The Fed exerts a dominant influence across the yield curve, not just on the short end

Long-term interest rates are a series of future short-term rates. That necessarily means that an interest-rate targetting central bank exerts the dominant influence not just on the short end in its currency area, but across the yield curve. Nevertheless, a lot of people act like this isn’t true. The bond vigilante paradigm, for example, is a clear violation of this principal. Federal Reserve Board Chairman Ben Bernanke set the record straight in a speech yesterday at the Federal Reserve Bank of San Francisco.

The question: why are interest rates so low? The answer from Bernanke with emphasis added:

Why Are Long-Term Interest Rates So Low?

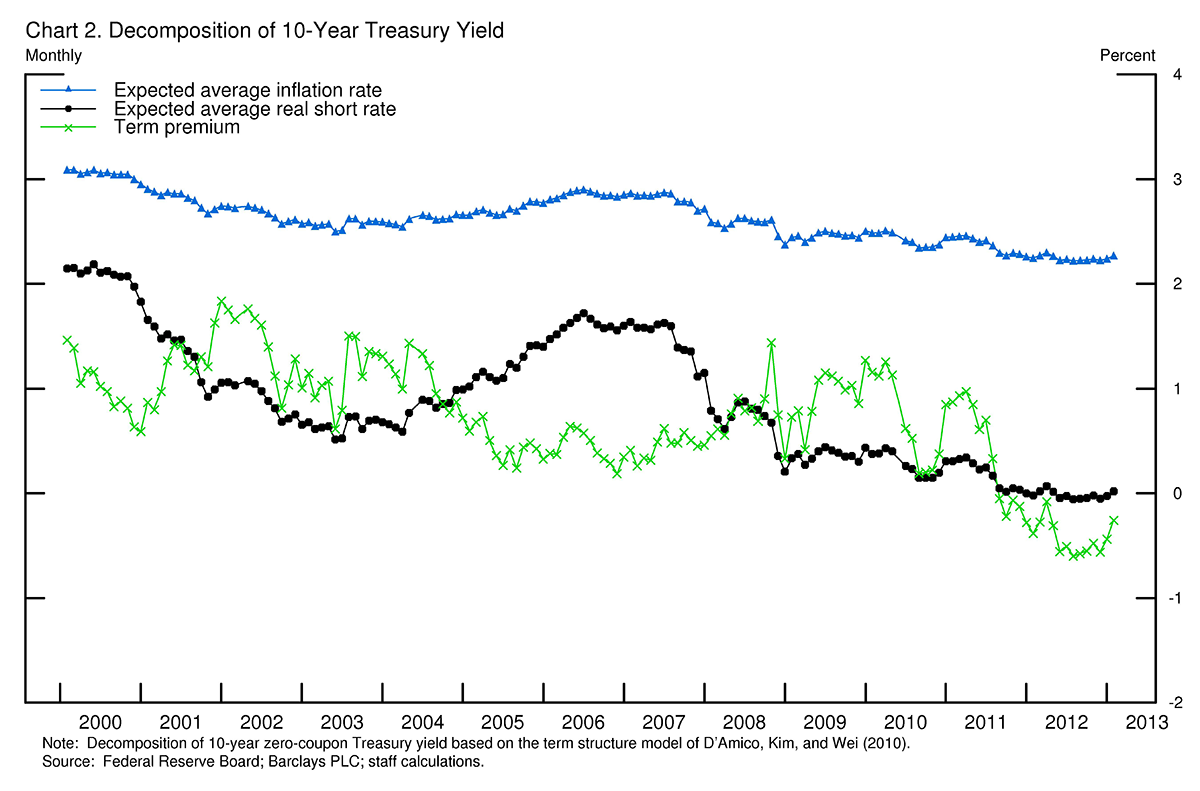

So, why are long-term interest rates currently so low? To help answer this question, it is useful to decompose longer-term yields into three components: one reflecting expected inflation over the term of the security; another capturing the expected path of short-term real, or inflation-adjusted, interest rates; and a residual component known as the term premium. Of course, none of these three components is observed directly, but there are standard ways of estimating them. Chart 2 displays one version of this decomposition of the 10-year U.S. Treasury yield based on a term structure model developed by Federal Reserve staff. The broad features I will emphasize are similar to those found by other authors using a variety of methods.

All three components of the 10-year yield have declined since 2007. The decomposition attributes much of the decline in the yield since 2010 to a sharp fall in the term premium, but the expected short-term real rate component also moved down significantly.

{kind=link}

Source: Federal Reserve Board

So, Ben Bernanke is telling you that longer-term yields are simply a series of inflation-adjusted expected future short-term rates with a term premium tacked on. I hope this explanation looks familiar because this is how I explained it in 2011:

“Here’s what is happening:

- The Federal Reserve is a monopolist. The US government, as monopoly issuer of its own currency, has given the Fed monopoly power in the market for base money. The Fed exercises this monopoly power by targeting the overnight rate for money, the fed funds rate

- Any monopolist can only control either price or quantity, not both. And the Fed wants to target rates i.e. price. It can’t do that unless it supplies banks with the reserves they desire to make loans at that rate. That means that they must be committed to supplying as many reserves as banks want/need in accordance with the lending that they do subject to their capital constraints. Failure to supply the reserves means failure to hit the federal funds rate target

- Markets know, therefore, that the Fed, as a monopolist, will always be able to hit its federal funds target now and in the future. Therefore, future overnight rates reflect only future Fed Funds target rates as set by the Federal Reserve. This means that future expected overnight rates reflect only market-determined median expectations of future Fed Funds target rates as set by the Federal Reserve (plus a risk premium). Long-term interest rates are a series of future short-term rates. All I need to do to mathematically represent any long-term interest rate is smash together a series of short-term interest-rates over the long-term period.”

This is exactly why, in the event of currency revulsion, the currency is the release valve and not interest rates. And this is also why government liabilities of sovereign currency issuers are always the safe haven asset for domestic investors – barring political insanity. People operating under the so-called bond vigilante paradigm simply don’t understand modern money.

What does this mean for investors?

- The US is not the next Greece. Anytime you here someone making the comparison, you can be assured that they either have no clue about modern money or they are playing you for a fool. Greece is a currency user that gave up monetary sovereignty willingly to join the euro zone. That’s why Greece defaulted and Italy is in a pickle and Japan is not.

- If foreigners start hatin’ on the US dollar, interest rates will not rise. The only reason interest rates rise when an interest-rate targeting central bank exists in a sovereign currency area is because that central bank has raised policy rates or investors expect it to do so. The currency is the release valve for currency revulsion, not interest rates. The question is whether anything – say, inflation – would force the central bank to raise policy rates. This is why people hating on Japan have been wrong for years – and will continue to be wrong until inflation takes hold in Japan.

- If you want to invest in the safe haven asset, all you need is a qualified view of future policy rates and inflation. As I wrote last week, regarding Britain, “the other stuff is irrelevant.” Ben Bernanke is telling you that.

- Central banks that telegraph policy will shift private portfolio preferences toward risk-on. Bernanke made his speech to reinforce the idea that the Fed wants to be as explicit as possible about the future path of policy rates in order to exert maximum influence on US government interest rates across the curve. What this means for bond investors is more certainty. And greater perceived certainty translates into investors taking greater risk and leverage.

Most importantly – and dangerously, if inflation and interest rate expectations remain both muted and relatively certain because the Federal Reserve is telegraphing future policy, investors will shift portfolios to higher-yielding and riskier asset classes. They will reach for yield, greatly altering the pattern of capital investment in the economy. Ceteris paribus, longer-lived, higher-yielding, riskier and more speculative investments will be made. This is exactly what is already occurring despite what Bernanke may be telling us.

Comments are closed.