A couple of weeks ago I told you about two properties in London that I was familiar with as background for my post on house price inflation in the UK. What was clear from those two examples and dozens of others I found is that rental yields are extremely low in London, such that rents do not cover mortgage costs at 80 or 90% LTV. And house price appreciation in Central London is well out of line with both income and inflation trends. There is something going on in London that is causing people to ‘consume’ housing at inflated prices.

Given the last post here, a guest post on house price inflation from 1870 that I found interesting, I thought it would be useful to show you the amortization calculations for an 80% LTV house at varying rates of interest. What the analysis will show is that at low rates of interest, the affordability of housing changes dramatically, making residential property very sensitive to interest rate changes.

Here’s the example. Say you are looking to buy a 3-bedroom house for 300,000. And the comparison you have to that price is a rental unit that is 1,200. The way I would compare the buy to rent calculation in the US would be to make property tax and mortgage interest tax deductions a wash, leaving you with interest payments as equivalent to rent with the principal as a forced savings you could replicate as a renter. So from a buy vs. rent comparison, you are basically looking at the interest payment against the rental payment as the big comparison.

This is a bit simplified, especially for countries where mortgage interest is not tax deductible but it will help to discern the impact of interest rates on resource allocation to or away from the property sector.

In the last two decades or so a 5-year variable rate mortgage might have yielded 6% so that the initial interest payment would be 1200, exactly the amount you would pay in rent for the equivalent accommodation. In the scenario I am setting up then, rent vs. buy is a wash from a cash flow perspective in the initial month of the buy vs. rent calculation. And since this is the basis on which mortgages are made, you could say residential housing is correctly valued here. The forced savings principal is 238.92 to bring the total payment to 1438.92.

{kind=link}

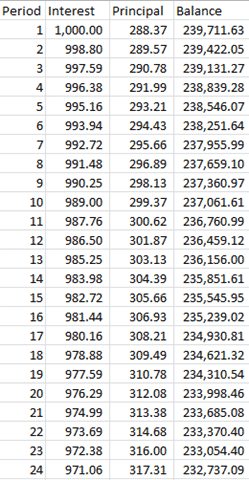

If we drop the interest rate to 5%, three things occur that shift resource allocation to residential property. First, the overall monthly payment declines. Now you pay just 1288.37 total. So the house is now much more affordable, even though interest rates only declined 1%. Second, the nominal amount of your mortgage payment that is principal is much higher now even though the monthly payment is lower. That’s a big incentive to buy because it means that with a lower interest rate, from day one you are reducing your principal much faster while paying less. And third, the proportion of interest and principal changes fairly aggressively as only 1000 is interest now and the forced savings principal is bigger at 288.37. Instead of a 5 to 1 ratio of interest to principal, you begin with a 3.5 to 1 ratio. And remember this is after only a 1% reduction in rates from 6 to 5%.

{kind=link}

{kind=link}

Finally, with rates at 3%, for a 5-year variable rate mortgage, where they are right now in the U.S., the contrast to the 6% rate is stark. Interest expense has been cut in half to 600. Principal is now 411.85 right at the start, which gives it just better than a 1.5 to 1 ratio, compared to a 5 to 1 ratio at 6%. And the total payment is 1011.85, 15% less than the equivalent rental

{kind=link}

When central banks keep interest rates lower for longer, at effectively zero percent as they have recently, they are skewing resource allocation toward longer lived assets like housing for exactly the same reasons we see in the mortgage amortization schedules. The real value of distant cash flows increases dramatically at low rates of interest due to the proportional drop being larger.

Conversely, if rates rise from a low base, it crushes those loaded up on debt because the interest expense is much larger. Imagine you have household income of 60,000 and are buying a house at 80% LTV for 300,000. In one scenario you are paying 1011.85 per month, but in another scenario you pay 1438.92 per month, 40% more. That’s the kind of interest increase that can lead to a default. And while a 30-year fixed rate mortgage eliminates this risk for homeowners, the value of the house is reduced by the same factor given the decline in affordability.

In my view, a country like the UK, the US, Ireland, Spain, Sweden, Denmark, or the Netherlands where household debt levels are still elevated, there is very little room for interest rate policy normalization because of the factors outlined in this analysis. Unless wage growth allows for greater household breathing space, a sharp rise in rates would be crushing to households.

Central banks know that low rates are an inevitability for years if not decades because of the fragility of household balance sheets in an environment of stagnant wages. You can see then how a Japanese outcome becomes more likely as a result because, with rates at zero or very low when recessions hit, policy accommodation is not sufficiently robust to have a large cyclical impact. And so deflation and secular stagnation take hold. This is where the US and Europe are headed right now.