By Sober Look

India and Brazil are struggling to regain control of their currencies as both the rupee and the real touch new lows (all-time record for the rupee). It is remarkable how violent the corrections have been in just the past 3 months:

| Green = rupees per dollar; Blue = real per dollar |

{kind=link}

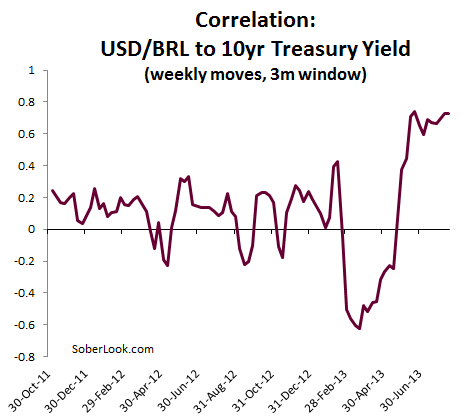

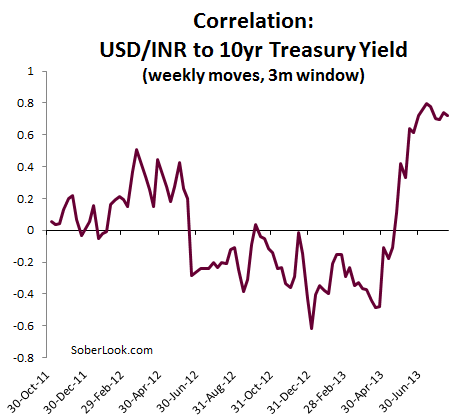

For those who don’t watch these currencies on a daily basis, these sell-offs seem to happen in spurts – almost at random. But there is a pattern here, particularly in the past few months. Investors are dumping these currencies during periods of higher expectations of the Fed’s slowing its securities purchase program. The evidence for the pattern is in the correlation between these exchange rates and the US treasury yields. Since Bernanke’s first comments on slowing the securities program, currency weakness consistently corresponds to higher US yields resulting from sharper taper expectations (see post).

{kind=link}

{kind=link}

The prospects of higher long-term interest rates resulting from the Fed’s taper is forcing investors out of emerging markets – and these two nations are feeling the brunt of this “rotation”. To be sure, we have no way of knowing if this would have still occurred if the Fed had not initiated QE3 a year ago. But the severity and the speed of these corrections would suggest that this is one of those unintended consequences of applying and then trying to exit an aggressive monetary stimulus program within highly interconnected capital markets, operating in a global economy. This has not been a part of the FOMC’s forecast…