Get Them to the Greek (Writedowns) – IASB

By Global Macro Monitor

Wow! Just came across this piece from the FT about the concerns of the International Accounting Standards Board (IASB) of how European financial institutions have not reserved enough against potential credit losses on their Greece sovereign bond holdings. Are these guys reading the Global Macro Monitor? Recall our piece posted on Friday,

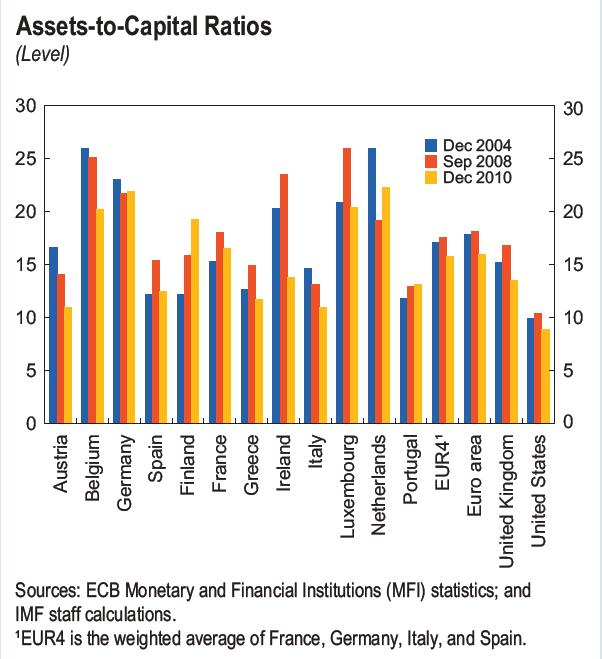

…all of the bailouts have been a de facto attempt to recapitalize European banks, who would have taken massive hits in the event of defaults in the periphery and thus collapsing the European financial system. The problem is, as far as we can see, the European banks continue to report decent earnings failing to take sufficient reserves against their sovereign exposure, which would be painful, but necessary, and result in reporting losses. European banks are relatively thinly capitalized to begin with…Where is the European Banking Authority? Every euro the banks receive in backdoor bailout money as the periphery bonds mature and get paid by the European taxpayer should go into loan loss reserves. It appears some banks have just begun to take the hits and to allocate specific reserves against their sovereign exposure to the periphery.

{kind=link}

This is what today’s FT piece had to say,

In a private letter sent to the European Securities and Markets Authority, the European Union’s market regulator, the International Accounting Standards Board criticised the inconsistent way in which banks and insurers have been writing down the value of their Greek sovereign debt. “This is a matter of great concern to us,” Hans Hoogervorst, IASB chairman, said in the letter, which was seen by the Financial Times.

People familiar with the IASB’s letter said the intervention was unprecedented and reflected its belief that some European companies had not been making enough provisions for Greek sovereign debt losses.

Makes you go hmmmmmm! Others are reaching the same (and correct, in our opinion) conclusion after assessing the situation. Judge Robert Bork used the following analogy to explain what appeared to be collusion between several parties,

If you pull up to an intersection and five people sitting at the bus stop all simultaneously raise their umbrellas, it doesn’t necessarily follow they have colluded to do so. It could be they were all reacting to the same external force – rain!

This is important stuff. Breaking the destabilizing feedback loop between sovereign debt and the European banking system is a necessary condition for a sustainable market rally and global recovery. The problem is that most of Europe is still in denial though the IMF’s Christine Lagarde, the former French FinMin, gets it. Be sure to read the full FT piece and review our Friday’s post.

Actually rather than trying to break the link between sovereign debt and the European banks let it runs its natural course. It will end up with massive write-offs by the sovereigns and nearly all the big banks almost certainly collapsing. What it leaves us with is a string of countries without debts and its citizens without a horrendous debt burden. It will open up huge gaps in the financial markets for new smaller operators who are not too big to save and moral hazard will be restored. Trying to maintain the status quo is what is destroying the EU banks and the EU itself.