Why the flattening yield curve doesn’t worry me yet

If you look at the yield curve since the early 80s double dip recession, what you’ll notice is that inversion – where 2-year rates exceed 10-year rates – precedes every recession. Right now, we’re still 70 basis points from inversion though. So far from expecting a slowdown or a recession, I would sooner expect economic acceleration. Let me go into detail below.

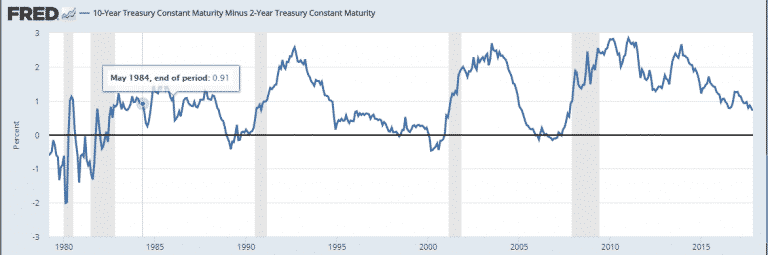

First, here’s the chart. It’s the 10-year constant maturity Treasury rate minus the 2-year rate. This spread is the most commonly cited one used to denote how flat or steep the yield curve is.

There are several distinct periods in the picture above.

- During the double dip, the curve steepened dramatically from a near 200bps inversion to 100 basis points. This presaged recovery. But when the curve flattened once again and inverted, recession came soon after.

- During the 1980s, the 2-10 spread was never steeper than 160bps. And it dipped dramatically twice, once in 1984 and again in 1986 without presaging recession because the Fed was cutting. It was only when the curve inverted in 1989 as the Fed was hiking that recession came. And the delay between inversion and recession was about 16 months.

- In the early 1990s, the curve steepened dramatically as the United States recovered from a commercial real estate bust and the Savings and Loan crisis. But when the Greenspan Fed raised rates unexpectedly fast, we almost had a recession. And the flattening of the yield curve matches that fact. Even after the recession was averted and the Goldilocks era began, the curve remained relatively flat all throughout the late1990s, briefly inverting during the Russian default and Long-Term Capital Management crisis. Only in March 2000, when the curve inverted more decisively, did recession follow.

- Then, when the Fed brought rates down to 1% in the early 2000s, the curve steepened dramatically again – as much as it had in the early 1990s. But we saw a dramatic flattening starting in early 2004 as the Fed began to hike with the first inversion occurring in February 2006, a full 22 months before recession.

- The last phase here began as the Fed cut rates to zero during the Great Financial Crisis. For the third decade in a row, we saw the curve steepen to a spread in excess of 250 basis points as recovery took hold. While the curve flattened to below 150 basis points in 2012, as the Fed poured on QE3 from September 2012 to December 2013, the curve steepened again to over a spread over 250 basis points before declining as the Fed withdrew accommodation.

I would make two observations about the data from this period then. First, the steepness of the yield curve is not a sign of impending economic acceleration or deceleration per se. Rather, the curve is an indicator of the market’s perception of the level of monetary accommodation. For example, when the yield curve steepness peaked in December 2013 as the Fed ended QE3, the subsequent flattening was a sign that the market believed the Fed was becoming less accommodative, not necessarily that the economy was slowing.

Second, the yield curve has to invert to signal recession. Every time there has been a recession there has been an inversion beforehand. And because long-term interest rates are a series of future short-term rates, what an inverted yield curve is essentially saying is that on balance Treasury market participants believe that the Fed will be forced by a weakening economy to start cutting rates in the medium-term future in order to prevent the economy from becoming even worse. That’s why December 1994 was a near miss and June 1998 saw a brief inversion but no recession. In the case of 1994, the Fed was forced to cut and the economy actually recovered. In 1998, the Fed also cut and added liquidity to boot, even helping engineer a rescue of LTCM. The economy avoided recession again.

Conclusion: With the spread between ten-year rates and two year rates still around 70 basis points, the Fed has no reason to panic. In fact, with the global economy showing signs of acceleration and the last two quarters of US GDP growth hitting above 3%, the Fed should be more concerned about a US acceleration than a slowdown.

But, of course, some prognosticators are betting the Fed raises rates 4 times in 2018. With the curve already so flat, that would be a policy error. Given that the long end of the curve has not responded to economic growth or to Fed hikes, I believe four hikes in 2018 would take us into the danger zone of a spread of just 40-50 basis points or less. The potential for recession would start to rise dramatically at that point were the Fed to hike into a curve that flat.

This is a ways off though. People talking about a 2-10 spread at 70 basis points like its the end of the world aren’t looking at the data. Right now, the skies are blue. But the Fed does have to be careful. It won’t take much to get us into the danger zone from here. And that’s when you need to turn defensive.

Comments are closed.