Bond markets are often seen as more prescient in anticipating economic slowdowns than stock markets. Yield curve inversion has predicted every recession in the US since 1970, for example. Inverted yield curves are a leading indicator of recession because they are signs of expectations that the economy will be so negatively impacted that it will force the central bank to ease rates in the future.

During the last recession, economists like Federal Reserve Chairman Bernanke speculated that signs of yield curve flattening and inversion were not prescient because of an alleged "global saving glut".

I would not interpret the currently very flat yield curve as indicating a significant economic slowdown to come…

An alternative perspective holds that the recent behavior of interest rates does not presage an economic slowdown but suggests instead that the level of real interest rates consistent with full employment in the long run–the natural interest rate, if you will–has declined.

Given the global nature of the decline in yields, an explanation less centered on the United States might be required. About a year ago, I offered the thesis that a "global saving glut"–an excess, at historically normal real interest rates, of desired global saving over desired global investment–was contributing to the decline in interest rates.

–Ben Bernanke: Reflections on the Yield Curve and Monetary Policy (Before the Economic Club of New York, New York, New York, March 20, 2006)

This perspective proved false when recession did come late in 2007.

Bloomberg is running a story that indicates this same inverted curve harbinger may be at play again:

The so-called Treasury yield curve, adjusted for distortions caused by the Federal Reserve’s record low zero to 0.25 percent target interest rate for overnight loans between banks, shows that two-year notes yield 20 basis points, or 0.20 percentage point, less than five-year notes, according to Bank of America Corp. research. The unadjusted gap of 79 basis points at the end of last week indicates the chance of recession at about 15 percent.

I am a bit sceptical of this ‘adjusted’ curve talk. Nevertheless, the data have been weakening.

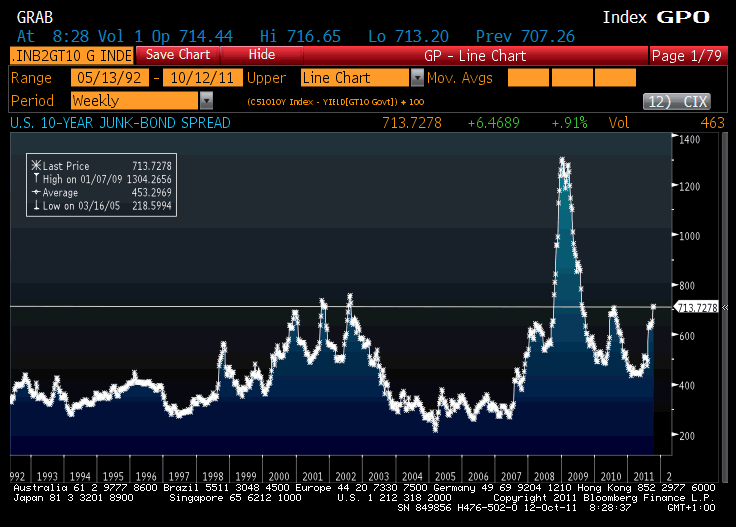

What about high yield. An increased spread between high yield and government bonds is often seen as a harbinger of economic downturn as well. As the economy rolls over, more marginal debtors feel stress first and this gets reflected in bond yields. Bond funds reduce risk and the spread between safer bonds and high yield bonds increases.

The extra yield investors demand to own bonds from investment-grade companies worldwide reached 277 basis points, or 2.77 percentage points, on Oct. 5, the widest since July 2009, before declining to 275 yesterday, according to Bank of America Merrill Lynch index data. Spreads on high-yield, high- risk debt globally in the U.S. reached 932 basis points on Oct. 4, the highest since September 2009, before narrowing to 897.

Here’s the chart courtesy of Andy Lees.

{kind=link}

What do you see? Not everyone thinks this is telling us things will get worse. Some see value. Bloomberg again:

“We are beginning to look at high yield again,” Andrew Sutherland, head of credit at Standard Life, said in an interview at the company’s office in the Scottish capital. “If markets turn around, that sector could snap in very quickly. We wouldn’t want to miss it, but are pacing ourselves very gradually. High yield still looks attractive.”

I see this as a macro call. High yield is attractive if you think that the economy will rebound. if not, the extremely low high yield default rate will rise considerably, as will yields.