Hedging against rising global political uncertainty

Starting in 2007, global markets were buffeted by a series of financial and economic crises that created the greatest deflationary scare since the Great Depression. We have left out-and-out crisis mode. But the challenges are still considerable, especially politically.

After the sovereign debt crisis ended in Europe, it was easy to think that we were in the clear economically and politically. But just as soon as the crisis in Europe ended, we had a major energy investment crisis. And after a brief recovery, this energy investment crisis is set to re-emerge against a backdrop of increased global political risk. Here’s my take on the issues.

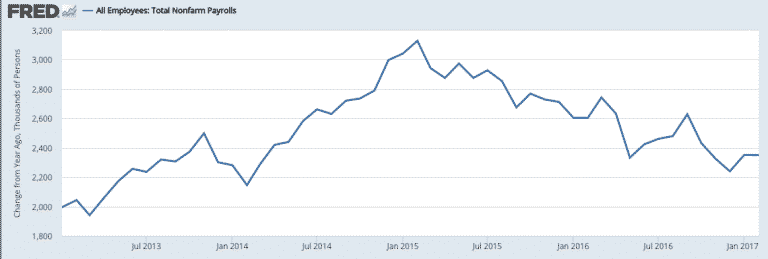

First, on the energy question, we now know that a major downturn in the energy sector due to falling prices is not stimulative to the economy. What we saw in 2014 and 2015 was a massive wave of capital expenditure cuts and bond market distress that overwhelmed the positive impact of lower prices on global consumer demand. In fact, if you track the moving average of US non-farm payrolls over the past several years, you see a measurable downdraft in jobs added to the economy when the price falls caused energy capex cuts.

And while the deceleration in payroll growth is consistent with what one should expect in a tightening labor market, the timing and slope of the curve demonstrate the influence from the energy sector overwhelmed all other factors.

The fundamental issue that created the oversupply in the energy sector has not gone away. It has perhaps worsened. The fact is that shale oil production adds a lot of incremental production capacity at relatively short lead times when that production is economically viable. The initial downdraft in oil prices was arrested because we hit a wall on the marginal cost of shale production of so many outfits that rig counts plummeted dramatically and future capital expenditure ensured that production would not ramp up quickly.

Since the initial rout in oil though, marginal costs have gone down and rig count has gone way up again, resulting in a massive oversupply of almost 280 million barrels compared to the five-year average. As we see US rig count at the highest levels since September 2015 right now, the oversupply of oil is set to persist until price pressure causes production to decline.Likely this means another rout in oil prices. And given the negative impact the last rout had on capex, jobs and demand, we should read this as a net negative for global growth. This outcome is particularly negative for emerging markets, as it intensifies the likelihood of a strong dollar environment. It also means high yield is vulnerable. And it makes further yield curve flattening in the US a further risk.

The political backdrop to the market risk is negative. As I said early in the year, the tensions with Russia and China are known. It was Turkey’s role as a bridge country between the Middle East and the West and its strained relationship with the EU that I believe presented the greatest ‘Black Swan’ risk. And we now see with the row over Turkish referendum campaigning in EU countries that that risk is starting to crystallize.

But there is one additional risk I want to mention briefly: France. The talking point on France revolves around Marine Le Pen winning the election and breaking up the eurozone. Three things here:

First, I don’t think Le Pen can do it. And as a result, I see the breakup risk for the euro as a longer-term risk — of building anti-EU, anti-euro sentiment, most likely to come to a head in a recession. Second, the uncertainty is Knightian i.e. it can’t be modelled or hedged. And so present spreads cannot possibly reflect reasonable worst case outcomes because no manner of hedging is going to be able to deal with the risk associated with potential redenomination in Europe; the cost of those hedges is too expensive relative to the near-term likelihood of the risk crystallizing.

But there’s another unspoken risk in France – and that involves French Presidential frontrunner Emmanuel Macron. Previous frontrunner François Fillon’s travails continue, as it was revealed today that his daughter had recycled 70% of her ‘salary’ back to her parents. Fillon seems very unlikely to survive this scandal to make it into the second round of voting in my view. That leaves Macron in pole position. But Macron as President is a ‘bad’ outcome for stability since he has no political base. his election would create uncertainty because it would make the likelihood of a weak presidency greater.

Europe is at the center of too many of the risks to advocate an overweight in Europe given the backdrop. And certainly emerging markets present their own risks. My view here is that should an oversupply-induced oil rout take place, the likelihood of more Fed rate hikes diminishes rather quickly. And given recent worries about US 10-year yields breaking out of a 30-year down channel to the upside, a bullish US government bond view is worth considering.

Comments are closed.