My thoughts on the latest US economic data points

As the Federal Reserve prepares for its next open market committee meeting and statement, I want to take a look at what US data are saying about the US economy. The main focus here is going to be the underlying pace of the US economy and the degree to which cyclical factors are diminishing or adding to that pace and whether or not the Fed has incorporated this analysis into its thinking.

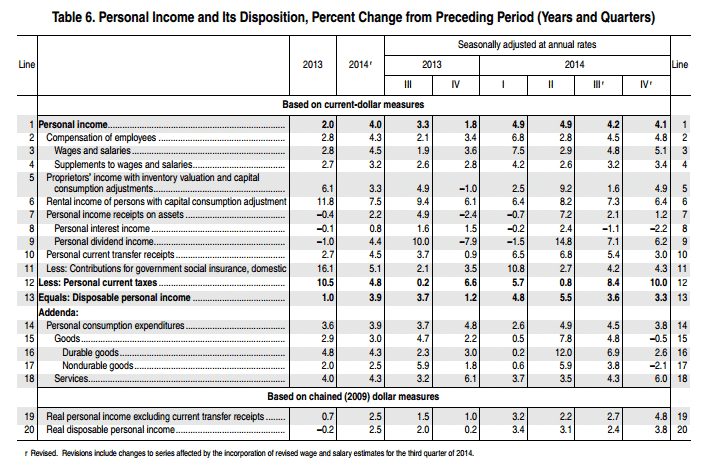

First, let’s look at the macro data from the household sector, since that’s the main driving force in the US. The wage-related data are holding up nicely. If you look at any wage-related time series, whether it is the personal income from the BEA, labor costs from the BLS or the hourly wage data from the monthly jobs report, what we see is wage data that are moving up in real terms and in nominal terms. The BEA data, for example, show personal income gains from September to January of 0.2, 0.4, 0.4, 0.3, and 0.3% for each month respectively. In fact, if you look at 2014, every quarter’s personal income data is up at an annualized pace over 4%.

For me, that’s the real reason behind the Fed’s move toward raising rates. While disposable personal income is not quite as robust of late, with the unemployment rate falling toward 5% and wage growth at a reasonable level in both nominal and real terms, the fed finally feels comfortable with removing the language around “patience” and preparing to raise interest rates.

On the jobs front, we are still not seeing an appreciable uptick in initial jobless claims that would suggest a reversal in the pattern of job growth. Thus, we should be able to count on the 250-350,000 increase in non-farm payrolls lasting through the June timeframe when the Fed will begin to contemplate raising interest rates. I expect the unemployment rate to fall a couple tenths of a percentage point by then such that we will be very close to the 5% level that some Fed officials believe is the rate at which an employment-inflation trade-off exists. See my comments on this from 6 March.

Bottom line: unless we see a reversal in these numbers the Fed is going to raise rates sometime between June and September.

The problem of course is that the recent US macro data have been extremely weak, especially compared to Europe or China.

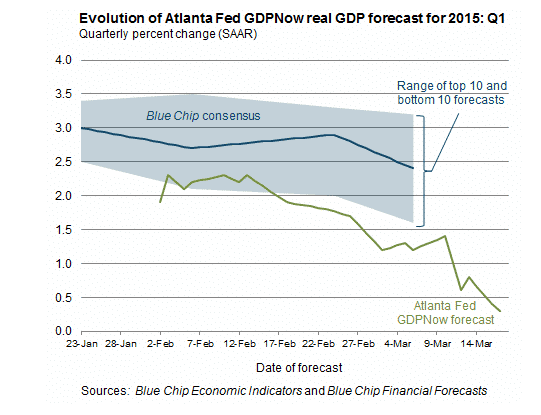

The US economic surprise index is deep into negative territory and the Atlanta Fed nowcast is showing a horrible Q1 print coming. How does the Fed address this conundrum? I believe the Fed will address it by noting the weakness in recent data as something to watch but not as something to make it maintain “patience” on staying the course at the zero lower bound. As a result, the Fed will move to a data-dependent path in which forward guidance is more unpredictable and market reactions should be more volatile.

If the US macro economic data are decent over the next 3-6 months, the Fed will raise rates at least once. If the data continue to be weaker than expected, the Fed will pause and wait until we see better data. Watch inflation, the unemployment level and wage growth. I tend to believe inflation is the least important of these three macro points and that the Fed will not react to lower inflation readings because oil prices are still falling. On the other hand, while the Fed won’t react to yield curve flattening, you should, because it is a sign that the market is uncomfortable with the fed’s policy stance and that economic weakness is coming.

Comments are closed.