Originally posted on Vox

By Luigi Buttiglione, Philip Lane, Lucrezia Reichlin, Vincent Reinhart

The world has not yet begun to deleverage its crisis-linked borrowing. Global debt-to-GDP is breaking new highs in ways that hinder recovery in mature economies and threaten new crisis in emerging nations – especially China. This column introduces the latest Geneva Report on the World Economy. It argues that the policy path to less volatile debt dynamics is a narrow one, and it is already clear that developed economies must expect prolonged low growth or another crisis along the way.

The Lehman Brothers bankruptcy tipped the world into its worst economic crisis since the Great Depression. The recovery has been slow and weak – even in those economies such as the US that emerged first from the acute phase of the Global Crisis. Emerging markets did better during the Crisis, but have recently slowed down. Some, such as China, are seeing marked increases in leverage that raise the odds that they will experience home-grown crises in the future.

To understand the length and depth of the Crisis – as well as the weak recovery – it is essential to analyse the role of debt dynamics.1 In the 16th Geneva Report on the World Economy, we conduct a deep dive into the details of global debt dynamics over the past decade. This includes consistent comparisons across regions and sectors and an emphasis on the interaction of debt and income. We provide a multi-dimensional perspective on leverage for both advanced and emerging economies. Our comprehensive approach includes both public and private debt, with the latter broken down on sectoral lines (households, non-financial corporates, financial sector). Moreover, we take into account national adding-up constraints by relating sectoral debt levels to the overall international investment position.

What deleveraging?

Contrary to widely held beliefs, the world has not yet begun to delever. Global debt-to-GDP is still growing, breaking new highs. Figure 1 shows the evolution of total debt (excluding the financial sector) for our global sample (advanced economies plus major emerging market economies). While there was a pause during 2008-09, the rise of the global debt-GDP ratio recommenced in 2010-2011. Data in the report also show that debt-type external financing (leverage) continues to dominate equity-type financing (stock market capitalisation).

Figure 1. Global debt-to-GDP ratio, 2001-13

{kind=link}

As Figure 2 shows, global debt accumulation was:

- Led by developed economies until 2008; but

- Has been led by emerging economies since 2008; the sharp rise in Chinese debt is especially striking.

These emerging markets as a group are an important source of concern in terms of future debt trajectories. China and the so-called ‘fragile eight’ could find themselves in the unwanted role of ‘host’ to the next phase of the global leverage crisis.

Figure 2. Debt dynamics for a selection of advanced and emerging economies

{kind=link}

Note: DM = developed markets, EMU = Eurozone; EM = Emerging Markets.

While the emerging markets may be the Global Crisis’s future, its legacy continues to have severe consequences in the developed economies. This is especially true for Eurozone peripheral countries, which are vulnerable due to the complexity of their crisis and the inadequacies of the mix and sequence of policy responses. To date, the US and the UK have done a good job of managing the trade-off between deleveraging policies and output costs. They did this by avoiding credit crunches while still achieving meaningful debt reductions in their private sectors and their financial systems.

This result, however, was achieved at the cost of a substantial re-leveraging of the public sector – including their central banks. As a consequence, deleveraging the central banks will be a primary policy challenge for the foreseeable future.

Evolution of debt-carrying capacity

While debt levels are rising, the world is seeing a poisonous combination of growth and inflation rates that are lower than expected – in part due to the Global Crisis. Deleveraging and slower nominal growth are in many cases interacting in a vicious loop, with the latter making the deleveraging process harder and the former exacerbating the economic slowdown.

Debt capacity in the years to come will depend on future dynamics of output growth, inflation and the real interest rates. Potential output growth in developed economies has been on a declining path since the 1980s.

- We argue that the crisis has caused a further, permanent decline in both the level and growth rate of developed economies’ output.

- The underlying output growth in emerging markets – most prominently China – has also been slowing since 2008.

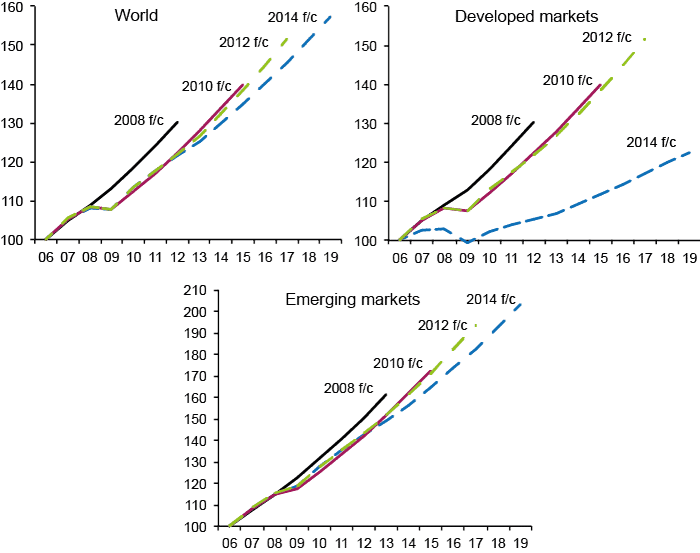

As evidence of this, Figure 3 shows the slowdown in growth forecasts for both advanced and emerging economies, as captured by the progressive reduction in output projections in the different vintages of the IMF’s World Economic Outlook since 2008.

Figure 3.

{kind=link}

The equilibrium real interest rate – that is, the interest rate compatible with full employment – is also poised to stay at historical low levels. Debt capacity will be under pressure if the actual real interest rate settles above its equilibrium level. This is likely to be the case in jurisdictions subject to the combined pressure of declining inflation and the zero lower bound constraint. Additional concerns come from possible increases in risk premia in those countries with a high level of legacy debt.

The danger of early rate rises

In such a context, and with still very high leverage, allowing the real rate to rise above its natural level would risk killing the recovery. Beyond pushing the economy into a prolonged period of stagnation, this would also put at risk the deleveraging process which is already very challenging.

Although there is a lot of uncertainty about such predictions, our call is for caution on interest rate rises. The case for caution in pre-emptively raising interest rates is reinforced by the weakness of inflationary pressures.

Moreover, the ECB should catch up with the other major central banks in an aggressive policy of quantitative easing.

- A forceful intervention with outright purchases of sovereign bonds – as well as private securities – is the correct tool for dealing with excessive downward pressure on inflation and fulfils the ECB mandate of price stability while helping the stabilization of the debt and easing credit conditions.

Further procrastination in implementing these by now urgent policy measures would risk, in the medium term, the resurgence of pressures on the sustainability of the Eurozone itself.

The broader challenges

The policy requirements for successful exit from a leverage trap are much broader than the appropriate conduct of monetary policy. The report addresses the fiscal challenges, the scope for macro-prudential policies and the restructuring of private-sector (bank, household, corporate) debt and sovereign debt.

The report also argues that – given the risks and costs associated with excessive leverage – more needs to be done to improve the resilience of macro-financial frameworks to debt shocks and to discourage excessive debt accumulation. Finally, we advocate enhanced international policy cooperation in addressing excessive global leverage.

References

Buttiglione L, P Lane, L Reichlin and V Reinhart (2014), Deleveraging, What Deleveraging? The 16th Geneva Report on the World Economy, CEPR Press, September.

Bank for International Settlements (2014), 84th Annual Report.

Bank for International Settlements 2014 Annual Conference

Borio C, R N McCauley and P McGuire (2011), “Global Credit and Domestic Credit Booms”, BIS Quarterly Review, September, pp. 43–57.

Jorda, O., M. Schularick and A. M. Taylor (2011), “Financial Crises, Credit Booms and External Imbalances,” IMF Economic Review 59(2), 340-378.

Lo, S. and K. S. Rogoff (2014), “Secular Stagnation, Debt Overhang and Other Rationales for Sluggish Growth, Six Years On”, BIS 2014 Annual Conference,

Mian, A and A Sufi (2014), House of Debt: How They (and You) Caused the Great Recession, and How We Can Prevent it from Happening Again, Chicago, IL: University of Chicago Press.

Obstfeld, M (2014), “Trilemmas and Tradeoffs: Living with Financial Globalization”, BIS 2014 Annual Conference,

Footnote

1 Over recent years, the Bank for International Settlements (BIS) has provided a wealth of analysis of global debt dynamics; see, for example, Borio et al (2011), the 2013-2014 BIS Annual Report and the papers presented at its 2014 Annual Conference. In particular, see Obstfeld (2014) and Lo and Rogoff (2014). On household debt, see Mian and Sufi (2014). On the relation between credit booms and financial crises, amongst many others, see Jorda et al. (2011).