By Edward Hugh

This post first appeared on my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.

This week we got what seemed to be some good news in the ongoing Euro debt crisis. Bond spreads in many of the countries on Europe’s periphery tightened vis-their German equivalents. Unfortunately we also got some bad news to go with it (no silver lining these days without the accompanying black cloud it seems): the tighter spreads were the result of a weakening of German bunds (or a rise in their yields) following what many considered to be a failed bond auction.

{kind=link}

What is becoming clearer to almost everyone is that this is now no longer simply a Euro periphery sovereign debt crisis. It has become a full blown crisis of confidence in the Euro itself.

{kind=link}

But just in case anyone was in any doubt, this week Deutsche Bank Chief Economist Thomas Mayer said as much on Bloomberg TV. Naturally he is far from the first to make this point – Commission President José Barroso and European Council President Herman Von Rompuy have been stressing the point for some time now – but it is an interesting reflection of how widely this opinion is now spreading.

{kind=link}

One of the reasons for the recent rise in tone and in the level of concern is that it is clear contagion is now spreading far from the periphery. Belgium and French bonds have come under increasing pressure. And, of course, that famous German bond auction seems to suggest that even German yields are not immune to contamination. Actually, one unsuccessful German bond auction doesn’t make a season of them, and Germany is well able to finance itself, but obviously markets are now drawing the conclusion that if Germany isn’t willing or able to cut loose from the sinking economies on the periphery, then the German economy will eventually be dragged down with them, which means that German bunds are no longer seen as a surrogate Deutsche Mark, but rather as the backstop for all the unfunded periphery losses which might show up on the EU desk.

The frontier between core and periphery is becoming increasingly blurred, with Belgian borrowing costs hitting a Euro era high of 5.8% last Friday.

{kind=link}

Of course, this weekend there has been a huge rush to agree a budget and put together a government, but after seven months of dawdling as if the large sovereign debt the country is labouring under wasn’t a problem all these last minute efforts somehow fail to convince. Really it is the whole European model of nation states and national identities which lie behind the common currency that often lie at the heart of the problem. If countries like Belgium lack a national consensus, while others like Italy and Spain have minorities (who pay more than there numerical share) who are not really convinced they want to be in the country, then how can a fiscal union which would be based on some countries permanently paying (the so called transfer union) while others continually receive hope to hold itself together politically?

{kind=link}

Then the possibility of joint and several responsibilities between an ever diminishing number of “core” core countries is simply leading to impossible pressures on the sovereign debt of the countries concerned. We have seen the first jitters in the direction of German debt this week, but France is a much clearer example as the exposure of the French banking system to Italy (400 billion euros worth, including public and private sector debt, according to BIS data) is leading to impossible pressure accumulating over the French rating, something which makes activating the EFSF as initially intended look increasingly difficult.

{kind=link}

And contagion from the crisis is now heading East. Austria is worried about its triple A, and is imposing new restriction on CEE funding by Austrian Banks. Naturally, as Fitch suggest, this is likely to extend the credit crunch out to the East.

{kind=link}

{kind=link}

Hungary is the obvious “missing link” here.

{kind=link}

But Romania is evidently not far behind, and President Traian Basescu is definitely not amused.

{kind=link}

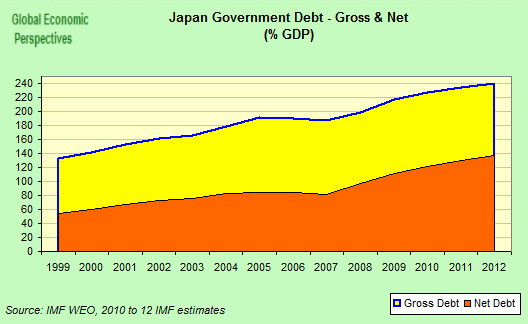

Of course the problem is not just a European one. Japan has a massive sovereign debt problem too.

{kind=link}

{kind=link}

In fact, far from having the “V shaped” recovery from the Tsunami some (not me) were predicting the short term outlook for the economy seems pretty dire. Policymakers in Japan still attempt to pin the problems down to confidence issues stemming from the Euro debt crisis and the high value of the yen, but surely what has been happening in Japan over the last 20 years has something more than local interest, since it was a harbinger of things to come elsewhere.

{kind=link}

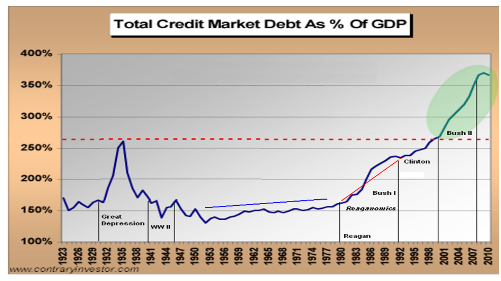

The Present Crisis Is Generalised One, Effectively Facing All Developed Economies

In the first place there is the problem of debt (whether public or private).

{kind=link}

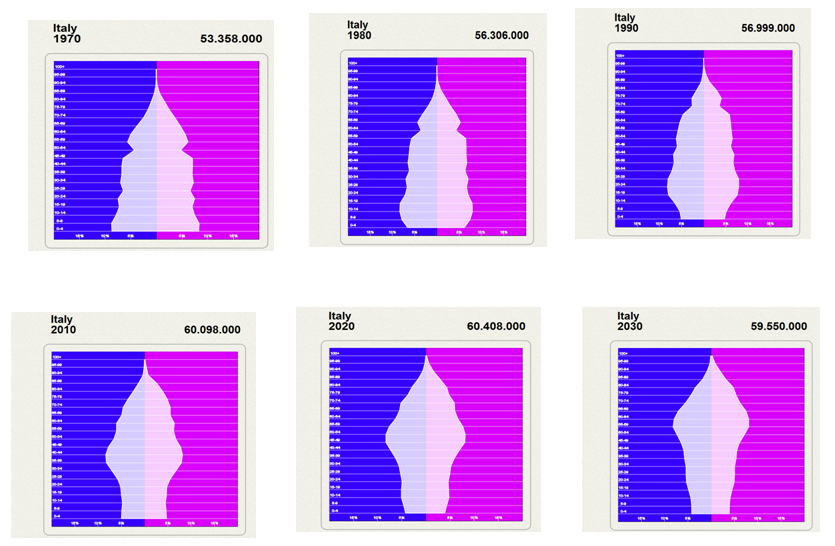

Secondly there is the problem of population ageing. The figures below show the transformation in Italy’s population pyramid between 1970 and 2030. In many ways Italy’s demography was at the most favourable point for economic growth (supply side) around 1990 (third figure top row) since the proportion of the total population in the working age group was at near its maximum, and the median age of the workforce was still relatively low. The point to get is that it isn’t simply the level of debt that is the problem, it is the level of debt in the context of the implicit liabilities (in terms of health and pensions) which such population ageing represents, and the reduced growth outlook that having declining and ageing populations represents. Europe’s leaders are essentially in denial on the extent of this problem, and are putting all their eggs in the “structural reforms to raise trend growth” basket.

{kind=link}

The third factor which has decisively changed things to the disadvantage of the ageing and indebted developed economies has been the rise of the new emerging economies. This has changed the perception of risk, against developed economies and in favour of emerging ones. It is unlikely that this trend will be reversed. So we have economies with excessive debt plus implicit liabilities who are going to be challenged to sustain growth rates similar in magnitude to those we have observed in the recent past, and it is this which makes the level of accumulated debt unsustainable and which makes it possible to speak of a developed world generalised debt crisis.

{kind=link}

But, despite this, those countries in the Euro area have a special problem. The common currency was created with a deficient institutional structure, which creates confusion over who is responsible for what. Viewed from outside the EU it almost seems as if you need a PhD in European studies to follow what is going on. In an era where the best policy if you have a financial product to take to market is “keep it simple” this hardly would seem to be a good idea.

{kind=link}

Cutting through all the foam and wrapping here, the key question is who is going to sign the cheques and who is going to pay? José Barroso and Herman Van Rompuy may make very nice photo images in Washington, but what exactly does there bank balance look like? So the key question market participants want to know, as President Barack Obama asked in Canberra recently, is who (or what) really stands behind the Euro. The answer so far has simply been a deafening silence.

{kind=link}

So what are the institutional solutions that are being toyed around with? The basic point to get is that this is all about money, who is to provide it, and who will take any losses there may be in the longer term. Basically there are three lines of attack on the table.

a) The ECB

b) The EFSF

c) Eurobonds

In fact the solution Europe’s leaders are likely to come up with involves some variant of all of these. As I suggested in my last piece, the ECB is desperate to go so far and no further. This is understandable given that no central bank likes the idea of finding itself having to show losses. Just how far the bank is prepared to go in order to avoid this is made plain from the rumour circulating this weekend that the IMF was readying up 600 billion Euros to lend to Italy. Just where the IMF was going to find the money was not explained by most of the sources, but thanks to a speedy translation from Edward Harrison at Credit Writedowns, we discover that it was another one of those cockamamie schemes whereby the ECB would actually lend the money, but the IMF would guarantee all the risk. Which simply begs the question; is there no one in Europe willing and able to guarantee the risk? And if not, why not? A stunning silence from Berlin.

{kind=link}

Under the circumstances it is hardly surprising that the IMF rapidly denied the report. It looks to me like someone, somewhere (someone with responsibilities for funding the IMF perhaps?) put their foot down, and firmly.

{kind=link}

Nonetheless it is quite likely that the ECB would be involved in some way, shape or form in any final attempt to rescue the Euro, possibly via some kind of security markets programme, and keeping the banking system supplied with liquidity.

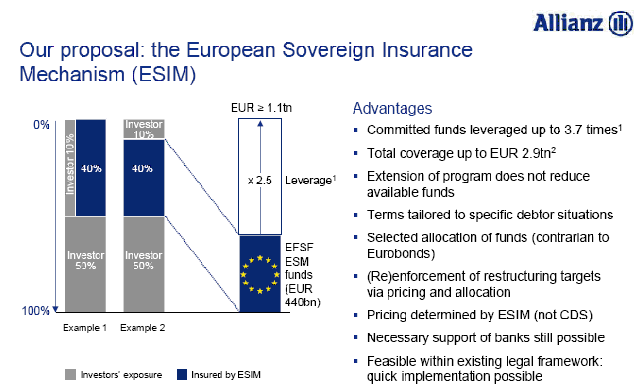

Which brings us to the EFSF, and here we do have some news. According to a report from Reuters, the documentation is all ready and prepared for the EU Finance Ministers meeting tomorrow on formulas for leveraging the EFSF.

{kind=link}

The formula being used for leveraging makes the current proposal look very similar to original Allianz Insurance proposal. The documents seen by Reuters specify that the EFSF could offer partial protection to investors buying a country’s bonds at a primary auction of around 20-30 percent of the principal amount of the bond, depending on market circumstances.The protection certificate would be detachable from the bond and could be traded separately, but the investor would have to hold bonds of the country before cashing it in. The certificate could be paid if the bond issuer triggers a credit event under the full definition of the International Swaps and Derivatives Association, but, of course, in the wake of the Greek private sector involvement swap investors are now nervous that any future restructuring of Eurozone bonds might be carried out in such a way as to not trigger an ISDA event, so it is not really clear how valuable this insurance actually is, or how it will be perceived by investors.

{kind=link}

But this isn’t the sum total of the problems faced by the EFSF approach, since according to CEO Klaus Regling, the original leveraging objective is now no longer attainable, due to the loss of market confidence. And with Italy alone rumoured to be looking for something like 600 billion Euros, the doable quantities from the EFSF now fall far short of what will be needed.

{kind=link}

Which brings us back to Eurobonds, which must be the last ditch recourse of someone or other. Markets certainly pricked up their ears last week when Angela Merkel issued those famous “now for now” words, but since that time we have simply had confusion. Actually the latest proposal on the bonds have come from the commission rather than the Paris-Berlin axis.

{kind=link}

Most observers have reached the conclusion that such bonds will at some point form part of Eurozone policy, but how, and when? The problem is that Angela Merkel is widely perceived as holding back in order to put pressure on recalcitrant periphery governments to bring their deficits into line. But you can only take brinksmanship so far before you risk having things blow up in your face, a point which is very well illustrated by the dilemmas facing Mario Monti’s new government. The problem is the timescale of debt reduction is one thing, and that of market confidence another.

{kind=link}

Germany is insisting that any advance towards Eurobonds is dependent on moves to what Angela Merkel calls a fiscal union. But by this she doesn’t mean the type of common treasury they have in the US, where stronger states help the weaker ones, what she means is common fiscal discipline, with powers from the centre to enforce.

{kind=link}

The only thing that can be said with any certainty about this situation is that it is very confused. One leaked proposal follows after another, while representatives of the EU Commission in Brussels can barely conceal their frustration with the “go it alone” approach being promoted in Paris and Berlin. Matters reached a head today with an article in the German newspaper Die Welt (allegedly based on a leak) asserting that Germany was preparing to issue “top tier” Eurobonds with a select group of other triple A countries.

{kind=link}

This could be read as a first step to a two tier Euro, which would at least be a step towards something. But it is too early to answer the question of whether it is, or whether it isn’t.

Readying Up For The Transition

In the meantime market participants are walking with their feet. Both banks and ratings agencies are sounding their loudest warnings yet that the euro area risks unravelling unless those responsible for decision taking intensify their efforts to stop the rot.

{kind=link}

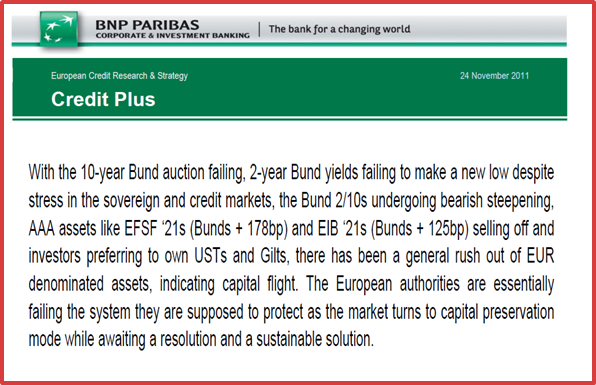

Just this morning I got a research report from Mehernosh Engineer and Gregory Venizelos of the PNB Paribas European Credit Research team.in which they argue that capital flight is already effectively taking place.

{kind=link}

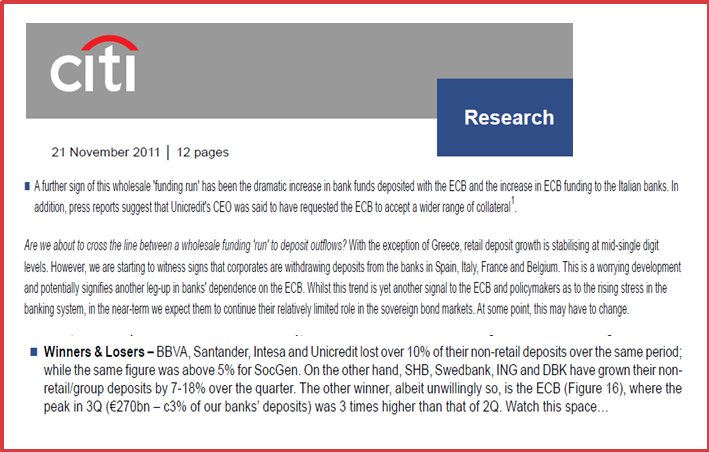

On the other hand Citi’s European Research Team are on “deposit watch”, and claim to see signs of deposit outflows from periphery to “core”, not retail deposits but corporate ones.

{kind=link}

Meanwhile over at Nomura they are already speculating on how assets will be denominated after break up:

{kind=link}

and giving advice to clients on the legal ins and outs of asset redenomination. Closing time in the gardens of the west anyone?

{kind=link}

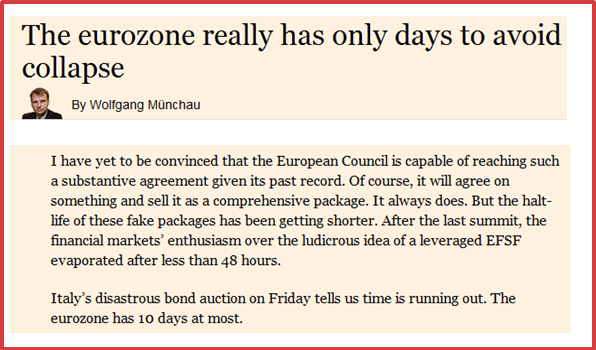

In this environment, it is hardly surprising that Wolfgang Munchau was his usual cheerful self in the FT this morning.

{kind=link}

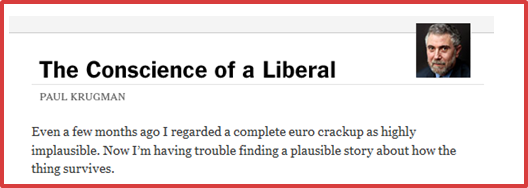

While perennial optimist Paul Krugman puts the situation really quite succinctly on his blog.

{kind=link}

Incidentally, if you can’t read any of the inserts, try clicking over them to get a magnified version.