believe we are going to see DB pay for money laundering activity emanating from the former Soviet republics just as Danske Bank will pay, as it is in the headlines for lax controls there.

Deutsche remains a problem. I believe the German government is worried because its anti-bailout position means there is only a implicit backstop for this too-big-to-fail institution in extremis, in crisis https://t.co/GdfqSuUY6l

— Edward Harrison (@edwardnh) July 24, 2019

Read the thread linked above because it gets at the problems.

- DB has no real backstop because Germany has insisted Italy, Greece and other EU countries not be allowed to bail out their problem banks. It can’t ‘go soft’ on Deutsche as a result.

- But Deutsche Bank just reported a massive €3.1 billion loss in Q2, greater than expected. Their tier 1 capital ratio could fall to 12.7%. That’s just 20bps above minimum requirements, meaning they will need more capital soon.

- Meanwhile, Deutsche’s domestic commercial banking business makes NO money whatsoever. It’s no different today than when I was there 20 years ago. So, without investment banking, there’s no profit center to help rebuild their balance sheet. Cuts alone aren’t going to get them there.

- Today, the European Central Bank signalled it was ready to cut rates for the first time since 2016 from their already negative level. That’s just a tax on banks. Goldman Sachs estimates that another 20bps cut would trigger losses in the 32 banks they cover of €5.6 billion, about 6% of profits. What companies like Deutsche need is a steep yield curve, not more cuts.

My conclusion:

There’s ZERO chance Deutsche Bank can generate any meaningful returns on its domestic commercial banking business and restore its balance sheet while the ECB’s policy rate is negative. It’s effectively a zombie bank now.

— Edward Harrison (@edwardnh) July 24, 2019

The German Outlook

Look at that Ifo chart again and look at 2008 and 2009. It’s probably not going to get that bad in reasonable worst case scenarios. but, at a minimum, it tells you what the downside risks are.

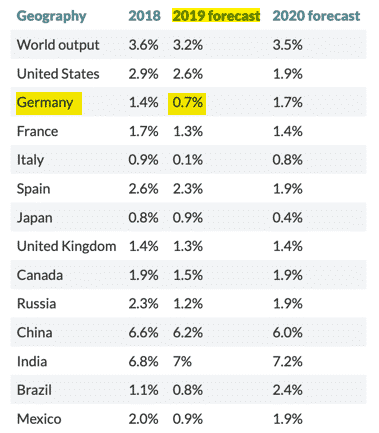

The outlook for Germany is negative. Two days ago, the IMF downgraded its global growth forecasts. And Germany’s 2019 number looked awful.

Source: MarketWatch

I think there is a lot of downside risk there.

And let’s remember that, were Deutsche Bank to go into freefall, that would be a huge negative shock for the global financial system, much worse than Lehman Brothers. It’s unfathomable to me that they wouldn’t bail DB out in some fashion, as an emergency measure, which I am sure all the EU treaty loopholes allow.

My view here on Germany is negative. It has caught out moralizing about fiscal responsibility and other countries getting their house in order. But they have a huge problem on their doorstep with Deutsche Bank and they have been playing with fire by using beggar thy neighbor policies to prop up their domestic economy. The chickens are coming home to roost. And the Germans have nobody to blame but themselves.

Comments are closed.