By Sober Look

US residential rental costs continue to increase. Stories like the one below are echoed throughout the nation.

KARE 11/AP: – Lower-income renters say they are struggling with rapidly increasing rents in the Twin Cities area.

Dena Felper tells the St. Paul Pioneer Press her rent is expected to increase by 23 percent by March to $750 per month. She says she’ll have to take another job – her third – to pay for the increase.

The Minnesota Housing Partnership says Twin Cities residents are seeing some of the biggest rent increases in 12 years and the average rent in the area is nearing $1,000 per month.

Minnesota Housing Partnership Director Chip Halbach says about half of all Minnesota renters pay more than 30 percent of their income in rent.

The partnership says the foreclosure crisis created a flood of new renters, allowing landlords to be pickier and raise rents.

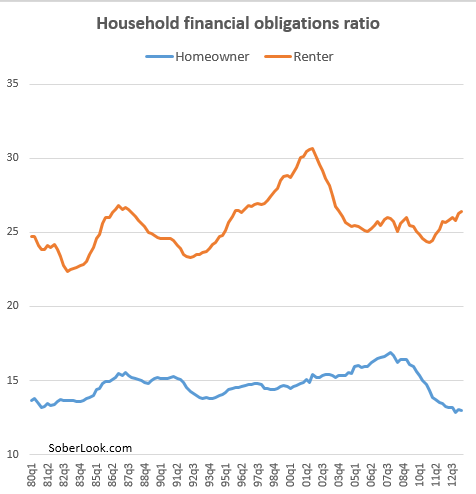

With wages stagnant (see post), the proportion of income going into rent is on the rise. The Fed recently released the latest data on the so-called “Financial Obligations Ratios” (FOR). For homeowners FOR represents required payments on mortgages, credit cards, auto loans, student loans, auto lease payments, homeowners’ insurance, and property tax payments – all as percentage of disposable income. For renters the mortgage payments and property tax payments are replaced with rental payments.

While homeowners have been able to reduce their monthly payments to the lowest level in decades via mortgage refinancing and cutting back on credit card usage, the FOR for renters has been on the rise.

| Source: FRB |

{kind=link}

It’s an unwelcome trend that shows a rising disparity between the lower income renters and the nation’s homeowners.

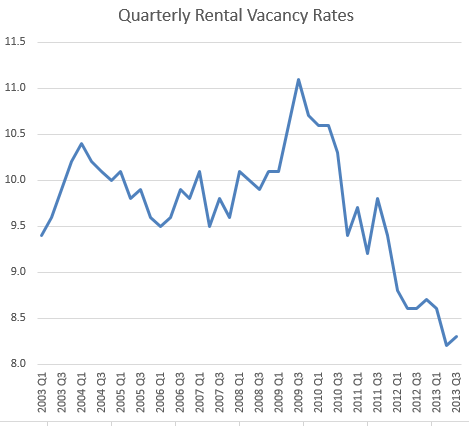

Update: Just to put this trend into perspective, the rental vacancy rate in the US is near the lowest level in over a decade, allowing landlords to raise rent.

{kind=link}