By Andrew Lees, UBS

With the 40 year anniversary of Nixon defaulting on the US dollar commitment all over the press, and his policy of printing money to get out of the mess, I thought it was worth a quick reminder that, far from supporting economic growth like Nixon thought, the printing presses eroded growth. To begin with equities rallied heavily, up 30% from the abandonment of Bretton Woods until their highs in January 1973, but then started to fall in both nominal and real terms. In fact the S&P did not return to its January 1973 high in nominal terms until July 1980 (chart 1) and in real terms, not until 1987 just before the crash. It didn’t return to its 1960’s highs until early into the 1990’s – (chart 2). In real terms the S&P didn’t bottom until July 1982, 2 1/4 years after inflation had peaked.

{kind=link}

{kind=link}

So what? The US was suffering from a disinflationary shock due to the constraints that gold standard was imposing on it. Inflation had fallen from 6% plus in 1970 to just over 2% by the end of 1971/start of 1972 hence Nixon’s printing money exercise. To begin with the monetisation supported asset prices, both pushing equities aggressively higher and supporting lower Treasury yields, but eventually the monetisation became self defeating. The monetisation simply pushed commodity prices higher, offsetting the benefits of cheap money. Effectively the return per unit of additional monetisation collapsed – sound familiar?

A lot of people have said that equities should be supported by the recent fall in oil price, but of course that is nonsense as the oil price fall is simply due to reduced end demand; it is not because of the sudden productivity gain that has made more oil available at a lower price. Any return to monetisation therefore is likely to push oil prices back to their highs, choking off any fledgling recovery. Just as in the 1970’s therefore, the initial boost to equities (both nominal, but especially real) quickly faded. Monetisation instead shifted from asset price inflation to real inflation. Chart 3 overlays the M3 money supply growth (red line) against CPI and Treasury yields. In that first phase of monetisation mentioned above when equities rallied heavily, inflation and 10 year Treasury yields declined, but once the monetisation started having this self-defeating effect, equities slumped in real terms and bond yields started to soar.

{kind=link}

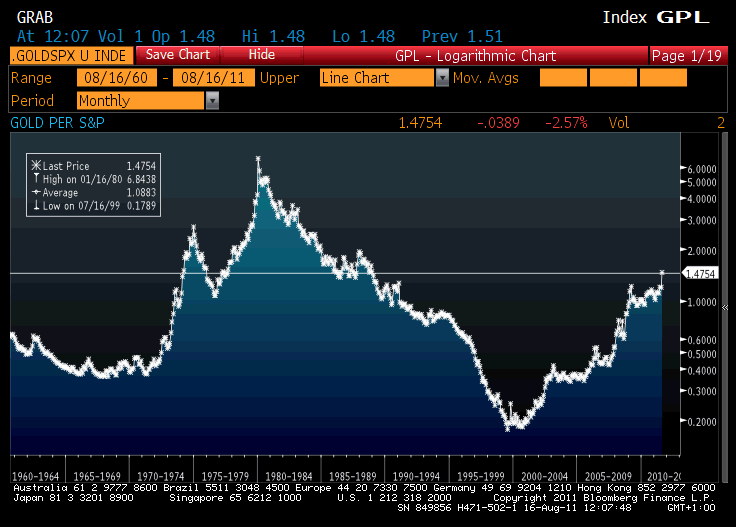

I would suggest that we must be nearing this watershed whereby inflation shifts from asset prices to real prices with obvious consequences. This is when commodity prices are likely to start accelerating upwards against equity prices – (see chart 4 for gold vs S&P which as you can see went exponential in the 1970’s when this watershed had happened) – as equities must de-rate. Unfortunately monetisation and Keynesian stimulus that people see as the solution now becomes the problem as the misallocation of capital has become simply too extreme.

{kind=link}