The ECB Sticks To Its Playbook …

… and markets unwind [1] (click for better viewing)

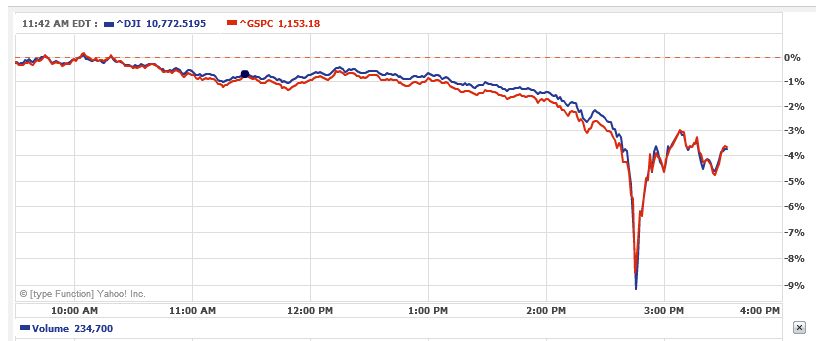

It thus appears that those hoping that that the market turmoil would be confined to Europe were proven wrong today as global stocks entered a veritable rout most likely triggered by the lack of any sort of meaningful action by part of the ECB.

Global stocks extended the biggest three-day drop in more than a year, the euro sank to the lowest since March 2009 and Greek, Spanish and Italian bond yields surged on concern European leaders aren’t doing enough to halt the region’s debt crisis. Oil slid, while Treasuries rallied.

The MSCI World Index lost 2.8 percent at 2:22 p.m. in New York to extend its three-day plunge to 5.9 percent, the biggest since March 2009. The Standard & Poor’s 500 Index dropped 3.1 percent to a two-month low and is down 6 percent over the past three days. The euro sank to as low as $1.2613 as 10-year bond yields soared at least 0.22 percentage points in Spain and Italy and investors demanded 1.63 percentage points to own the Spanish debt instead of benchmark German bunds, the most in 13 years. Greece’s two-year note yield topped 16 percent, a record. The 10-year U.S. Treasury yield fell to 3.41 percent.

European Central Bank President Jean-Claude Trichet held interest rates steady at a record low of 1 percent today and said it didn’t discuss whether to purchase government bonds to stem the region’s debt crisis, defying market speculation that it would take such measures. The euro maintained losses even as Greece’s parliament approved austerity measures demanded by the European Union and International Monetary Fund as a condition of its 110 billion ($140 billion) bailout.

“The ECB can fix this instantly by doing what the Fed has done — instantly providing liquidity by buying bad fixed-income instruments and paying cash in U.S. dollars,” said David Kovacs, head of quantitative strategies at Turner Investment Partners in Berwyn, Pennsylvania, which manages $18 billion. “The reason the market is horrified now is Trichet said it’s not even being discussed. Smart investors are basically selling risk assets.”

Please note that I am not saying that the ECB has to start buying government bonds now, but clearly the helping hand it extended earlier this by scrapping the collateral rules for Greek sovereigns (and thus in effect other distressed EMU sovereigns as well) was not deemed enough and as markets today were warming up to some form of concession by the ECB that they would have to scrap that old playbook of theirs entirely, they did … well just the opposite.

As a result everything risky took a solid beating with global equities plunging around the globe (well Canada may be the exception c.f Alphaville, but still …). Also in FX land the action heated up. In this way, the EUR/USD is currently trading below 1.26 (and counting) and other traditional risk/carry trade plays have been taken to the dump. One notable example here is the AUD/USD which has moved from 0.92-0.93ish to 0.88ish in only one week and another is the EUR/JPY fiddling with 113 at the moment which is truly astonishing. Today, BNP Paribas released the ominous call that the Euro will be trading on par with the Greenback in Q1-2011 to which my response is simply; that late!

So, where do we go from here? Well, the theatricals on Wall Street and elsewhere are of course just that, but as the we are about to close the book on a week where the debt crisis brought its first real human casualties the stakes are being upped not least in the context of European policy makers where today’s message that … (quote: Tullet Prebon’s Lena Komileva)

… The ECB went for a “safe haven” approach focused on defending its independence, its inflation-fighting credibility and the euro as a store of value.

Well, it just won’t cut it and at this point it really does not matter whether you are a deflationist or an inflationist or whether you believe the Greek people (or perhaps those in Spain or Portugal) should burn in hell for their irresponsibility. The stakes have been raised and while I believe a Greek debt restructuring/default has been inevitable all along it now carries the risk of leading to a new and altogether more sinister batch of "inevitable outcomes"; it is called contagion and we are right in the middle of it. You better have that playbook ready!

—

[1] – Although this suggest something else may be brewing.

————–

This was a post by Claus Vistesen, who also blogs at his own site Alpha.Sources.

If the ECB buys the greek bonds there is no need for a bailout by the member states. But the ECB does not have the same powers as the FED. The FED can make any amount of losses it wishes and the american public has to finance it. There is no such mechanism in the EU (maybe luckily for the taxpayers).