Monopsony in the UK

By Will Abel, Silvana Tenreyro, and Gregory Thwaites

This post first appeared on Vox.

The growing prominence of giant companies in advanced economies has raised concerns about the increase in monopoly power (e.g. Eeckhout and de Loecker 2018). Most attention has focused on the markets in which these firms sell. With market power, firms in an industry may set prices higher, and produce less in aggregate, than they would if the industry were more competitive (Gutierrez and Philippon 2017).

But firms can also dominate the markets in which they are buyers – especially labour markets. Monopsony power, first studied by Robinson (1969), arises when an employer faces little competition for workers from other firms, and can set wages at a level lower than would be the case in a competitive market. Manning (2003) outlined how monopsonistic labour markets are more likely to emerge when employees do not have enough information about work opportunities, and mobility costs are high.

In new research (Abel et al. 2018) we use employee-level micro-data to find out the extent of monopsony power, its effects on wages, and what determines these effects in the UK’s private sector from 1998 to 2017. Using a 1% representative sample of all employees, along with unique firm identifiers, we are able to construct industry-region measures of concentration in employment over time.

Specifically, we construct a Herfindahl-Hirschman index (HHI) to measure the concentration of employment among firms in a labour market. An HHI is a typical measure of concentration which ranges from 0 to 1. A score of 1 indicates a completely concentrated market, with only one employer and lower scores indicate higher levels of competition in the market. We construct our HHI at an industry-year-region level, where industry is measured at the 2-digit SIC level, and we use NUTS2 (roughly county-level) regions. This divides our data into 85 industries, 39 regions and 19 years, a total of 62,985 concentration measures in our dataset.

No long-run trend in aggregate labour-market concentration in the UK

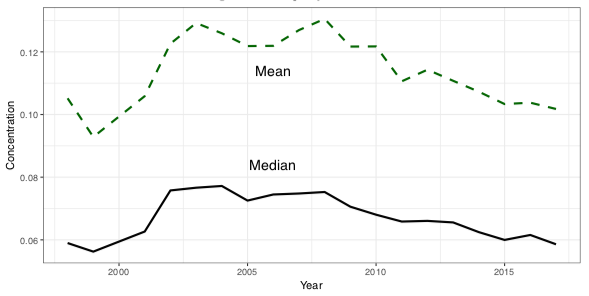

Figure 1 shows a time series for the median and mean level of concentration faced by employees over time. Between 1998 and 2017, the mean labour market concentration fell by 1% and the median by 3%, and so concentration levels at the end of our sample are similar to those at the start. There is, however, substantial rise and fall during this period. From 1998 to 2008, mean and median concentrations increased by 24% and 28% respectively. They subsequently declined to their starting levels.

Figure 1 Median and mean level of concentration of employment in the UK private sector, 1998-2017

Source: Abel et al. (2018).

Variation in concentration across industries and regions

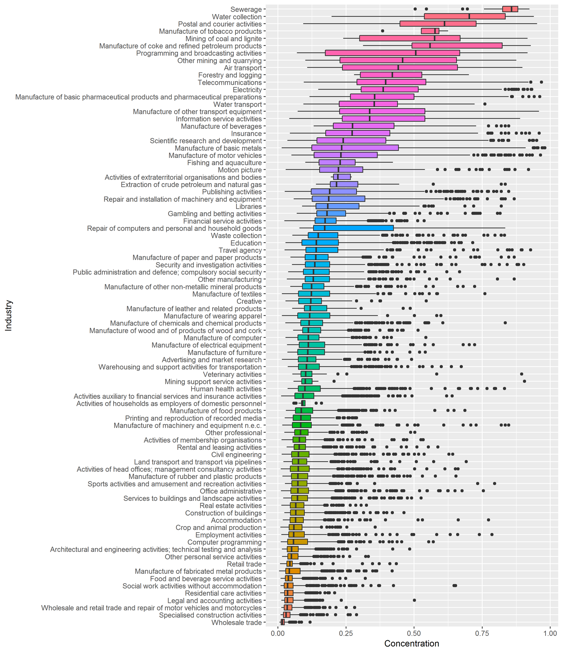

Behind this relative stability in the aggregate time series, there is substantial variation at the cross-sectional level. Figure 2 shows the distribution of concentration measures by industry – where each observation represents an industry-region-year concentration measure.

Figure 2 Concentration of employment in the UK private sector by industry, 1998-2017

Source: Abel et al. (2018).

Two features are clear:

- There is large, expected variation in concentration between industries. There is high competition for workers in retail and residential care industries, for example, while there are relatively few employers in industries such as sewerage, mining and courier services.

- There is a strong rightwards skew to the data. Even in competitive industries, some workers still face highly monopsonistic labour markets. There is some regional variation: the relatively sparsely populated regions of South Yorkshire, the Highlands, and Cumbria are the most concentrated regional markets. West London, East Anglia, and Oxfordshire are the least concentrated. But there is substantially more within-region than between-region variation. Even workers in parts of Manchester or London face highly concentrated labour markets, depending on their industry of work.

So, while there are large variations in labour market concentration across industries and regions, aggregate measures of labour market concentration have been remarkably stable.

Concentration and wages

The next step is to examine the relationship between concentration and wages. We regress the worker’s gross weekly wage per head on the HHI for their (region-industry-date) labour market, plus a set of worker- and firm-level characteristics, and region, industry and time fixed effects.

Conditional on these controls, there is a small negative correlation between labour market concentration which is not statistically significant at standard levels. In other words, we have only weak evidence that labour market concentration affects wages.

The picture changes substantially when we distinguish between those workers who are covered by collective bargaining agreements (CBAs), which are union-negotiated pay agreements that may also apply to non-union members. There is now a large, precisely estimated, significant negative correlation between concentration – but only for workers not covered by a CBA. Moving from the 25th to the 75th percentile of concentration is associated with a decline in pay of 1.1%.

Given that CBA coverage declined from around half of private sector workers in 1998 to around one-fifth in 2017, concentration is having a bigger impact today, even though markets are not on average more concentrated than they used to be. Also, when we allow the effect of concentration to vary by both firm productivity and CBA coverage, we find that at high-productivity firms, higher employer concentration is associated with lower pay for workers regardless of CBA coverage.

Take monopsony seriously when assessing mergers

There has so far not been much work like this on the extent and effects of labour-market monopsony. Our approach and findings are very close to those of Benmelech et al. (2018). They focus exclusively on US manufacturing firms, representing around 9% of current employment, and also find a negative relation between employer concentration and wages, that union membership (related to, but distinct from, CBA coverage) weakens this relationship, and that the link between productivity and wages is lower in more concentrated labour markets. The magnitude of their effects is comparable to those we find for the whole UK economy. But Benmelech et al. find that labour-market concentration has been increasing over time in the US, we find these measures are relatively unchanged in the UK.

Azar et al. (2017) also look at the effects of monopsony power on wage growth in the US, and find a negative relationship between the two. Their results are around 10 to 15 times larger than those we find.

This work shows that labour market concentration has an important effect on wages when there is no collective bargaining. An important policy implication is that antitrust authorities should consider the impact of proposed mergers on market power in labour and other input markets, as well as in product markets.

References

De Loecker, J and J Eeckhout (2018), “Global market power”, NBER Working Paper No. w24768.

Gutiérrez, G and T Philippon (2017), “Declining Competition and Investment in the US”, NBER Working Paper No. w23583.

Robinson, J (1969), The economics of imperfect competition, Springer.

Manning, A (2003), Monopsony in motion: Imperfect competition in labor markets, Princeton University Press.

Abel, W, S Tenreyro, and G Thwaites (2018), “Monopsony in the UK”, CEPR Discussion Paper 13265.

Benmelech, E, N Bergman, and H Kim (2018), “Strong employers and weak employees: How does employer concentration affect wages?”, NBER Working Paper No. w24307.

Azar, J, I Marinescu, and M I Steinbaum (2017), “Labor market concentration”, NBER Working Paper No. w24147.

Comments are closed.