As you may know, I now use the sectoral balances approach very heavily in looking at economic forecasting. The crux of the sectoral balances is that, from an accounting perspective, every sector’s deficit must be offset by an equal surplus in another sector of the economy. I think it is a very valued-added way of breaking down an economy because it allows one to aggregate different sectors of an economy at a level that makes sense given broad cyclical movements and to discern how those movements will impact not just one sector but other sectors of the economy as well. British economist Wynne Godley is the one who most effectively put this approach to practice and a recent interview with Jan Hatzius of Goldman Sachs highlights this fact.

At the very base level, the most useful sectoral disaggregation is the one that divides an economy into three parts: government, trade and private domestic sectors. I like to further divide the private domestic sector into non-financial business, financial and household in order to isolate these sectors and their macro impact. But the basic three sector approach in and of itself is very useful. Hatzius spoke to Business Insider recently, talking about what he’s seeing using this approach. I want to break down his analysis and make some comments.

Hatzius comment #1:

…every dollar of government deficits has to be offset with private sector surpluses purely from an accounting standpoint, because one sector’s income is another sector’s spending, so it all has to add up to zero. That’s the starting point. It’s a truism, basically. Where it goes from being a truism and an accounting identity to an economic relationship is once you recognize that cyclical impulses to the economy depend on desired changes in these sector’s financial balances.

What Hatzius is saying here is that the the accounting tautology that forces one sector’s net spending to equal another’s net income is actually important because it allows one to understand “cyclical impulses” that arise within one sector. The key here is that one needs to disaggregate economic sectors of the economy at a level that is significant enough to show economic impulses that act similarly across most all agents within that sector. The point is to identify sectors of the economy whose individual economic agents will largely be moving in concert with each other in a discernible way so that their aggregate impact creates a discernible net movement in that sector’s deficit or surplus from one period to another.

Put a bit more simply, it’s not enough to just carve up the economy into different groups. You need to be able to predict what those groups are going to do as an aggregate. And their sectoral balance has to move meaningfully for it to have any significance for the other groups of the economy.

Given this, Hatzius is bullish on the US economy. And here’s why:

If the business sector is basically trying to reduce its financial surplus at a more rapid pace than the government is trying to reduce its deficit then you’re getting a net positive impulse to spending which then translates into stronger, higher, more income, and ultimately feeds back into spending.

Since mid-2009, that surplus has gradually come down as businesses and households have gotten closer to where they need to be from a long-term balance sheet perspective. They’ve paid down debt, they’ve eliminated the excess supply of housing, and that’s basically allowed them to reduce the financial surpluses that they run. They’re still running large surpluses – still 5.5 to 7 percent of GDP, but they’re no longer as large. We expect those figures to come down as the balance sheet adjustment process makes further strides and that’s an underlying source of boost to the economy that’s happening on the one side.

Hatzius is saying that the domestic private sector will meaningfully reduce its net surplus in the second half of 2013 because the deleveraging process will abate cyclically. And that, he says, will translate into a big reduction in government deficits and into a large uptick in GDP growth. The one word of caution Hatzius offers to this whole affair concerns the fiscal cliff where he says the economy would contract violently if we don’t have an operational deal by February. As you know, I agree. There’s a lot more from Hatzius at Business Insider.

Here’s where I see this.

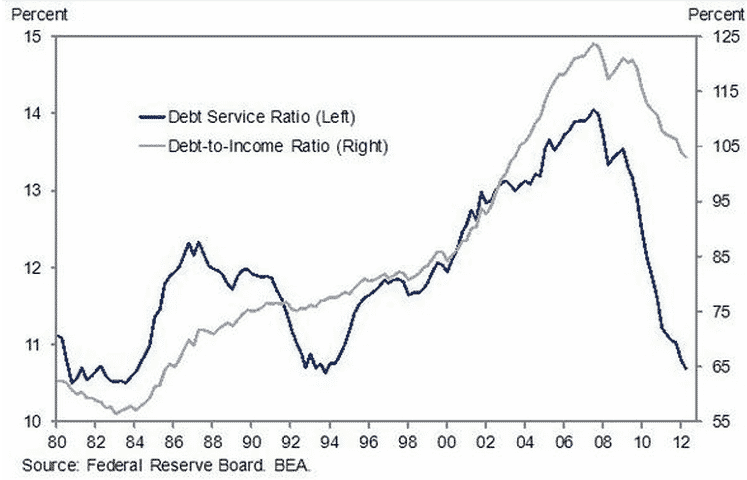

I agree with Hatzius’ macro points that a releveraging is bullish for cyclical growth and will reduce US government deficits. I also agree that the fiscal cliff will short-circuit all of this and cause a nasty double dip. However, where I disagree is at the sub-sectoral level, on households and businesses. Let’s look at households first. Look at US household debt-to-income versus debt servicing cost ratios. I did a chart on this in October.

{kind=link}

And what you see in the chart is a doubling of the household debt level from the end of the last secular bear market due n great part to the reduction of interest rates from the historically high levels that prevailed in the early 1980s. What this meant during the 1980s and 1990s was a fairly benign debt service cost situation even as debt levels in households increased dramatically. It was only after the end of the technology bubble and the Fed’s subsequent policy accommodation, when it held the Fed Funds rate at 1% from 2003 to 2004 that debt service costs began to spiral upwards with the debt levels. And in both cases, the move upwards was parabolic as the housing bubble facilitated ever greater increases in household debt by giving debtors tangible equity against which to support the rise.

Now, the Fed Funds rate is zero percent. Household debt has receeded from almost 125% of GDP to just over 100% of GDP. And debt service costs are the lowest in a generation. What Hatzius is saying is that, from a cyclical perspective, this should mean releveraging, especially 3 years into a cyclical recovery. I agree with this analysis. Here’s how I put it in March:

When it comes to the balance sheet recession and deleveraging, policy makers have abundant ways to forestall the inevitable reduction in debt ratios. Americans increased the savings rate during the downturn. However, the savings rate is not increasing. The average personal savings rate in the U.S. peaked in mid 2009 just as the recession ended. The data since do not suggest savings will continue upward until another economic downturn hits. Deleveraging may continue in small measure, but I continue to believe that this balance sheet recession will see the bulk of deleveraging as a result of economic downturns.

So don’t be surprised by consumer releveraging. It is the norm.

Nonetheless, I question how much releveraging will occur. I believe US household debt levels are still very high as the debt level is about 40% of GDP higher than they were 30 years ago. And given the still weak job growth in the US economy and the changed psychology of the housing market, I believe US households will be in a protracted balance sheet recession for a long while. The psychology therefore is not geared toward releveraging in the way that it was during cyclical upturns during the last 30-odd years. This spells weaker cyclical growth.

Moreover, I also question what the implications will be on a secular basis. As I have said time and again, the US economy does not have the policy space it once did because policy rates are at zero percent and deficits are still large. When the US next hits recession, there will be a combination of still high household debt levels, large fiscal deficits and low policy rates which will combine to produce a lower than normal fiscal expansion, a higher than normal deleveraging and zero monetary stimulus. To me, that is the important point here. When the US next goes into recession, the balance sheet recession will resume more aggressively because the underlying impetus for deleveraging by households is still extant.

Regarding the business sector, companies have already done the heavy lifting on deleveraging. And there are record profits in the private sector right now in the US. Debt is not a problem there. My analysis here says that government deficits are the biggest driver of elevated corporate margins. This means that to the degree that government has expanded its deficits, not because of the private sector’s desire to net save, but rather as stimulus to support growth, that stimulus has facilitated business sector profits over household sector income. So what I am saying here is that government is not just recording higher deficits simply in reaction to impulses coming from the business and household sectors. It has consciously been trying to spur aggregate demand by deficit spending. And this policy has not been effective in translating to higher net savings at the household level since savings rates there peaked over three years ago.

Unless businesses now start adding headcount and boosting capital spending then, the sectoral balances intersection here is going to be dictated by government and the deficit reduction mentality taking shape in Washington. As I wrote in October:

the macro event that we should be looking for is a net reduction in public sector deficits. Not only will this reduce GDP, it will also have an extremely negative effect on corporate margins and profitability in the US – just as deficit reduction in Europe has hurt U.S. multinationals already.

In sum, I believe directionally Hatzius is right. In the absence of the fiscal cliff, the US economy looks better than Europe and should continue to grow. However, I believe Hatzius underestimates the psychological impact of the balance sheet recession in restraining spending, especially in an environment of slow job and wage growth. I also believe Hatzius reverses the causality between the business sector and government in determining why US fiscal deficits are so large. I believe much of it is determined by the desire to increase aggregate demand and not by business sector deleveraging as business deleveraging has long since ended. In addition, I do believe we should expect some modest impact from the fiscal cliff at a minimum. Hatzius says this will be a drag on growth in the first half of 2013 but will not be a drag later in the year. That seems to be a reasonable guess. Most importantly, on a secular basis, the US is still in a balance sheet recession with limited policy space. And while the cyclical situation is better, the secular outlook is still problematic. Only a long and uninterrupted economic upturn accompanied by large fiscal deficits will change this subdued secular outlook in the absence of defaults, debt forgiveness or credit writedowns.