It’s the booming economy driving bond prices down, not Chinese selling

There are two things which warrant attention that are empirically wrong with the thesis that Chinese selling of US Treasuries will drive down prices. First, foreigners were net sellers of Treasuries when prices were rising. Second, Chinese selling would be in 2- or 3-year bonds, not at the long end where the selloff in Treasuries is occurring.

First, let’s remember that for years and years, we have been hearing that the bond vigilantes would come after the Japanese and eventually send their yields through the roof. That never happened, instead, yields have plummeted toward zero — even as Japanese government debt ballooned to well over 200% of GDP.

Then we were told, “well, that’s because the Japanese sell all of their government securities domestically, unlike the US. In the US, foreign bond vigilantes could dump Treasuries and yields would skyrocket, sending the US into a recession.” That’s already happened — at least the first part where foreigners ‘went on strike’.

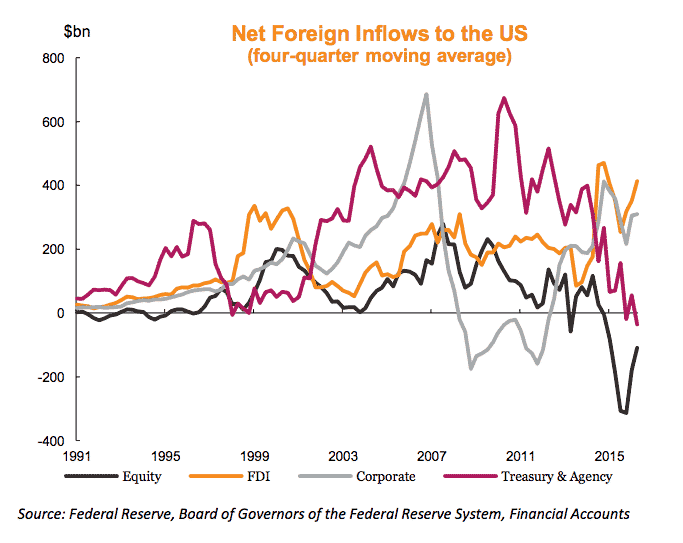

Take a look at the data through 2016

Source: Fulcrum Asset Management

The red line is foreign buying of US Treasury and agency securities. And you can see that level plummeting in the period from 2011 to 2016 (when the US Federal Reserve was engaged in quantitative easing). Meanwhile 10-year yields actually fell nearly a full percent.

Conclusion: Foreigners deserted the US treasury market for a five-year period and rates fell instead of rising. That doesn’t speak to the power of bond vigilantes, does it?

Now that US tax cuts are in the bag, a related question that a lot of serious people are asking is this: “Who Will Buy All the New Treasury Securities?”. That’s how Wells Fargo’s Economics Group put it in November.

Strong demand for U.S. Treasury securities in recent years, coupled with reduced issuance, has kept yields on those securities low. However, the supply-demand dynamics in the Treasury market may be changing. Issuance likely will ramp up significantly in the next two years as the federal deficit widens again. The Federal Reserve is effectively becoming a net seller of Treasury debt as it shrinks its balance sheet, and foreign central banks probably will not purchase as many Treasury bills, notes and bonds as they did during the past decade. If demand for Treasury securities falls short of supply at current prices, then yields will need to rise to clear the market. Indeed, we look for yields on Treasury debt to rise in the next two years.

Let me give a different argument, not based on flows and supply and demand. Treasury yields have risen recently, not because there’s more net issuance of government paper or because foreigners are net sellers, but rather because the economy has kicked it up a notch. We have seen two consecutive quarters of annualized growth over three percent and the headline unemployment rate is 4.1%. Meanwhile the Fed raised rates three times in 2017 and is poised to raise them three more times in 2018.

If you believe, as I do, that bond yields come from expected inflation, future short rates and a term premium, then it makes perfect sense to see yields rise and some modest steepening of the curve.

Bottom line: If yields were rising because the Chinese were selling or about to sell Treasuries — and that actually affected bond yields, it would be the 2- to 3-year space that we getting savaged. And we would see the curve flattening instead of steepening. Moreover, foreigners already became net sellers of Treasuries in the five years to 2016 and yields plummeted, even so. This speaks to lower inflation expectations more than supply and demand from abroad – which should have currency effects instead.

My view: Until we see slowing in the US economy, we should expect rates to rise somewhat and for a modest steepening of yields. If inflation starts to rise, expect these trends to become even more pronounced. And that’s when a cyclical bear market in bonds could begin. But by mid-year, I expect the economy to slow and for rates and term spreads to decline again. If net issuance of Treasuries does rise due to deficit spending, I expect this to have no impact on yields.

Source: Who Will Buy All the New Treasury Securities? – PDF – Well Fargo

Comments are closed.