This post is going to be relatively long because I am going to try to combine a number of threads together. I thought about putting this post in the investor newsletter pool. But I am going to give it a wider distribution because of the economic implications. But, look for any follow-ups via the investment newsletter channel on Patreon.

This piece was precipitated by the sudden and unexplained sharp decrease in government bond yields across economies. I noticed, in particular, that the 10-year German Bund was negative yielding yesterday, within one basis point of the Japanese 10-year. And both of those yields have gone lower since.

The overarching theme here is about downside economic risk, the decrease in yields as a signpost of that risk, and of potential reasonable worst case outcomes. I will try to tie it all together at the end. Let’s start with the Fed.

Fed policy shift as market catalyst

My thesis here is that the sharp adjustment in bond yields shows bond investors taking out insurance on the underperforming global economy now that the Fed has shifted from a tightening to an easing bias. And it makes sense purely from a tactical perspective because of the Fed’s dominant role as supplier of global liquidity. In the world in which the Fed was tightening, it was fine for other central banks to ease because that policy divergence would have no incremental tightening impact on their domestic economies. But, in today’s world in which the US central bank is easing or threatening to ease, no central bank will want to be tightening except if the domestic economy warrants it. They will want to be in sync with the Fed. And that puts downward pressure across global government bond assets.

Moreover, it is also clear that almost all of the major central banks have an easing bias, including the ECB, the Bank of Japan and the Bank of England. So, with the Fed’s about-face on rates, we have moved from a world of Fed tightening ratcheting up pressure on borrowers of US dollar, domestic and foreign, to a world in which trade flows are stymied, making it ever harder to ‘steal’ growth via mercantilist policy and export growth. And so, eventually competitive currency depreciation dynamics could come into play. That’s bullish for bonds.

The real economy has weakened

Weakening leading indicators have been in place for a year now. On that front, this sentence from an FT article caught my eye:

“Citigroup’s global Economic Surprise Index, which measures how often data comes in better or worse than forecasts, has been in negative territory for almost a year. That is its longest sub-zero stretch since 2008.” https://t.co/BSHBwS7LFL

— Edward Harrison (@edwardnh) March 28, 2019

And so, even though ECRI research says leading economic indicators continue to point to more downside risk, the question in markets now is whether the global growth slowdown is bottoming. Just as I have been willing to entertain Lael Brainard’s thesis that ‘this time is different’ regarding curve inversion – a view that Jerome Powell has championed as Fed chair, I am also willing to consider that the LEIs are giving us a head fake about where global growth is headed. Some of the numbers have turned up.

For example, for the first time in many weeks, data released this morning show the 4-week average for initial jobless claims came in below year ago levels. That’s a sign that, though the jobs picture may have weakened somewhat, the employment market is not deteriorating significantly. It speaks against the possibility of a US recession.

Nevertheless, I would err on the side of caution in placing your bets. And that means taking into account downside risks, what this article is all about.

Europe as ground zero

In terms of risks going forward, I am looking at Europe in particular. One reason is that European public asset markets have greater leverage to pro-cyclical economic sectors like manufacturing and banking. So, to the degree global growth continues to slow, we should expect Europe to underperform.

But, Europe is also positioned poorly regarding countercyclical stimulus. Overnight rates are already at -0.40%. And the ‘no-bailout’ rule for euro zone member state government debt means that the ECB’s backstop for Italy and other peripheral nations is suspect. It can only be activated in conjunction with Europe’s bailout fund, the European Stability Mechanism, meaning only in extremis – after Italy has gone through the bond vigilante wringer.

Moreover, the Fiscal Stability Treaty, a new stricter version of the Stability and Growth Pact, signed on 2 March 2012 by all EU member states, except the Czech Republic, and the UK, will mean fiscal policy will, at best, be constrained. At its worst, we could see austerity became fiscal policy as governments attempt to meet their debt and deficit hurdles in a deflationary environment. And the ECB can use its role as euro zone ‘lender of last resort’ to enforce the rules, as it did with Greece.

Banks as source of contagion

The question regarding any move from a low-grade garden variety recession to out-and-out panic and crisis revolves around triggers and accelerants. And the banking sector is front and center on that score.

There are two ways that Europe’s financial sector could contribute to downside risk. First, there is the still problematic government debt – bank debt nexus. The way this worked during the European sovereign debt crisis is through bank collapses creating contingent liabilities for euro zone member state governments. When banks actually did collapse, as they did in Ireland, for example, the state was forced to step in and bail them out, socializing the banks’ losses by heaping bank debt onto the state’s debt load. Ireland and Spain were forced to seek bailouts for exactly this reason.

This coupling still exists despite the bail-in rules now in place, simply because Europe’s banking union is incomplete. And the lack of a euro zone wide deposit guarantee means the collapse of one Italian bank, for example, will mean runs on other Italian banks, forcing the Italian government into the bailout role. Without an explicit central bank backstop, that means very bad things for Italian government debt.

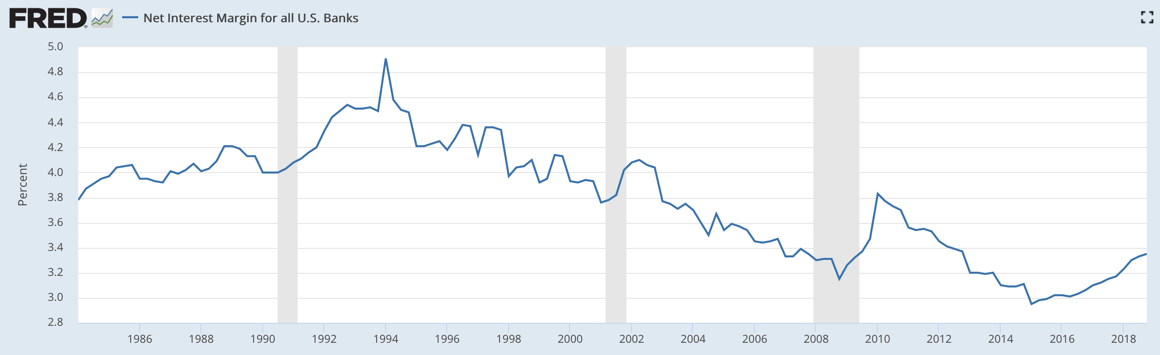

Net interest margins

But, then there are the net interest margin problems associated with the ECB’s permanent zero rate of interest. First, negative interest rates are just a tax on reserves that lowers net interest margins.

“low short-term interest rates can depress bank margins because for many types of deposits, banks are reluctant to lower interest rates. Since banks must pass on lower rates on assets based on contractual re-pricing terms (e.g. floating rate loans), and have an incentive to do so to those borrowers that have other financing choices (e.g. from corporate bond markets), bank margins compress as rates decline.”

The conclusion:

banking systems in many low interest-rate countries will face challenges. Until lost income can be offset through other actions, lower profitability will reduce financial institutions’ ability to build and attract capital, increasing their vulnerability to shocks and declines in market confidence, undermining their ability to support the real economy, and potentially weakening the transmission channel of monetary policy.

That’s where Europe is right now. And there’s a lot of evidence that permanent zero rates lower bank profitability. For one: “Changes in bank rates have a much greater impact on and explain more of the variation in net interest margins than do changes in balance-sheet compositions.”

But, when the curve is very flat or partially inverted, as it is in the US, Canada and New Zealand, right now, “the [flatness or] inversion also prevents banks, which borrow short and lend long, from getting as much net interest margin. And, in that way it restricts credit.“ That’s what I wrote yesterday. Empirically, we know this is true. And evidence from the US shows it is smaller banks with greater exposure to interest income that drive this phenomenon. The Dallas Fed has produced research on this last year. And since, European debt capital markets are less well-developed than they are in the US, banks there are more interest income dependent. And we should expect the European banking sector to suffer as a result.

As an aside, the Fed’s research is also a reason to see large US banks as better-positioned for a US downturn since smaller banks have more on-balance sheet exposure to commercial real estate and other sectors likely to suffer in a downturn. Though the chart below doesn’t show it, since policy rate levels dominate the NIM trend, research shows that net interest margins are pro-cyclical.

And smaller banks will be hurt by this.

The interest income channel

In terms of zero rates, one thing I have focused on in the past that others seem to overlook is the interest income channel. Let’s start here with Moody’s:

In the first half of 2018, many large US banks reported a decline in their average noninterest-bearing deposits versus the comparable year ago period, Moody’s Investors Service says in a new report. This is a credit-negative trend, which combined with pricing competition, will lead to a further increase in deposit betas and constrain net interest margin (NIM) expansion.

“Because banks pay no interest on noninterest-bearing deposits, their decline will constrain the incremental profitability gains from any additional US Federal Reserve interest rate increases that occur over the next year,” Moody’s Senior Vice President Allen Tischler said.

For banks, the growth and retention of noninterest bearing deposits is typically a priority as it is both a cheap funding source and an effective tool to manage interest rate risk arising from holding long-dated assets, such as residential mortgages. BB&T Corporation (A2 stable) and Citizens Financial Group (holding company unrated; bank-level issuer rating Baa1 stable), were the only two large banks to experience growth in average noninterest-bearing deposits in the last year.

Moody’s says deposit betas measure the change in the cost of deposits relative to the change in the Fed funds rate. Higher deposit costs reflect the drop in noninterest-bearing deposits as well as competition from alternatives, such as higher yielding money market accounts offered online.

Two takeaways: First, the private sector has traditionally been a net receiver of interest income. So, lowering interest rates on a sustained basis as a way of igniting the economy will suffer due to this shortfall of interest income. This is especially true as societies age, given the higher preponderance of fixed income in the portfolios of older investors.

But, equally important, to the degree that you have zero or negative rates, it acts like a repellant for deposit growth. And that alone will cause net interest margins to shrink. Again, small banks and euro banks will feel the pain more than large US banks.

Sweden: monetary policy uber alles

With that background, we can start to think about policy choices available if the economy continues to decelerate. I want to use Sweden as a guidepost here for a number of reasons. First, it is monetarily sovereign, meaning it has more policy space within which to operate. Second, it is run by the centre-left party which is more politically likely to use fiscal space for policy tools. And third, it has had enviable growth over the past decade.

Here’s Bloomberg:

Sweden now has so little debt that many are starting to wonder why the government is not spending a lot more.

LO, the nation’s biggest trade union group, wants the Social Democrat-led administration to change its policy and channel a lot more money into the economy instead of worrying about protecting budget surpluses.

“Until Sweden has full employment, we could have a deficit target,” LO president Karl-Petter Thorwaldsson said in an interview.

He wants investments to go up “for a number of years” and points to housing and infrastructure as areas where spending “should be carried out at a larger scale.”

The biggest Scandinavian economy, which relies on global trade for about half its output, is slowing down, but the government has so far appeared reluctant to use its fiscal leeway to fight that trend.

That has drawn criticism from analysts, with some even referring to the government’s penny pinching as a form of “insanity.”

Swedish government debt is at its lowest in 40 years and falling.

According to the National Financial Management Authority, debt would sink below 35 percent of GDP this year and breach 30 percent in 2021. At that point, the government would be required by law to explain to parliament why debt is so low.

Translation: Even though the Swedes could change their policy mix away from over-reliance on rate policy, they are loathe to do so.

How to explain Sweden

What’s happening in Sweden is the same thing that has happened everywhere else in Europe. After some difficult economic periods – in Sweden, it was after the house price collapse that hit Scandinavia and the UK in the early 1990s – governments got religion about dialing back state control and instituting structural reform. We could argue about the efficacy of those policies. But what is clear is that the paradigm shift was embraced by the centre-left as much as by the centre-right parties – as it has been right across Europe and North America.

The result is that activist fiscal policy is seen as irresponsible. And so, to the degree that countries activate countercyclical policy levers, they do so with monetary policy, lowering rates or increasing them to hot up or cool down an economy. You can see the dominant impact of policy rates in the net interest margin chart I posted for the US above on US banks.

And what that does is create a large gap between an interest rate level that would act as an accelerant on real economy growth and the one that acts as an accelerant for credit growth and asset prices. Think of Hyman Minsky’s two price system model of the economy and you have the makings of asset price inflation in the midst of wage and consumer price stagnation.

So, Sweden has seen a large gap open up between the haves and the have-nots as well as a bubble in housing in the wake of the financial crisis. They are trying to manage this via rate policy even as labor unions are telling them no. And the disaffection engendered by this two-tier economy is driving voters away from traditional parties, particularly the centre left. Nationalists and far right parties are the biggest beneficiaries of the move in Sweden – and elsewhere in Europe.

Outlook: The Japanification of Europe

What I’m seeing, then, is policy inertia that skews decisions in favor of monetary policy over fiscal policy, entrenching income and wealth inequality and providing succor to nationalist political parties. Sweden is but one example. As in Japan, the continued use of zero and negative rates will lower bank profitability and reduce interest income in a society more dependent on fixed income sources due to aging demographics. The result is so-called secular stagnation.

To the degree, this policy inertia continues, even into the teeth of a recession, it could lead to an economic and political crisis in Europe as the banking and manufacturing sectors falter. In the eurozone, the institutional framework will not be able to cope with this outcome, resulting in renewed worries about the integrity of the euro zone.

In terms of financial assets, for me, this makes the case for bonds. The scenario here is inherently disinflationary or deflationary. And the initial responses by central banks will be to leave rates lower for longer. To the degree they try to ‘reflate’ via monetary policy, they will fail. And yields will fall, particularly at the long end of the curve.

The irony in all of this is that, if I’m right, in the short term, it is outliers like the Fed that will need to move by cutting rates back toward zero over the medium term. But, once there, they will be trapped – and reach the end of the line regarding monetary reflation.

Eventually, we are going to see fiscal policy take the baton though. When, in what form and after what kind of economic, political, and military adventurism is the important question. Even if we avoid worst case outcomes, the grist for a continued populist backlash will remain until policy skews toward labor and closes the income and wealth gap. Europe will feel this upheaval more than most.

Comments are closed.