A Hungarian Waltz On The Wild Side

By Edward Hugh

The Hungarian government’s much publicised unorthodox plans to cut the country’s public debt level has been attracting a lot of attention of late, both from the media and from the rating agencies. Some observers have been quite positively impressed. Fitch Ratings, for example, raised their outlook on Hungary’s sovereign credit rating in early June from negative to stable, citing government plans to reduce what is currently the largest accumulated public debt among the European Union’s eastern members. Others, however, continue to have their doubts. Moody’s, for example, has decided to maintain a negative outlook on the country’s due to concerns about the general trend in government policy, and the possibility of slippage with deficit objectives. Either way, these are changes within very defined margins, since at the end of the day, Fitch currently still rates Hungary at BBB- and Moody’s at Baa3, in both cases these ratings amount to the lowest investment grades.

Nor are the analysts any more unanimous. Christian Keller, head of emerging Europe research, Barclays Capital, feels the most challenged of the CEE economies have now gotten over the worst, and could now serve as role models for their Southern counterparts. Capital Economic’s Neil Shearing does not agree, and warns that those who suggest that emerging Europe will avoid contagion from the South could “prove to be being dangerously complacent”.

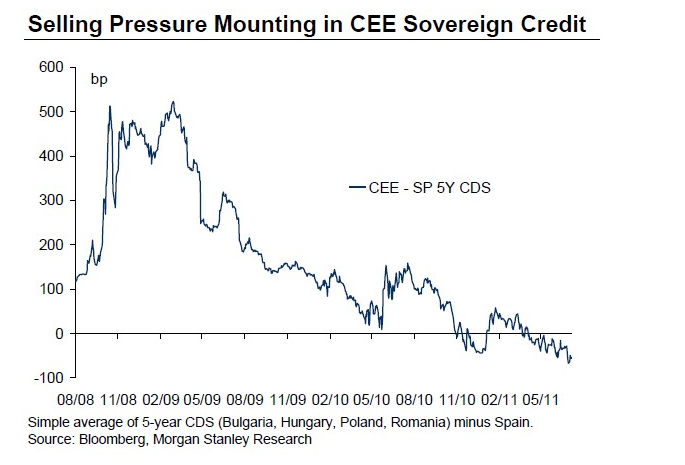

On the other hand Market sentiment seems to be much more with Fitch than Moody’s so far, since, as I highlighted in this post, Hungary’s CDS are now well below the highs of over 400 seen as recently as last November in the wake of the Irish crisis.

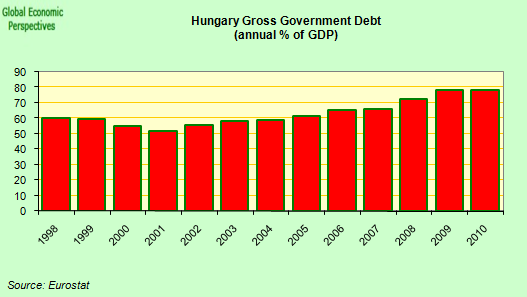

Arguably though the much maligned Moody’s have their finger more on the pulse in this case, since the way Hungarian risk is being treated by both Fitch and the CDS seems to reflect pretty optimistic assumptions. Not only is Hungary is the East European country with the highest gross government debt to GDP levels (around 80%), it also has very high gross foreign debt (around 135% of GDP, of which 45% is forex denominated), and it is a country where institutional quality is a constant cause for concern. The most glaring recent example of this is the decision to unilaterally liquidate the formerly mandatory private pension pillar, and recover the accumulated reserves for the coffers of the state system, a measure which at a stroke took 9% of GDP from the accumulated debt, and a lot of short term pressure from the deficit. Yet since the pension liabilities remain however you account for them, this is simply another kicking the can down the road move, and not a real example of a positive saving.

Indeed it is the predominance of this and other similar “one off” measures in the Hungarian debt stability programme which worries not only Moody’s, but also the EU Commission and the IMF.

“Central and Eastern Europe has remained fairly immune thus far from contagion, as financial stability and solvency among euro area peripheral countries as well as some quasi-core (Italy) countries have lately taken centre stage. One can argue that CEE has benefited from ‘benign neglect’ on the part of investors, who focused their attention elsewhere. However, this fragile equilibrium is not necessarily going to hold,”

Morgan Stanley Research Note

To some extent the scale of the debt in relation too its peers makes the country look very much like the Italy of the East – since 2006 the country has suffered from stubbornly low growth, the scale of the challenge involved in bringing about a real reduction in the sovereign debt has been consistently underestimated, and one administration followed by the next has relaxed in the comfort of continually rose tinted GDP growth forecasts.

But when we come to examine things in the cold clear light of detailed macro economic scrutiny, apart from the presence of a strong trade surplus there is not that much to commend in Hungary’s recent economic performance. So even though Hungary’s CDS and other risk measures have gradually fallen back in line with the regional pattern, we might well ask ourselves whether this will not be yet another case of a decoupling that wasn’t?

A Story Of Success Tinged With Failure

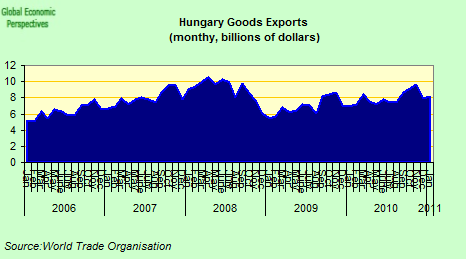

But let’s get things off on the right foot: not everything in the Hungarian economy is going badly. In the first place, and above all, exports are booming.

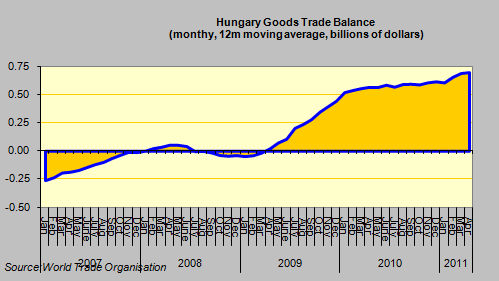

And the goods trade balance is impressive:

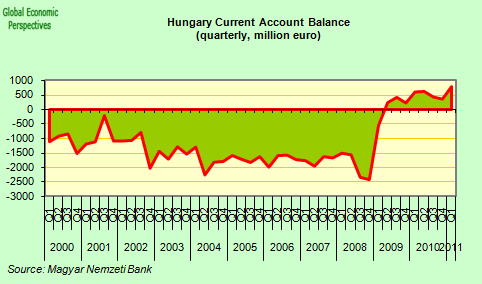

So obviously the country has been doing something right. The current account position has even turned positive:

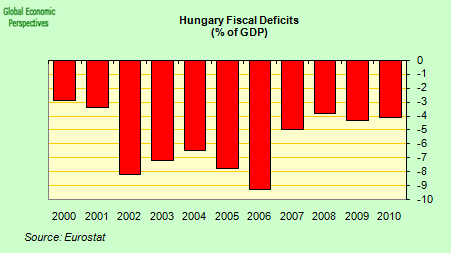

And the government deficit has improved substantially:

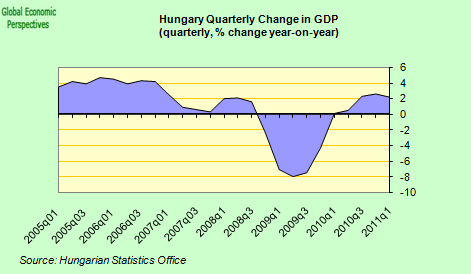

Growth has returned to the economy, following a peak to trough fall of over 7% fall during the financial crisis.

So that was the good news, what we might call the Hungarian success story. But unfortunately the story doesn’t end there, there is more.

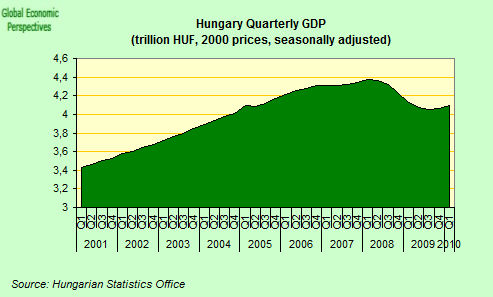

The apparently positive picture highlighted above conceals another, much more problematic and preoccupying one. Despite all that recent growth Hungarian GDP is still substantially below its pre-crisis peak. Indeed it is so far below that it remains at a level which was first attained at the end of 2005. That is to say, Hungarian GDP has effectively stood still for the last six years.

But while GDP has been marking time back there in the middle of the last decade, Hungarian debt certainly hasn’t been standing still. Officially recognised government debt reached around 80% of GDP in 2010, and while it may not rise significantly in the short term, this is both well above the 60% level the country needs to gain access to the Euro, and well above public debt levels in most of the country’s regional peers. The critical question is whether the policies being currently pursued will be able to bring that level back down again, or is Hungary, like Italy, in a knife edge situation where if growth and inflation are not sufficiently high, and interest rates begin to climb if risk sentiment turns against the country, the debt will start to climb upwards in a way which will be hard to control?

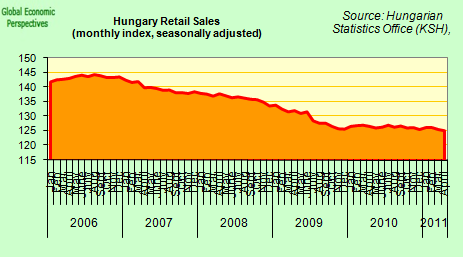

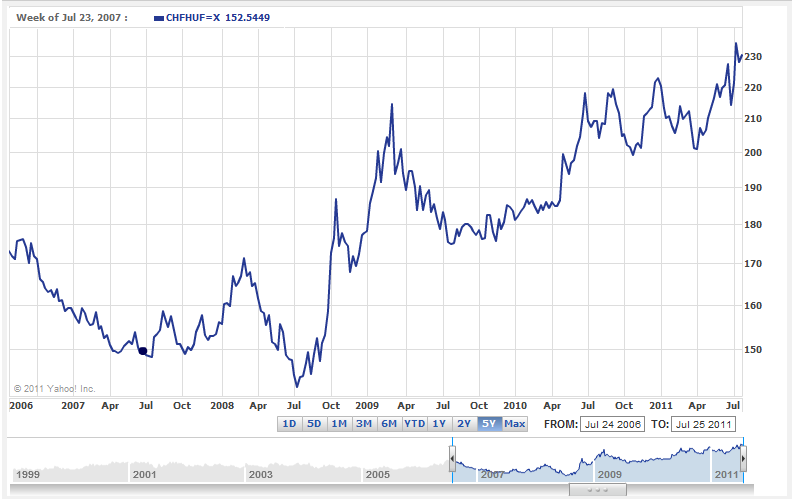

One of the factors which is sure to make it hard to achieve those ambitious government growth targets of 3% in 2011 and 3.3% in 2012 is the state of domestic demand, which is now in continuous decline on the back of a falling population and a significant credit squeeze produced by a heavy dependence of CHF borrowing. In fact retail sales have now been going down since mid 2006. They continue to fall, and it seems pretty unrealistic to imagine that this trend will now be reversed.

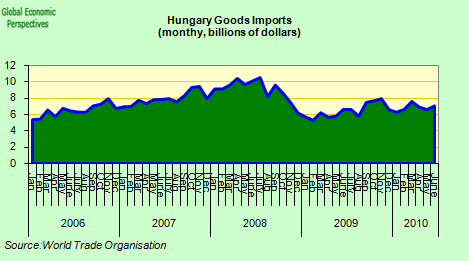

Which is why the strong trade surplus is as much a product of a slump in imports as it is of booming exports.

Private sector credit is effectively stagnant. Even the small apparent interannual rise in the value of outsanding mortgages shown in the chart below is a little deceptive, since the increase is almost all accounted for by the rising value of existing Swiss Franc mortgages (pushed up by the value of the CHF) and there is little if anything in the way of net new mortgage lending.

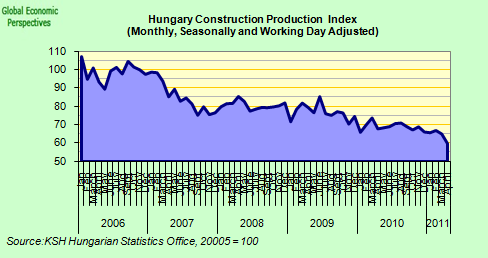

Which means the construction industry has entered what is now a rear terminal downsizing state. The industry is now only half the size it was at the start of 2006.

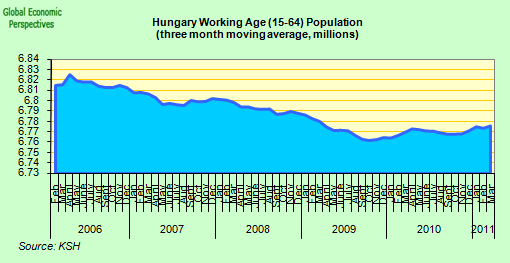

So while the Hungarian domestic economy and the country’s demography seem to symbolise one steady march towards the past,

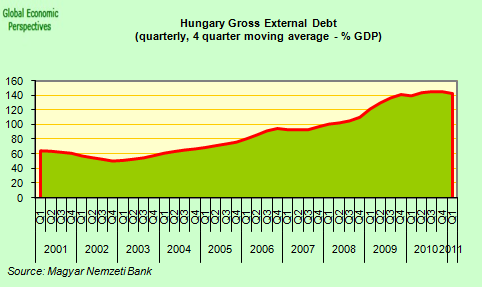

the face of the future can be seen from the level of indebtedness. While GDP, housing starts, car sales etc have all fallen, the one thing which has just kept growing and growing is the size of the country’s gross external debt, which stood at 135% of GDP at the end of the first quarter of 2011.

As The Global Economy Slows, Hungary Faces Growing Risk And An Uncertain Future

The recovery in the Hungarian economy remains weak due to a lack of domestic demand. After falling 14 percent in real terms in the 12 months to mid-2009, domestic demand has remained essentially flat. Still high unemployment, muted wage growth, falling consumer confidence, and stagnant credit are weighing on consumption. Meanwhile, fixed investment continues to decline amid considerable idle capacity, bottlenecks to credit supply, limited final demand, and an uncertain business environment. Recent data underscore concerns about the recovery: retail sales growth remains flat in early 2011 while the rate of decline in fixed investment actually accelerated in Q4 2010. Such weak demand has kept a lid on underlying inflationary pressures, while private real sector wage growth remained at historic lows.

IMF, Hungary: First Post-Program Monitoring Discussions, June 2011

The key points I wish to make in this post are as follows.

– There is a substantial contagion danger due to the current mispricing of risk, and the possibility of a sudden correction.

– There has been no real recovery in domestic demand, which means the country has to rely on exports, and this becomes difficult during a time of rapid economic slowdown elsewhere.

– The large proportion of external debt makes it difficult for the country to volutarily devalue, and indeed since 45% of government debt is non-forint-denominated any slippage in the HUF only pushes debt to GDP upwards.

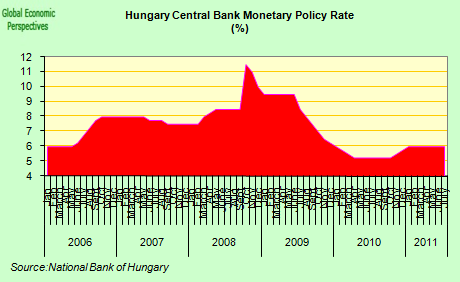

– To avoid slippage the country needs to maintain a comparatively high interest rate policy (currently the central bank benchmark rate is 6%) which makes it hard to apply monetary easing to stimulate demand.

This cocktail – less GDP (in comparison with before the crisis), less people, a smaller workforce accompanied by higher (and potentially growing as political pressures mount) debt – is inherently unstable and quite unsustainable in the longer run, and especially so if financing costs start to rise again and exports wane during any forthcoming Eurozone crisis.

One of the most worrying things about the current situation is the air of unreality which seems to surround recent policy initiatives. Indeed the Hungarian convergence programme itself is a rather amazing document, especially when it comes to the growth forecasts. Most worrying of all is the idea that policymakers may actually believe some of the own musings here, even though they verge on the world of fantasy. According to the document authors:

The Convergence Programme identifies two scenarios: one is a cautious and conservative path in which the positive effects of the Structural Reform Programme are manifest late and not with full effect. The other is a dynamic path of growth that assumes the successful handling and management of existing bottlenecks. The probability that the actual implementation of the plan resides somewhere between these two paths is 80%. In the dynamic scenario the risk premium will decrease in the long term and due to the incentives of the New Széchenyi Plan investment will grow at a higher level than in the conservative approach. These effects enhance capital accumulation and labour demand at the same time, improving the household’s disposable income and domestic demand. Under these favourable circumstances the Hungarian economy can grow at 4,8-5,5% in the period of 2013-2015.

So the Hungarian economy could grow between somewhere between 4.5% and 5.5% between 2013 and 2015? With all the known problems the Hungarian economy is facing! On which planet are these authors living? Fortunately neither the EU Commission nor the IMF have been taken in. The EU Commission has really yet to pronounce on the longer term forecasts, but their shorter term growth expectations (at 2.7% in 2011, and 2.6% in 2012) are significantly below those of the Hungarian government, while the IMF outlook at 2.8%, 3% and 3.2% (for 2013/14/15 respectively) is much more in the land of the living, even if it still sounds rather optimistic.

Then there is the political risk, which Moody’s draw attention to. You provide your voters with hopelessly unrealistic expectations, then somehow or another you try to find a way to comply, which normally implies higher rather than lower budget deficits. This is a possibility to which the IMF is currently extremely alert.

The 2010 general government deficit of 4.3 percent of GDP (ESA terms) exceeded its target by ½ percentage point— mainly at the local government level—despite a series of ad hoc corrective measures late in the year. This slippage implied a primary structural weakening of 1¾ percent of GDP in 2010, undoing much of the adjustment achieved during the 2008–10 Stand-By Arrangement (see the forthcoming Ex-Post Evaluation report). Poor budget performance continued into the start of 2011 where the first quarter central government cash deficit has already exceeded the government’s initial annual target, largely because revenues fell short of optimistic expectations.

IMF, Hungary: First Post-Program Monitoring Discussions, June 2011

In addition to the other worldly feel of government documents, the Swiss Franc exposure represents a big downside and potentially sizeable drag on Hungary’s prospects. As Moody’s note in their latest report on Hungarian banks:

“The large amount of foreign-currency lending to households underpins the rating agency’s expectation that asset quality will deteriorate further, as these borrowers’ ability to service their debt has weakened significantly following more than 30% depreciation of the forint against the Swiss franc in recent years,” Moody’s Vice President and Senior Analyst Simone Zampa, the author of the report, noted.

Unsurprisingly there are clear signs that the export sector is now feeling some of the pressure. The GKI economic-sentiment index declined for a third consecutive month in July, dropping to its weakest since April 2010, as confidence among both businesses and consumers deteriorated. Even more importantly, sentiment in the industrial sector, whose exports pulled the country out of recession, “deteriorated palpably in July,” according to the report. “The sentiment index in the industrial segment dropped especially significantly, the deteriorating trend has been in place for a quarter now.”

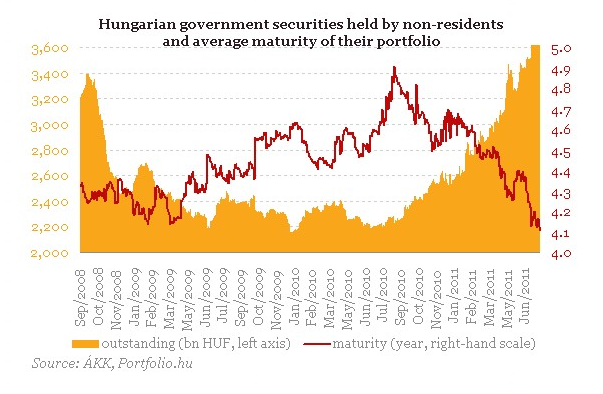

And the financing all that external debt represents another problem, especially as investors have taken more and more of it at shorter, and shorter maturities. As the IMF notes, financing the debt amortization schedule will be a particular challenge for the country in the coming years.

“Evidence is accumulating suggesting that the public debt reduction plan will prove much less than forecast, leaving Hungary more exposed to external vulnerability and failing to safely anchor the sovereign credit rating in investment grade territory…”This raises the question of whether Hungary’s fundamentals have improved enough to motivate a stable high foreign positioning and whether a further escalation in the Greek debt crisis will lead to a sharp sell off of the forint.”

Raffaella Tenconi, analyst at BofA Merrill Lynch

So problems enough, and, as the IMF emphasise, it is important not to let the calm of the current environment mislead, and produce complacency.

Fiscal slippages in 2010 and 2011 to date highlight the difficulty of translating policy intentions into results, particularly in the context of a still weak economy. In this context, the surplus in this year’s budget (which is entirely due to the one-off revenue effect of the de-facto nationalization of the second pension pillar) and the current benign market environment must not lead to complacency, especially in light of the electoral timetable and a challenging public debt amortization schedule after 2012.

IMF, Hungary: First Post-Program Monitoring Discussions, June 2011

This post first appeared on my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.

The fact that imports have collapse in the face of a weak domestic economy and so created a surplus looks good if you do not delve too deeply. I have had concerns about eastern Europe and Hungary in particular for two years.

Yes the population has fallen, probably by emigrating en masse. There are many Hungarians in the UK and I suspect anywhere where there work is possible. This demographic solution while keeping unemployment lower does not help growth prospects. Also it is dependant on exports which as you say could be very vulnerable when global trade slows down.

If there are problems in Hungary it will take down Austria’s banks. It will happen but just when. So how long before talk of contagion affecting Hungary?

I cannot see the economy growing at the stellar rates predicted. They have a debt burden which will be very hard to pay down. Especially since much is in foreign currency so would be adversely affected by a fall in the currency. This limits its ability to grow out of trouble. WIthout this handicap they could lower the currency and grow much faster. So the choice is between holding their population in debt servitude for years to avoid write-offs and losses for banks both home and abroad. That spells problems for the economy long term.