The growing mess which will be left behind by the Abenomics experiment

By Edward Hugh

According to wikipedia, “overdetermination is a phenomenon whereby a single observed effect is determined by multiple causes at once, any one of which alone might be enough to account for (“determine”) the effect.That is, there are more causes present than are necessary to generate the effect”. In this strictly technical sense Japan’s deflation problem is overdetermined – there are multiple causes at work, any one of which could account for the observed phenomenon. Those who have been following the debate can simply choose their favourite – balance sheet recession, liquidity trap, fertility trap – each one, taken alone, could be sufficient as a cause. The problem this situation presents is simply epistemological – in a scientific environment the conundrum could be resolved by devising the requisite, consensually grounded, tests.

But I would here like to use the term “overdetermination” in another, less technical, sense, since it seems to me Japan’s problem set is overdetermined in that we always seem to be facing at least one more problem than we have remedies at hand.

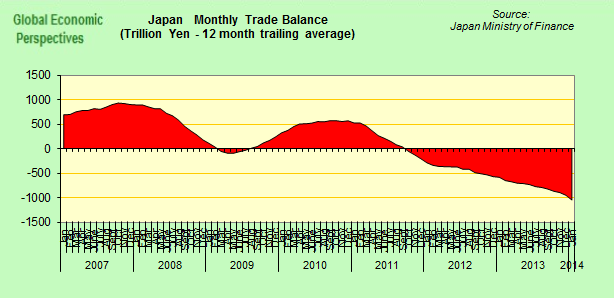

The case of the country’s ongoing energy dependency which is producing a growing trade and current account deficit would be a good example. Notionally the problem forms part of the legacy of the tragic tsunami which hit the country in March 2011 and lead to the decision to phase out nuclear energy capacity. But now that decision has been reversed, and starting this summer nuclear generating capacity is once more to be “phased up”. The issue is, from a strictly economic point of view would that be good news? Well, it would certainly help with the deteriorating trade balance:

But what about deflation? Would having cheaper domestically produced energy help here? Wasn’t generating inflation supposed to be the whole point of the Abenomics exercise? Don’t rising energy costs constitute the lions share of the country’s recent, much heralded, inflation?

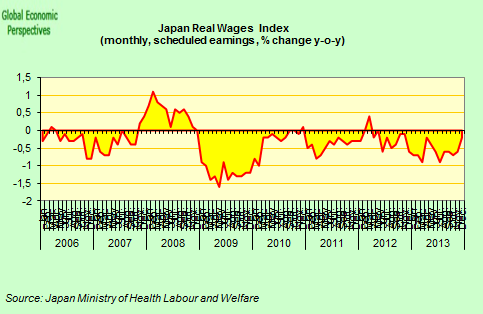

Falling Real Wages

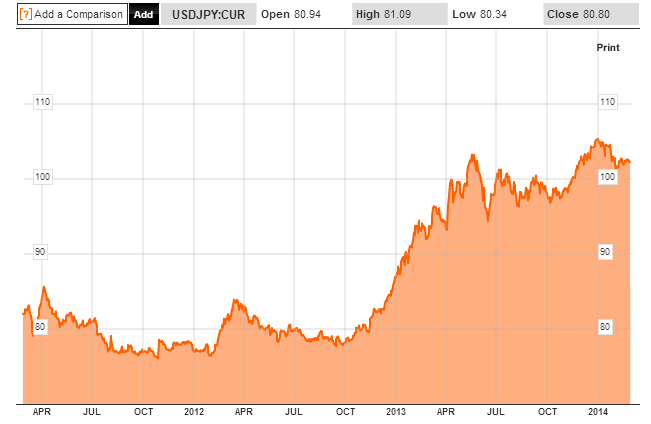

In this very context Takashi Nakamichi had a timely post on the WSJ blog last week. What is going to happen to Japanese inflation, he asks, if the yen does not undergo another significant depreciation? “Barring another major drop in the yen”, he points out, the earlier “exchange-rate effects will start to fade from this spring. Friday morning, the yen was trading around Y102 to the U.S. dollar – about the same level it was last May”.

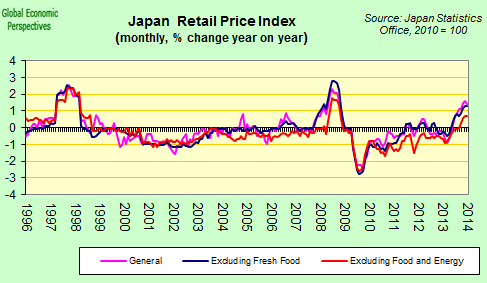

In fact – leaving aside the possible impact of next April’s consumption tax increase – the inflationary wave which followed the yen’s sharp depreciation (around 20% in the months between October 2012 and May 2013) may well already be waning. Annual inflation as measured by Japan’s general price index fell in January from 1.6% to 1.4%, while it remained the same on both the core (1.3%, ex fresh food) and the core-core (0.7% ex fresh food and energy).

As Nakamichi points out, roughly half of the current inflation in consumer products is due to the dramatic drop in the value of the yen. The drop has sharply inflated the costs of imports, especially energy imports, and these have partly been passed on to consumers. While many consumers in developed countries have been benefiting from lower energy costs, in Japan the costs of liquid natural gas — now a main source of power generation — were up 17% over a year earlier. In addition, “the Japanese also saw sharp rises in prices of foreign-made home electronics, which they increasingly import: Prices of washing machines were up 13%, while prices of audio equipment and refrigerators both rose 16%”.

Even the 0.7% annual rise in core-core inflation isn’t all it seems to be, since some 40% of the increase is accounted for by a one-off rise last year in charges for accident insurance and public services. The key point to grasp in all this is that the rise is due to what we could call “cost push” rather than “demand pull”. As Takeshi Minami, chief economist at the Norinchukin Research Institute put it,“Those increases had little to do with demand and supply.”

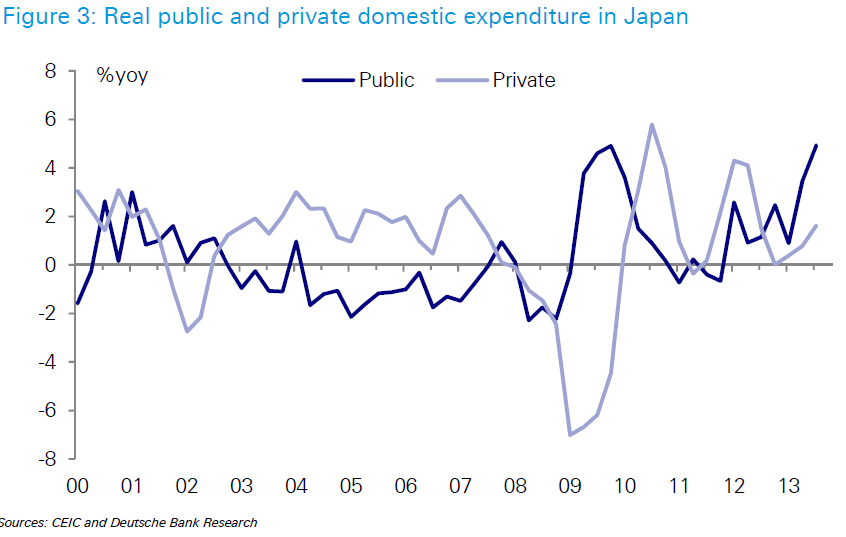

Initially private consumption surged in Japan on the back of the sharp rise in stock values which went hand in glove with the yen devaluation, rising by an annual 5.2% in March 2013. Subsequently it has fallen back and the rate of increase was just 1.1% in January, despite the “consume now” stimulus of a looming tax hike. In recent quarters what has most driven domestic demand has been private residential investment (in the anticipation that prices might finally start rising) and public spending on infrastructure projects as part of the “second arrow” stimulus programme (see chart below which comes from Deutshe Bank’s Michael Spencer).

The basic reason for the weakness in domestic consumption is obvious. Japanese real wages keep falling.

“Over the past 15 years, wages have dropped 15 percent. In the 11 months through November 2013, pay for the average worker rose only 0.2 percent. Households’ real income fell 1.7 percent in December from the previous year. Base wages, excluding overtime and bonuses, fell 0.2 percent in December, the 19th consecutive month they’ve dropped. The issue of wages, says Martin Schulz, an economist at Fujitsu Research Institute, “is a litmus test for whether Abenomics works or falls apart.””

Japan, Land of the Falling Wage By Bruce Einhorn, Jason Clenfield, and Yuko Takeo, Bloomberg

Naturally with so many different measures of wages and earnings to choose from, not everyone is convinced this is such a problem. FT Alphaville’s Cardiff Garcia, for example, has a good try at rescuing some sort of wheat from all the chaff in order to demonstrate that things aren’t as bad as they seem to be. Latching onto an argument presented by Capital Economics, he suggests that even with falling real hourly wages during an economic expansion if bonuses and employment growth mean that total earnings increase, so can consumption:

“The silver lining is that rising employment may partly offset the drag on aggregate incomes from falling real wages. Firms are happy to recruit more staff even if they are not yet ready to boost individual pay. Indeed, the total number of people in work has risen by around 1.5% in the last year. However, many of the new jobs are part-time, leaving most households still worse off.”

Capital Economics research report.

But is there really empirical evidence to back up the idea earnings are in fact increasing? And what about the forthcoming rise in consumer tax, that will surely add to inflation. In this sense it must be good for the economy, musn’t it? Not so fast say the editors at Japan Consuming, who in their February bulletin make the following very reasonable point:

Retailers are bracing themselves for consumer reaction to the increase in Consumption Tax. Retailers may be worried, but some consumers are looking at a serious change to their spending patterns if incomes don’t increase soon. Although the last tax rise in 1997 caused relatively minor sales disruption in the end, it came at a time when deflation was lowering prices and incomes were high – the highest on record in fact. This time around, incomes are falling just when prices are rising, making a sudden, doubling in direct taxes a potential disaster for the average Japanese household. But the situation is already bad: in the past year there has been a 24% fall in cumulative net annual disposable income, with the average family finishing with a [saving] surplus of less than half that of 2007. The surplus will be wiped out by the tax increase.

In 1997 an earlier LDP government increased the consumption tax to 5%, plunging the economy into recession. As now, in the year before the increase, consumers pushed up spending, but incomes on that occasion incomes were on the rise supporting consumption. The household saving surplus also hit a peak of ¥142,000 during the 12 months following the rise.

Fasting-forward to 2014, real average incomes are now 12% below the 1997 level. Expenditure too has fallen, if by slightly less: down 8.6%. On the other hand household saving for 2013 was 14.3% down on 1997 at just ¥106,962 per household, a fifth of one month’s income or just ¥8,900 a month on average. According to Japan consuming calculations, everything else being equal, a 3% rise in consumption tax will raise average monthly expenditure by ¥12,500 leaving a typical household ¥3,600 in arrears.

As they point out, these figures involve using a second average of the monthly averages of the past 12 months. So……….

“Taking the month to month cumulative totals of consumption expenditure and household disposable income, in 2007 total net disposable income exceeded expenditure by ¥393,493 for a typical two-person working household. This figure fell with the Lehmann Shock, but then rose slightly to ¥272,432 in 2011, still 30% down on 2007. It has since dropped further. In 2013, the generally increased levels of consumption were coupled with further falls in overall average disposable income. With a net short-fall of around ¥130,000 per household as of November, double the same month in 2012, more optimistic observers expected large end of year bonuses to turn this deficit around. These did not materialize – bonuses did rise in December 2013 but by only 2.8%, way down on the 6.4% rise in the summer. The result was an astonishing fall in cumulative net annual disposable income of 24% in the past year, with the average family finishing with a surplus of just ¥160,418, less than half that of 2007 on this basis.”

Ergo, even allowing for the impact of bonus payments and and increased part time employment net annual disposable income fell. Hardly a strong support for rising consumption.

Monetary Policy Impotence

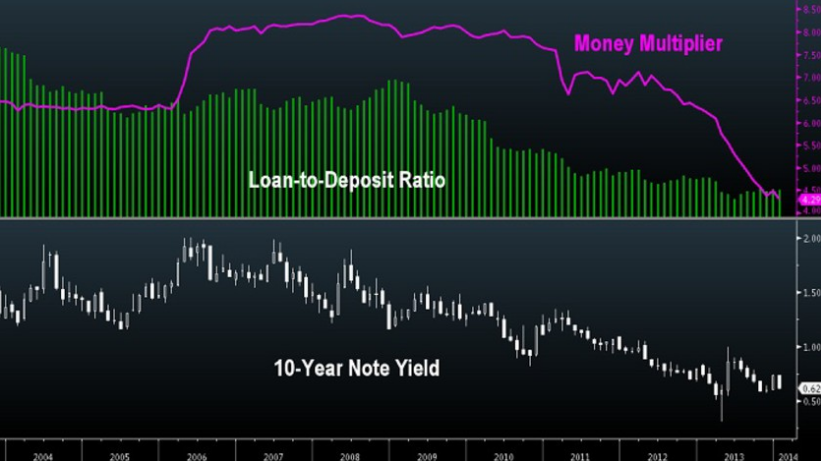

So what about credit? Isn’t that the mechanism which allows consumer spending to rise despite falling net incomes in countries like the US and the UK? Well not in Japan, as this Bloomberg chart of the day from February 20 makes plain.

The loan to deposit ratio in Japan’s banking system – at around 70% – is one of the lowest on record and the money multiplier fell in January to the lowest since 2003, when data became available, signaling the amount of money in the economy dropped relative to funds provided by the BOJ. Naturally, according to your preferred theory explaining what the problem is in Japan you will read this data one way or the other, but personally I see it as a clear sign of the decline in demand for loans which you could expect to see in a country with an ever older population.

Whichever way you look at it, it is clear that the preferred mechanism for overcoming deflation – using monetary policy to generate inflation expectations and increased “demand pull” inflation – simply isn’t working: the increase in base money isn’t passing through to broader money in the economy.

But it’s worse, the monetary expansion has driven down the value of the yen but in the context of the second arrow – a double digit fiscal deficit – this drop in value is leading to a growing not a declining trade deficit. The FT’s Tokyo bureau chief, Jonathan Soble, has an enlightening recent piece on this.

‘J-curve’ recovery eludes Shinzo Abe as trade deficit balloons

The widening of Japan’s trade deficit to an unprecedented Y2.79tn ($27.4bn) in January, more than Y1tn larger than the previous record, highlights a painful structural shift for an economy that has long relied on exports to drive its growth. For economists who follow Japan, the phenomenon might be called the case of the missing J-curve.

When the yen began falling sharply in late 2012, menaced by the threat of devaluation from Shinzo Abe, the soon-to-be prime minister, it made imports more expensive and dragged an already sizeable trade deficit more deeply into negative territory. That is exactly what economic textbooks predict would happen.

But theory, and past experience in Japan, suggested things would quickly turn round: consumers would respond to the rising cost of foreign goods by buying fewer of them, while Japan’s exports would become more competitive. Before long, the initial deterioration would be followed by an even more pronounced improvement: economists’ “J”-shaped curve.

Yet that has not happened. Instead, imports have continued to bound ahead of exports, creating ever-widening trade deficits and leaving Japan’s Abenomics recovery, the roughly year-old spurt of economic growth that has coincided with Mr Abe’s expansionary policies, reliant on domestic spending.

Stimulating the Unstimulatable?

But where is this domestic spending coming from? Not from earnings, nor from credit, as we have seen. It is coming from the government stimulus programme, which is, in an economy near its output potential, simply ballooning the trade deficit. “Sorry, what was that you just said?” “Run that past me again?” “In an economy running at near its potential output level?????” Yup, I think this is the heart of the problem. Most of the theories people are working on assume that the Japanese economy is running at way below potential, and that something extraordinary needs to be done to change this dynamic. As Larry Summers put it in his IMF speech, “we may well need, in the years ahead, to think about how we manage an economy in which the zero nominal interest rate is a chronic and systemic inhibitor of economic activity holding our economies back below their potential”.

But what if that view is wrong, and the aforementioned economies are not operating at below their potential.? What if their trend growth rates are systematically falling as populations age and working age populations fall?

And what if Japan’s deflation is a product of this process, rather than being a simple liquidity trap? In the words of former Bank of Japan governor Masaaki Shirakawa, “Seemingly, there would be no linkage between demography and deflation. But it may not be the case. A cross-country comparison among advanced economies reveals intriguing evidence: Over the decade of the 2000s, the population growth rate and inflation correlate positively across 24 advanced economies. That finding shows a sharp contrast with the recently waning correlation between money growth and inflation.”

If Shirakawa is right all the ongoing attempts to reflate the Japanese economy may be simply working against history, with the central bank governors sitting there, like modern Canutes, trying to order back the waves. Maybe the theoretical debate is far from over, but the evidence is mounting that Abenomics may lead Japan’s economy to shipwreck, tossed between the Charybdis of a growing external imbalance and the Scylla of a deflation driven monetary black hole.

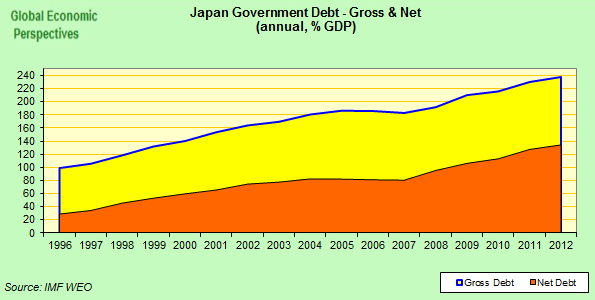

In the meantime, and while we decide, that government debt mountain simply grows and grows.

Comments are closed.