As we await the US jobs data, it bears remembering that oil is a big wildcard both on in terms of consumption and investment. Right now, oil is plunging, down as much as $14 a barrel for the Brent variant and $17 a barrel for WTI since mid-April. The question is whether the rout continues.

I think it does and here’s why.

Go back to March, when I wrote the last flurry of oil-related posts. That was when we saw the first post-OPEC agreement downdraft. Oil prices recovered in April but to a slightly lower level, before cliff diving again.

{kind=link}

Source: Business Insider

So there’s a tension here. Saudi Arabia is supposed to be the world’s swing producer and they have finally acceded to output cuts to stabilize oil prices, getting Russia onboard too. But, at today’s prices, a lot of North American shale production is viable and these guys are swamping the market, with rig counts up every week.

{kind=link}

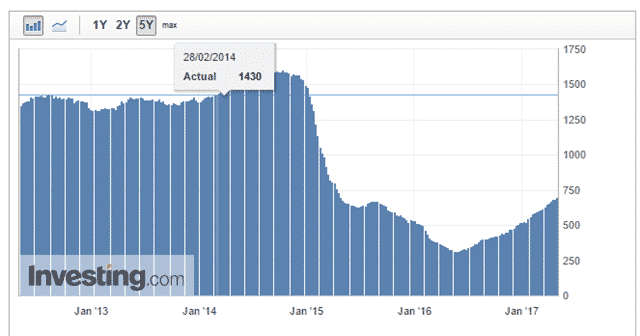

Now, if you look at the North American rig count numbers in a multi-year context things, we are nowhere near the highs of 2014.

{kind=link}

But back in March, I was calling the rig count a bubble. And the longest term view makes clear why.

{kind=link}

So, while one could legitimately call the increase in rig count and the switch of oil majors to shale oil investment an echo bubble, the size of the uptick is nowhere near what we saw before. And given where oil prices are coming from – $50 a barrel, there is no support for the kind of capex we saw when oil traded above $100 a barrel.

Why this matters. Oil prices are not going up dramatically. Shale oil has become the swing producer, and these shale projects are viable at these levels, ensuring a supply glut which will keep prices under pressure. But the downdraft in capex from any collapse in prices is likely to be more muted and have less impact on the economy. At the same time, with global growth re-accelerating, the fall in prices could be a windfall for consumers, especially in developed economies where workers’ real earnings is still recovering.

On net, I believe the scenario is negative for global growth, if marginally so. The risk is in credit, particularly regarding knock-on effects for emerging markets, commodity credits and high yield more generally.

The Fed is only likely to pause if we get a panic situation that drags oil back down to $30 a barrel. But, while the Fed is on course for three or four rate hikes this year because of a tightening bias, oil in the $40 range will get the Fed’s attention because of the capex and consumption implications.

Bottom line: oil prices will continue to be under pressure as long as rig counts are rising. We will see a yo-yoing of prices, but the calls for $60 or $70 a barrel look misplaced. Analysts still expect WTI to average $55 for the whole of 2017; these forecasts will be under pressure. Yield curve flattening and pressure on emerging market and high yield credits are the biggest risks.