Trade war escalation highlights downside economic risks

The big story today is the potential for a currency war, emanating from the escalating trade war between the US and China. But there’s a considerable degree of data flow that I want to parse to give a more complete macro view.

Having looked at the data already though, my overriding sense here is that it makes the case for Fed easing at the next FOMC meeting in September stronger, with financial conditions tightening due to continued geopolitical tension. On the economic front, I still believe a 2019 US recession is off the table. But, it is still y base case for 2020, with policy error a major reason why.

More complete analysis below

The currency war

When US President Trump escalated the trade war with China last week by saying he was going to impose 10% tariffs on $300 billion worth of Chinese goods, here’s how I put it after the Yuan skidded on Friday in reaction:

New tariffs give China the excuse they need to make this a currency war

— Edward Harrison (@edwardnh) August 2, 2019

And, indeed, on Monday, the Yuan fell even more, breaking through the psychologically important 7 barrier for the first time in 11 years. Patrick Chovanec’s comments on the price action made the most sense to me:

In this case, China is not weakening its currency, the market is, in direct response to the potential impact of the new tariffs President Trump just announced. Like it or not, he’s the one weakening the yuan – the Chinese, for once, just aren’t fighting it.

— Patrick Chovanec (@prchovanec) August 5, 2019

The Chinese currency regime is a hybrid. The currency doesn’t float but it’s not pegged. And that gives the Chinese an extra measure of control that Trump doesn’t have in the trade war. They can let the market dictate the Yuan’s direction to a certain degree, taking some of the sting out of the tariffs for Chinese exporters. And they can reasonably claim they are simply following the market by choosing not to prop up their currency as the market (understandably and predictably) makes part of the economic adjustment through the currency.

Is this a currency war? It isn’t quite yet. After all, despite the fact that the Chinese have better capital controls now than they did after their mini-devaluation in 2015, they still have to be concerned about capital flight if the currency falls too quickly.

But Trump could change their approach. His tact is about asserting maximum pressure when he believes he has the upper hand. And it’s clear he believes he has the upper hand now. So he may escalate. And if he does, the Chinese will not back down. That’s my view. After all, China is reported to have asked its state-owned companies to cease buying U.S. agricultural products as retaliation for tariffs, hitting Trump where it hurts politically. That doesn’t sound like a roll over and surrender or wait and see strategy.

So, as we think of potential outcomes, policy error has to be a real concern here, especially in 2020 once the cumulative impact of all this takes its full measure.

The US data are mixed

This morning we got a few new data points on the health of the US economy. And Markit’s data showed strength in the US, while ISM data showed weakness.

Markit’s Services PMI for July came in at 53.0, ahead of expectations for 52.2 and above June’s 52.2. That pulled the Composite PMI up to 52.6, ahead of expectations for 5q.6 and June’s 51.6 reading. None of those readings is particularly strong. But at least the direction is good.

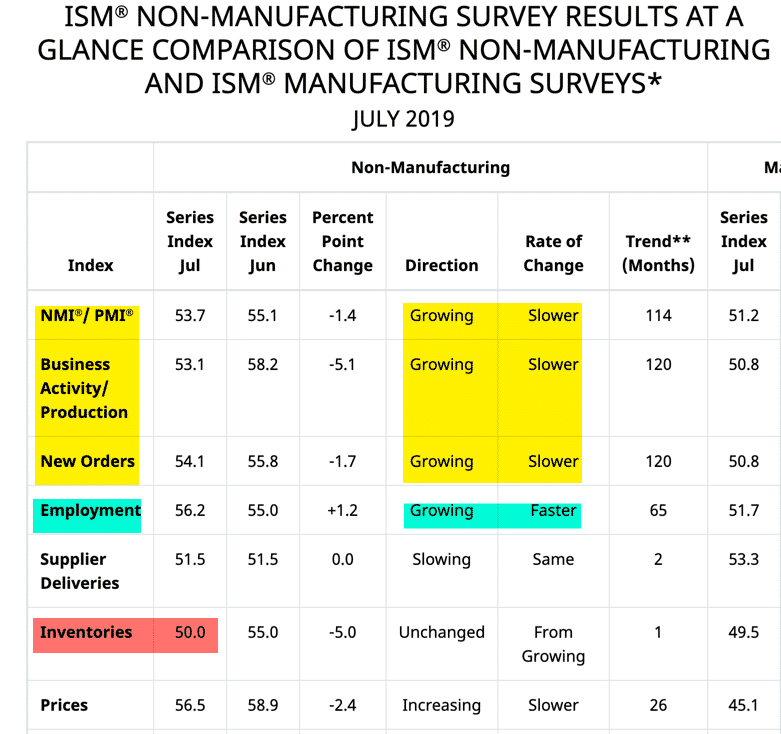

But soon after this data set came out, ISM rained on our parade with weak Non Manufacturing numbers, 53.7 versus a forecast for 55.5 and 55.1 in June. The internals were weak too, except for employment, which is lagging.

Inventories were particularly weak. Notable comments from survey were: “Letting supplies run lower than normal to keep expenses down” and “Demand lower than expected.”

For me, the inventories read is a huge warning sign about the lack of strength in the headline growth numbers in the US.

Manufacturing has been weak in the US. Now, we are seeing the services sector weaken as well. Remember, I had been saying I expected the services sector to pull the manufacturing sector up. But what we are seeing is the services sector is weakening to join the manufacturing sector, with employment lagging on the way down. What that could mean is that firms are running down inventories and waiting to make employment decisions. But, if things do not turn around, they are going to lower the boom. And employment will also follow down.

Something to consider

The Fed’s decision

I think the Fed will cut in September. That’s what it looks like now. Financial conditions have tightened considerably since the Fed cut last week due to trade uncertainty, with stocks and bond yields both tumbling. And the real economy data looks weak enough that the Fed will be forced to act pre-emptively. At this point, I think it could even cut 50 basis points.

The Fed’s cutting will have little real impact though. Most of this will be driven at the margin by sentiment, with financial conditions easing or tightening based on the rhetoric coming out of the White House and out of China. Escalating geopolitical tension will only exacerbate any risk-off sentiment — with employment now the last holdout in the US on the upside. So, the margin is think here. More risk-off sentiment could, indeed, bring us to a point where it feeds through to the real economy and creates a tipping point.

So, to the degree that economic slowing continues, we do have to be worried that it eventually leads to a recession, one that the Fed cannot prevent.

Brexit

Speaking of policy errors, let’s remember that Brexit is in the background, with the UK set to leave the EU on October 31st. This is a whole separate discussion, given the tenuous hold the Conservative Party has on Parliament right now. But I wouldn’t rule out a no-deal scenario. That’s either a base case or close to it in most reasonable decision tree matrices. And what happens then is unknown.

What we do know is that with Phillip Hammond out of office as Chancellor of the Exchequer, the UK is poised to add fiscal stimulus to act as a counterweight to any fallout – as it should be. I suggest you read “Fiscal stimulus underpins Boris Johnson’s strategy” in today’s FT for details. The numbers I hear bandied about seem small relative to the shock a no-deal Brexit could induce. But the new anti-austerity push does highlight the policy freedom the UK enjoys.

And notice that yields on long-dated UK government bonds are at all-time lows, even lower than after Brexit, as Johnson ramps up the spending rhetoric. It tells you that the convergence to zero is on in a big way. As growth slows, this is the most important theme dominating asset markets today in my view.

Happy Monday!

Comments are closed.