Is Japan Back In Recession?

By Edward Hugh

“People should seriously consider that Japan’s economy may have fallen into recession despite the weaker yen and a stock rally from the BOJ’s easing and the flexible fiscal policy by Abe’s administration,” said Maiko Noguchi, senior economist at Daiwa Securities. “Initial expectations that the economy could withstand the negative effects of a sales tax hike through a virtuous circle seem to be collapsing.”

“the risks are rising that the economy will later be determined to be in recession,” said Yuji Shimanaka, chief economist at Mitsubishi UFJ Morgan Stanley Securities Co.

Worsening Picture

As noted in my post – Does Abenomics Work? – (published 19 September) the tide of media opinion finally seems to be turning against Shinzo Abe and his economic reform plan for Japan known as “Abenomics”. The degree of skepticism being shown only seems to have grown on the back of a slew of recent data confirming the impression that the recovery of economic activity from the post sales-tax slump isn’t going to be as easy as either the Japanese government or the Bank of Japan initially thought it would be. As the authors of the Bloomberg report from which the above quotes are taken – Oops Japan Did It Again? Sales-Tax Spurs Recession Debate – put it: “Weak industrial production data from Japan today raises concern that the world’s third-largest economy may be back in recession, challenging Prime Minister Shinzo Abe’s growth strategy.” In fact, output which was down 1.5% between July and August (and down 2.9% over August 2013) has fallen in three of the past five months.

Other indicators point in a similar direction. Household spending was down 4.7% year on year in August, and the coincident composite index, which consists of 11 key indicators, including retail sales and industrial production, fell 1.4 points to 108.5, according to the Cabinet Office this week. The August drop was the the first fall since June.

Even corporates are becoming more gloomy. The latest Bank of Japan quarterly Tankan confidence survey fell back three points from June, the second successive fall since it peaked just before the tax hike.

{kind=link}

As the FT’s Ben McLannahan points out the Tankan numbers also suggested that “the recent drop in the yen – which fell more than 5 per cent against the US dollar in September – remains a double-edged sword for Japan Inc, pushing up profits for big exporters with extensive overseas operations while squeezing the margins of smaller manufacturers, which struggle to pass on the higher cost of imports.” Unsurprisingly it is the small manufacturers who are most disgruntled about the impact of Abenomics.

The economy fell between April and June by an annualized 7.1% and even though the rate of decline will have been much slower from July to September all the indications seem to point towards the possibility that growth was negative, which would mean that at least technically Japan is back in recession.

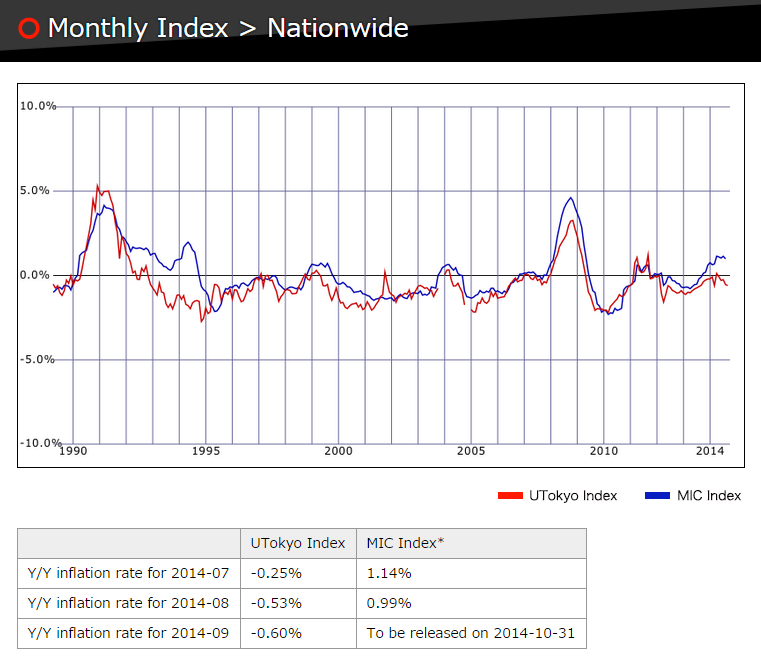

Abe is having more success with inflation, which is running at the highest level in nearly two decades. Yet even the inflation – which is at an annual 1.3% once you strip out the effects of the tax hike – has largely been driven by the rising cost of imports, and there are serious doubts whether even this will be sustained if there are not further yen devaluations. The Tokyo University frequently purchased items index (obtained from supermarket scanner data) shows underlying inflation continuing to ease.

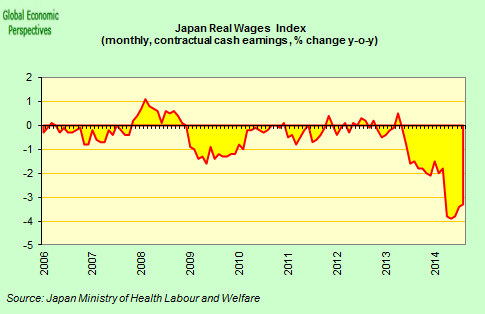

But even the inflation proves to be problematic in a country where wages

constantly fail to rise significantly. The fact that non inflation adjusted

monthly wages rose at the highest rate in I don’t know how many years makes a nice

headline, but the fact that real take home pay keeps falling

due to the impact of inflation gives a more realistic description of the difficulties involved in trying to refloat Japanese consumption..

The theory that is being applied assumes that Japan is in some sort of “temporary” liquidity trap due to the presence of a balance sheet recession, but what if the trap is permanent rather than temporary – see my Paul Krugman’s bicycling problem – and is the result of the country’s demographic evolution. In that case what – apart from all participating in a mass Labour of Sysiphus – do we really hope to achieve?

A policy which is exclusively aimed at attaining a positive natural rate of interest when the natural rate may be permanently negative seems of dubious value at the least, and when this policy in addition proves unable to drag the economy stably out of recession and only benefits the 10% of the Japanese population who have financial assets and senior management in large global companies, then in its application it seems almost to be noxious. A state of affairs which doesn’t escape the attention of the average Japanese in the street.

Falling Popularity

The popularity of Prime Minister Shinzo Abe’s cabinet was falling sharply going into the summer, forcing him to stage a reshuffle in September. The current approval rating is now back up at 64% but if the country’s economic fortunes don’t improve it will surely start to head back down again. On the critical question of whether to go ahead with next October’s second tax hike, some 68% of those interviewed in the most recent survey say they are opposed while only 28% supported implementation.

Most market participants assume that the Bank of Japan will react to further bad news by increasing the rate of Japan Government Bond purchases, but it is far from clear that this will happen. Indeed only this week Bloomberg reports that members of the governing Liberal Democratic Party’s governing council are starting to call for the formulation of an exit strategy from the yen weakening process as the debate over the policy’s pros and cons grows steadily more intense.

Meanwhile the Japanese government recently announced that the number of people over 65 reached 25.9% of the population in September – up 1.1 million from a year earlier. Tic-toc, tic-toc.

***************************************************************

The above analysis is based on arguments which are fleshed out in much greater detail in my “mini book” the A B E of Economics.

The book is available with Amazon as an e-book. It can be found here.

You don’t need to buy a Kindle to read this book. You can download a free app from Amazon.

Comments are closed.