US credit risk appetite hits euphoria

By Sober Look

Per earlier post (see discussion and chart), corporate spreads in the US are grinding lower – with new post-recession lows for both IG and HY spreads. The Merrill HY Index spread is now below 400bp and the investment grade equivalent is below 130bp. For those who track fixed income ETFs, the following chart comparing treasuries with corporate bonds (LQD vs. IEF and HYG vs. IEI) illustrates the extend of spread compression.

In fact US corporate credit is outperforming other forms of credit assets such as commercial real estate (see post). A good way to see that outperformance vs. global risk assets is in the components of the Credit Suisse Risk Appetite Index. For the first time since Bernanke began hinting about taper, US Credit Risk Appetite is at the level of “euphoria”.

|

| Source: Credit Suisse |

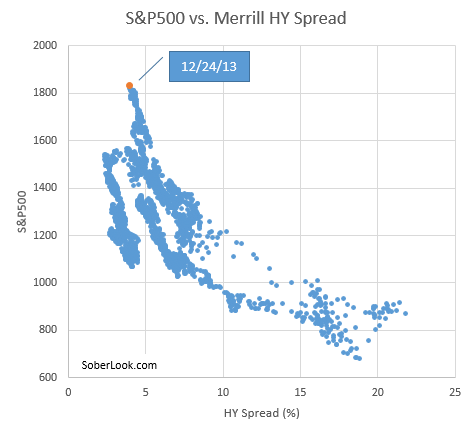

But some argue that these credit spread levels are justified given where the US stock market is currently valued. The scatter plot below shows the S&P500 index vs the HY index spread over the past 10 years. The last time spreads were at these levels (2007), equities were priced much lower (S&P500 was around 1550). Of course corporate revenue has grown substantially since then making this comparison less relevant. Nevertheless some are suggesting that it’s the stock market which is overvalued relative to credit.

Whatever the case, as monetary conditions in the US begin to tighten and interest rates rise, credit spread compression has to slow or reverse. The current trend is simply not sustainable.

Comments are closed.