Why I am now officially on recession watch

The recent data coming out of the US have been almost unrelentingly negative outside of the recent jobs reports. The Atlanta Fed GDPNow report was already down to 0.7% for Q4 when poor output and retail sales data came out. I expect the GDPNow forecast to fall even lower. And given the signal that the change in non-farm payrolls is sending and the difficult comps for weekly jobless claims, I believe we are now at stall speed in the US economy, putting me on recession watch. I have a number of data points to review here. So let’s get to it straight away.

As a recap, yesterday I put out a note indicating that my view was that the U.S. economy may be decelerating but that it wasn’t necessarily headed for recession in the near term. I have also previously written that Goldilocks was sick in bed but could be revived back to health. The overall message was that we should be concerned but not alarmed by the state of the real economy. Downside risk was considerable and increasing but the US had not hit stall speed.

The message I am sending today is less optimistic. We are at stall speed now and we should be alarmed both at how quickly markets are falling and what this says about the underlying health of the economy. I believe the US economy is so weak that any turbulence from a large income, inventory, or production shock could mean recession. The data revision I did yesterday and the news that has come out since that time make this clear.

First, let me update you on the two jobs data sets from yesterday — and why I view them more negatively today. The way I look at jobs is as income that supports consumption. An economy follows a growth path in large part because the job path underpinning income is moving upward at a stable or an increased rate. When the growth in employment stalls and then falls, it is a ‘shock’ to income growth that causes producers to re-calculate and potentially to purge inventories. This re-calculation doesn’t have to lead to recession. It could be a mid-cycle pause, after which the economy resumes a robust growth path. However, if the feedback between jobs, income, and production is large enough, we hit a stall speed, where any relatively large jobs, income or production shock would mean recession. This is where we are now.

I have been thinking a lot about the missing data I added to the non-farm payrolls series in yesterday’s correction. And I have come to the conclusion that the easiest way to parse this is to look at false positives and lags to recession once the second derivative turns negative. So I am going to concentrate on that here.

If you look at the 12-month percentage change in non-farm payrolls in the business cycle that ended in December 2007, you see no false positives indicating recession and a lag from early 2006 to late 2007 for recession.

For the business cycle that ended in 2001, if you look at the 12-month percentage change in non-farm payrolls, you do see a false positive that coincided with the mid-cycle pause after the Fed’s tightening cycle in 1994-95 and there was a lag from early 2000 to 2001 for recession. This is heartening because it means that you could see job growth roll over and the economy could still avoid recession.

Finally, if one looks at the 12-month percentage change in non-farm payrolls in the business cycle that ended in December 1990, one sees yet another false positive in 1985 indicating recession and a lag from 1989 to late 1990 for recession.

My overall impression of this data series, then, is that it is inconclusive in signalling recession. However, it is very good at signalling stall speed, given that 1985 and 1994 are two memorable mid-cycle pauses. Given the shape of the 12-month percentage change in non-farm payrolls line today, and the duration of the negative slope, it is reasonable to say the US economy is now at stall speed.

On the second series, jobless claims, going forward I will look at both initial and continuing claims for clues. In the past, I have said that a rise of +50,000 in average initial claims and of +250,000 in average continuing claims was enough to be a trigger for recession. The way I interpret this signal is that initial claims act as a payroll flow in that they show how many people eligible for unemployment insurance are losing their jobs. When that week-to-week flow increases a lot in a short period of time (6 to 12 months is the time periods I have calculated in the past), then it acts like an income shock to the economy — enough of a shock to take an economy from stall speed into recession.

When you look at last year’s initial claims numbers, what you see is the trend flirting with sub-300,000 levels before rising above 300,000 – perhaps due to seasonality effects — before then plummeting to as low as the 260s on a seasonally-adjusted average basis. That means a rise back to the 300,000 range would be very close to recession. Recession would almost certainly come with a rise to the 350,000 range this Winter and only the 320,000 range this Spring.

Right now, the numbers are still benign, with the 4-week average at 278,750, which is down from 293,000 a year ago. Using non-seasonally adjusted comparisons yields similar year-over-year comparisons, such that I feel reasonably good about the signal from this data series for the next couple of months until March.

Bottom line: Jobless claims say we are not even at stall speed yet.

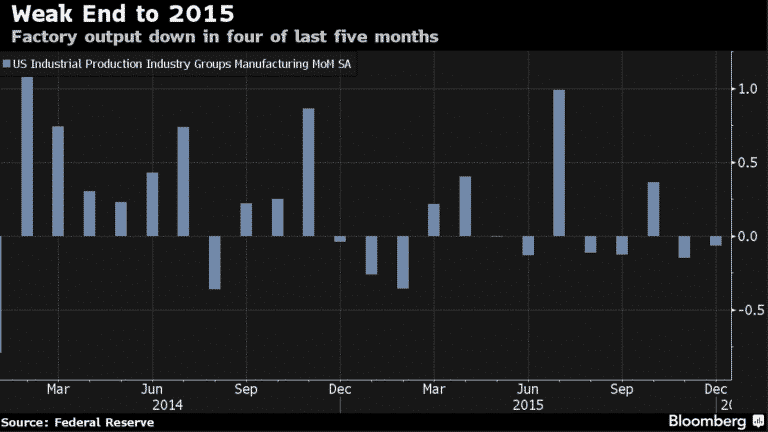

The other data points that came out today confirm stall. They are the output and retail sales numbers, with both declining in December. Retail sales were the weakest since 2009 last year and factory output was down for the second month in a row.

A lot of people are pointing to manufacturing weakness as a harbinger of worse things to come in the US. I’m not quite there yet. But I do believe the US economy has decelerated and is now at stall speed, given the steep and long-lived drop in payroll growth. Therefore, I am on recession watch. Recession is not a base case. But it is no longer a tail risk either. Recession in the US is a reasonable worst case outcome for the economy, especially if the Fed continues on a path of interest rate increases. Markets are sending this signal to the Fed right now. And I believe the Fed will probably stand down in March as a result. But that won’t be enough to ensure a positive outcome as prior tightening is still working with a lag.

Comments are closed.