On Christmas Eve, the Wall Street Journal had two interesting articles on the credit situation in the U.S., one from the banks’ perspective and one from the households’ perspective. In general, the data were positive but I believe the analysis was incomplete because it fails to consider net interest margins, which are coming down.

The first analysis was about the Fed and its provision of cheap money to banks. This cheap money has not translated into a huge surge in credit. Rather, according to the Wall Street Journal, it has increased bank margins.

Since the Fed began buying mortgage-backed securities to lower interest rates four years ago, rates on 30-year fixed-rate mortgages have fallen nearly three percentage points and averaged 3.37% last week, according to Freddie Mac .

While current rates are the lowest in generations, some economists argue that they should be even lower—perhaps 2.8% based on the historical relationship between mortgage rates and yields on mortgage-backed securities. The economists posit that banks are keeping the rates artificially high, boosting profits and depriving the economy of the full benefit of the Federal Reserve’s efforts.

[…]

Lenders profit on the gap, or spread, between their cost of obtaining money and the rate they charge when lending it out. Before the financial crisis, this spread averaged around 0.5 percentage point and widened to about 1 percentage point in the years after 2008. In October, after the Fed embarked on a new round of mortgage bond purchases, the spread leapt to 1.6 points and currently is hovering around 1.3 points.

The Journal provides the following graph to make their point.

{kind=link}

I see this analysis as intrinsically flawed. What they have measured in their graph is the profit from financial repression. They are measuring the difference between the money investors get from the mortgages underlying mortgage backed securities and the money banks would get from those securities now that the Fed is artificially suppressing mortgage rates.

Banks don’t look at their mortgage book in isolation. Rather they look to maximize their entire funding spread, which is measured via net interest margins. And these are coming down, not going up. Even the FDIC quarterly banking profile tells us this.

{kind=link}

So this particular Wall Street Journal post gets it wrong. What has really happened is that interest rates have come down even while bank funding costs have not. And so net interest margins are contracting. This is why banks are not ‘passing on the profit’ from cheap money.

Moreover, banks are profiting from a decline in charge-offs and in loan loss provisions along with increased non-lending income. They are not actually making more money from mortgage lending because the lending has become more profitable. As the FDIC put it in its quarterly banking profile:

For the ninth quarter in a row, net charge-offs (NCOs) were lower than a year earlier. Banks charged off $22.3 billion (net) during the quarter, $4.4 billion (16.5 percent) less than in third quarter 2011. The largest NCO declines occurred in credit cards (down $2.8 billion, or 30.4 percent), and in real estate construction loans (down $1.4 billion, or 61 percent). Charge-offs declined in all major loan categories except 1-4 family residential real estate loans, where NCOs were $1.3 billion (15.5 percent) higher than a year earlier. This increase was the result of new accounting and reporting guidelines applicable to national banks and federal savings associations concerning the reporting of restructured loans

[…]

Insured institutions reduced their reserves for loan losses by $9.6 billion (5.4 percent) during the quarter, as net charge-offs of $22.3 billion exceeded loss provisions of $14.8 billion. This is the tenth consecutive quarter that the industry’s reserves have declined. Much of the total reduction in reserves was concentrated among larger institutions. The ten largest banks together reduced their reserves by $7.3 billion (8.1 percent) during the quarter. Overall, a majority of institutions (53.5 percent) added to their reserves during the quarter. The combination of sizable reserve reductions with smaller reductions in noncurrent loan balances meant that the industry’s “coverage ratio” of reserves to noncurrent loans declined from 60.4 percent to 57.2 percent during the quarter. More than half of all institutions (53.4 percent) increased their coverage ratios, but their increases were outweighed by larger declines at many of the biggest banks.

My conclusion here is that banks are not passing on profits because these profits are fictional, the result of accounting gains that are probably not sustainable. When the cycle turns down, I would expect us to see that banks had under-provisioned for loan losses.

The second article is on the decline in credit costs for households.

U.S. households spent 10.6% of their after-tax income on debt payments in the third quarter of the year, the lowest level since 1983, according to recently released Federal Reserve data. Add in other required payments that aren’t classified as debt—such as rent and auto leases—and the figure rises to 15.7%, also near a 30-year low.

Debt payments are being pushed down by a variety of factors. After borrowing heavily during the housing boom, many families have devoted much of the past five years to working off debts and rebuilding savings. Not all such deleveraging has been voluntary. Foreclosures and bankruptcies have played a major role in reducing household debt, while tighter lending standards have made fresh borrowing difficult for many people.

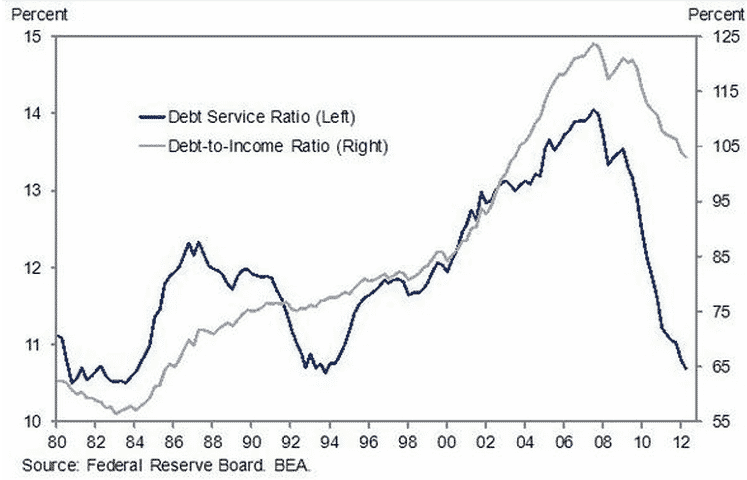

Here’s the thing. There has been a huge separation between debt service costs and debt to GDP levels for households in the US. Look at this chart.

{kind=link}

That tells me that the historic drop in debt service costs is the result of low rates. And given the still high debt to GDP levels, it also means that any increase in household debt interest rates would be a killer for the US economy. The use of easy money to restore household balance sheets has been successful so far. The problem, however, is that as soon as the business cycle turns, spreads will widen and household debt interest rates will increase, particularly for mortgages, which are the household sector’s biggest credit liability.

So again, don’t be fooled by the happy talk here. The situation is much more balanced than the article suggests. What we see here is a bank sector buoyed by low charge-offs and provisioning that is still worried enough about its balance sheets that it has not turned on the credit spigot the way the Fed has done for them. Meanwhile, the household sector has record low debt service costs due to the Fed’s efforts. And that has helped and will continue to help a struggling economy. The question is how long can this go on. And what happens when the music stops? Will households have deleveraged enough? I say no. And so I worry about the next recession more than I rejoice over the improved peak of the cycle metrics.