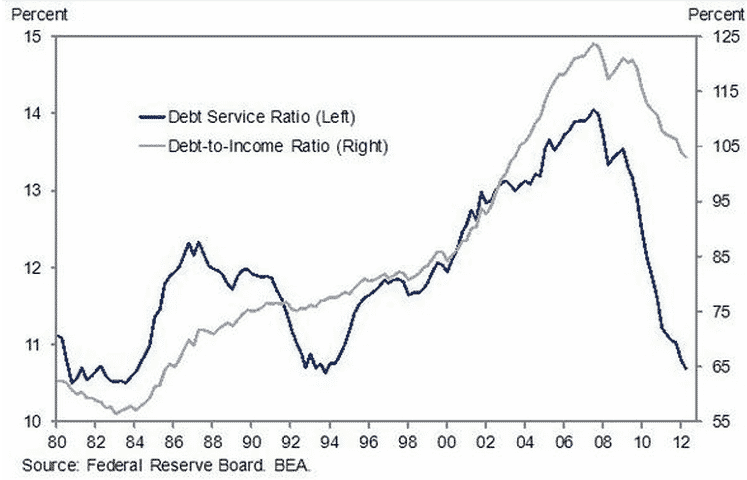

Here’s a great chart from Goldman Sachs that I spied as a result of a tweet by finance blogger Conor Sen who is someone to follow on Twitter. It shows the divergence in US household debt-to-income ratios and debt servicing costs as interest rates have declined. In my view this divergence has significant implications.

{kind=link}

This is a big issue for me because it highlights my beef with mainstream policy frameworks and their lack of regard for debt and credit aggregates or financial system fragility. Andrew Haldane of the Bank of England voiced disquiet about this recently.

Cycles in money and bank credit are familiar from centuries past. And yet, for perhaps a generation, the symptoms of this old virus were left untreated. That neglect allowed the infection to spread from the financial system to the real economy, with near-fatal consequences for both.

In many ways, this was an odd disease to have contracted. The symptoms should have been all too obvious from history. The interplay of bank money and credit and the wider economy has been pivotal to the mandate of central banks for centuries. For at least a century, that was recognised in the design of public policy frameworks. The management of bank money and credit was a clear public policy prerequisite for maintaining broader macroeconomic and social stability.

Two developments – one academic, one policy-related – appear to have been responsible for this surprising memory loss. The first was the emergence of micro-founded dynamic stochastic general equilibrium (DGSE) models in economics. Because these models were built on real-business-cycle foundations, financial factors (asset prices, money and credit) played distinctly second fiddle, if they played a role at all.

The second was an accompaying neglect for aggregate money and credit conditions in the construction of public policy frameworks. Inflation targeting assumed primacy as a monetary policy framework, with little role for commercial banks’ balance sheets as either an end or an intermediate objective. And regulation of financial firms was in many cases taken out of the hands of central banks and delegated to separate supervisory agencies with an institution-specific, non-monetary focus.

What Haldane is saying is that making policy choices for the real economy must take credit and debt levels into account, especially when thinking about the fragility of our financial system. This is exactly what William White and Stephen Roach have been saying in questioning central bank policy. White puts it this way:

From a Keynesian perspective, based essentially on a one period model of the determinants of aggregate demand, it seemed clearly appropriate to try to support the level of spending. After the recession of 2009, the economies of the AME’s seemed to be operating well below potential, and inflationary pressures remained subdued. Indeed, various authors used plausible versions of the Taylor rule to assert that the real policy rate required to reestablish a full employment equilibrium (and prevent deflation) was significantly negative. Such findings were used to justify the use of non standard monetary measures when nominal policy rates hit the ZLB.

There is, however, an alternative perspective that focuses on how such policies can also lead to unintended consequences over longer time periods. This strand of thought also goes back to the pre War period, when many business cycle theorists focused on the cumulative effects of bank‐created‐credit on the supply side of the economy. In particular, the Austrian school of thought, spearheaded by von Mises and Hayek, warned that credit driven expansions would eventually lead to a costly misallocation of real resources (“malinvestments”) that would end in crisis. Based on his experience during the Japanese crisis of the 1990’s, Koo (2003) pointed out that an overhang of corporate investment and corporate debt could also lead to the same result (a “balance sheet recession”).

The disease is a protracted balance-sheet recession that has turned a generation of America’s consumers into zombies – the economic walking dead. Think Japan, and its corporate zombies of the 1990’s. Just as they wrote the script for the first of Japan’s lost decades, their counterparts are now doing the same for the US economy.

Two bubbles – property and credit – enabled a decade of excessive consumption. Since their collapse in 2007, US households have understandably become fixated on repairing the damage. That means paying down debt and rebuilding savings, leaving consumer demand mired in protracted weakness.

Yet the treatment prescribed for this malady has compounded the problem. Steeped in denial, the Federal Reserve is treating the disease as a cyclical problem – deploying the full force of monetary accommodation to compensate for what it believes to be a temporary shortfall in aggregate demand.

The convoluted logic behind this strategy is quite disturbing – not only for the US, but also for the global economy. There is nothing cyclical about the lasting aftershocks of a balance-sheet recession that have now been evident for nearly five years. Indeed, balance-sheet repair has barely begun for US households.

I have made this the central theme of this blog since its name, Credit Writedowns, is supposed to evoke a sense that bank and household balance sheets are the determining factor in this crisis. But my sense here is that policy makers are still steeped in denial, in large part because of the efficacy of their efforts in creating a cyclical rebound, as the economy has responded to low interest rates. This is illustrated in the chart by the steep decline in debt service ratios. And note, I called this rebound fairly early and received a lot of flak for it, so I do recognise the policy successes here. What mainstream economists and policy makers see when they look at the Goldman chart is that cyclical falloff in debt service ratios. This focus uniquely on debt service costs with no regard to debt to income or debt to GDP levels – what I call “The debt servicing cost mentality” – is extremely dangerous. What I see – and what Roach seems to be pointing to – is the less steep falloff in debt to income ratios. And this makes sense because policy rates are at or near zero percent, meaning that the next recession will not witness such a large divergence in debt service cost and debt-to-incme ratios. For debt service ratios to recede in the next downturn, debt to income ratios must be reduced at the same rate, whether through lower debt from default and debt forgiveness or increased income. Likely, default will play the overwhelming role, at least initially.

As I outlined over two years ago, the origins of the next crisis are the simultaneous attempt for the public and private sector to deleverage simultaneously across a broad swathe of large industrialised countries. What we should anticipate – and what we have already seen in the euro zone – is failure and debt deflation because you must have massive defaults and debt forgiveness to effect simultaneous deleveraging in the public and private spheres. If and when the United States joins the party, that’s when the full ramifications of our policies will become evident.