By Edward Hugh

What follows is simply a follow-up note to my earlier (Elephant in The Euro Room) piece on Italy. The decision by S&P to put Italian sovereign debt on negative outlook, and the subsequent announcement by Moody’s that it was considering a downgrade has been widely commented on by analysts, and it might be interesting to take a look at some of the views that have been advanced on either side of the argument (although for the detailed analysis see me earlier post). But first, a summary of the problem.

Chronicle Of A Crisis Long Foreseen

The first thing to be absolutely clear about is that this issue is not new. As FT Alphaville’s James Cotterill notes: “In the original ‘why the eurozone will break up’ papers of the 1990s and early 2000s, it was never ever high Greek deficits, or Irish (or Spanish) bank losses going on to public balance sheets that were forecast to destroy the single currency. It was always Italy. High-debt, low-growth, Italy”.

As the New York Times’ Landon Thomas noted in the Blog Prophet of Eurozone Doom article he wrote about my work, “Mr. Hugh’s demographic thesis is not airtight: in fact, it was Italy, not Greece, that attracted his early attacks. But Italy, perhaps because its overall debt level was already so high and its population was older, pursued a policy of greater fiscal rectitude than its neighbors and avoided a real estate bubble”.

Not airtight, but nearly-so it seems, since behind the short term focus on fiscal rectitude there lies the longer term preoccupation about solvency and debt. and here Italy (and eventually Japan) jump right back into the cockpit. As Landon mentions, Italy didn’t have a housing boom worthy of mention, so private debt didn’t surge during the first decade of the century, and during the crisis Finance Minister Tremonti pursued a policy of flying under the radar by keeping deficit spending low. But now short term deficit issues are waning, and longer term solvency questions are surfacing in the wake of the renewed Greek crisis. Thus, while historians of the future may well struggle to understand just how it was that a simple fiscal deficit bailout programme was so badly handled that Greek sovereign debt shot up from around 110% of GDP entering the crisis to around 170% by the end of the “rescue” period (and this without even having enjoyed a real housing bubble, i.e. with a private sector that was not massively in debt), the Italian case will raise few eyebrows, since every thinking economist had seen it coming for so long (Japan too, see my Italy blog here, here, here and here).

The Knife Edge Problem

The issue in hand is not too hard to grasp, even for those little tutored in economics. Italy’s gross public sector debt stood at approximately 120% of GDP in 2010. This is already too high, since it is significantly past the critical 100% level widely considered to be “the point of no return if not handled carefully” one. And how did it get there is the question we may want to ask. Was the high debt level due (as is the case in Ireland) to an emergency bank bailout, or was the country struggling (the Japan case) to fend off entrenched deflation?

No, there were none of these exceptional (or mitigating) circumstances to take into account, we are simply faced with a series of governments that were persistently (and mainly due to the burden of accumulated interest charges) paying out more than they were receiving in income, for over more than a decade, and turning a deaf ear to all the warnings being offered. It is always heartening to hear Mr Tremonti telling us that he will clamp down on administrative excesses and politicians salaries, or that he will wage a war on tax evasion, but really it would be interesting to know why he is always just on the point of doing something decisive to solve Italy’s revenue raising issues, but somehow never actually does.

As the Irish Finance Minister Michael Noonan said in an interview at the weekend:

“In Ireland, if you decide to tax bar stools and you give that instruction to the Revenue Commissioners [tax authorities] there will be a tax and there will a yield,” he said. “Their collection does not seem to be very good and it is a matter of speculation as to whether they can fulfil the commitments they are making or not,” he added.

He was talking about Greece, but Italy obviously suffers from similar tax collection issues when it comes to tracking down the informal economy.

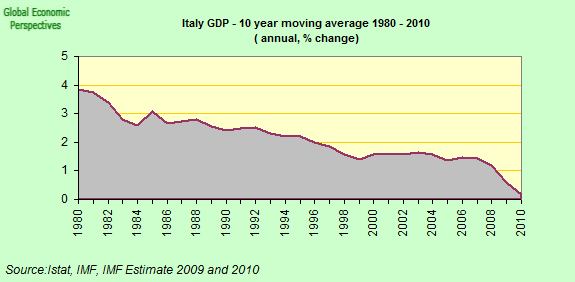

Basically, the Italian case is something of a hybrid one, since it is a bit like Portugal in its inherently low trend growth rate (significantly under 1% per annum) and like Greece in the tax execution problems it faces. In common with all the Mediterranean countries it also faces a great challenge when it comes to getting politicians to set aside party-politicking in order work together in the common national interest.

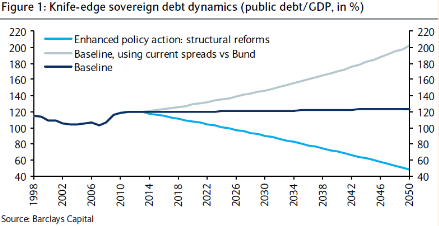

So Italy is now in the hot seat, since the focus of investor attention is moving beyond short term deficit control problems, and towards long term debt sustainability ones. Italy, as Barcap’s Antonio Garcia Pascual put it, is on the “knife edge”.

{kind=link}

And basically this isn’t going to be a story which needs a very long timeline to resolve, over the next few years either Italy’s public debt level will move downwards to 118%, 116%, 114% of GDP etc (and people start to breathe more easily) or it will carry on up towards 122%, 124% and 126% etc, in which case Italy will need to seek shelter in the new European crisis mechanism (if things hold together long enough for it to be put in place), and the debt will have to be restructured (the Euro was a costly little experiment, now wasn’t it?). This is the basic gist of the argument behind Moody’s recent announcement that they were thinking of downgrading the Italian Sovereign rating, since the risks that Italy is going to need restructuring are rising.

Of course what really put the cat among the Italian pigeons, was Moody’s subsequent announcement that it was putting 16 Italian banks on rating watch negative for possible downgrade due to their exposure to the Italian sovereign. Thus, in the blink of a press release was put to the test and found wanting a nice little theory that held that Italian public debt wasn’t such a big deal, since it is mainly held by Italian banks. Exactly, and precisely for this reason it is a big deal for Italian banks, at least two of which could be considered systemic. Hence the debacle on Friday on the Italian bourses.

So as Garcia Pascual says, Italy is sitting on a knife edge, or looking out over a precipice. Really there are only three things that matter – the rate of GDP growth, the rate of inflation, and the level of interest payments. Unfortunately for Italy, the first two of these are falling at the moment (see this piece on current risks to Italian growth), while the third is rising. Just last Friday, following the news that Moody’s were reviewing the rating of the Italian banks, the spread on Italian 10 year bonds over equivalent German bunds hit 213 basis points, a Euro era record.

As I have already stressed in the “Elephant In The Euro Room” piece, it is nominal GDP (or the sum total of real GDP plus inflation) that matters, and on existing interest rates the sum total of these two needs to be on average around 3% simply to maintain the debt were it is. Looking at the growth position, and the waning inflation as the global economy turns down, this level is unlikely to be achieved in 2011, so we will have our first evidence of “slippage”. The longer term problem is that these two variables, in the case of an economy like the Italian one, work in opposite directions, since (given that Italy’s economy is by and large export dependent for growth), in a currency peg structure more inflation means less peer-economy competitiveness, which means less growth. As Goldman Sachs economist Kevin Daly put it in a recent report:

“For countries attempting to address these twin imbalances (government debt and current account deficit) within a currency union, there is a ‘Catch 22’ situation: competitiveness can only be regained via real exchange rate adjustment (i.e., by running lower inflation than the Euro-zone average). However, in order to boost public sector finances, economies need stronger nominal GDP growth and, thus, relatively low inflation (or deflation) has the effect of exacerbating the public-sector deficit problem. In other words, it is difficult to address one imbalance without exacerbating the other, and vice versa”.

So that’s the first part of the problem. But there is more. If we go back to Garcia Pascual’s original baseline scenario chart, he assumed that the spread on Italian government debt would be about 100 basis points, in which case a nominal GDP growth rate of just under 3% and a budget deficit of just over 3% would stabilise Italian debt at around 120% of GDP. But the Italian spread just moved over 200 basis points, and in a post Greece-restructuring-event environment it is likely to go up, and not down, in which case, instead of stabilising, the debt will veer upwards, just on the increased country interest risk element alone.

Then again, you might say, Italy could go for a serious austerity programme (of the Estonian “let’s show these guys we’re serious” type), going well under the 3% deficit target, and even trying to obtain a general budget surplus. Surely this would bring the debt down, and increase investor confidence (thus bringing the spread down). Well, yes, it might raise confidence but look what has just happened to Greece and is happening to Portugal now. Apply more austerity to a fundamentally uncompetitive economy and you are liable to seriously reduce growth, and even send the country into a quite deep recession (Italy is, in my opinion, already near slight contraction). On top of that you have the danger that along with the austerity you will introduce another “indignados” movement, something which is more or less predictable in Italy’s deeply divided political environment. At which point the Euro would surely be “rockin and rollin”.

All of which takes us back to the structural reforms issue as the great white hope on which so many people stake their bets that Italy will see it though.

Of course, whether markets will continue to provide Italy with sufficient financing depends not only on macroeconomic and fiscal fundamentals, but also on factors that are outside of Italy’s control (such as investors’ appetite for European debt). The country’s outstanding level of public debt is high and fiscal discipline in the recent past had been preceded by less controlled public spending. And although economic activity in Italy has been sluggish, we continue to believe that the government’s stated goal of continuing to impose fiscal discipline will suffice to keep the country on a sustainable debt path.

Natacha Valla, Goldman Sachs

“In an environment of low nominal growth, Italy‟s high interest payments (of around 5% of GDP) will continue to weigh on debt dynamics. However, we expect the primary balance to turn into a surplus from 2011 onwards, which should help to stabilise the debt to around 120% of GDP over the next two years.Having said that, determined action to implement growth-enhancing reforms and further fiscal consolidation to reduce the structurally high expenditure components is essential”.

Lavinia Santovetti, Nomura

We agree with S&P, as we stated several times in Focus Europe, that Italy needs to intensify its efforts on structural reforms to boost its disappointing GDP growth. It is important that the strength of the private sector does not become an excuse for complacency. Productivity-enhancing reforms would increase the likelihood of meeting the post-2013 Government’s fiscal objectives……Given that fiscal consolidation remains a fairly consensus strategy across the main parties and the tangible strength of the Italian private sector, we remain positive about the stability of the Italian public debt. The key risk in the short term is a political mistake in dealing with the European peripherals.

Marco Stringa, Deutsche Bank

{kind=link}

Of course, it is always a worthy option to live in hope, but looking at the evolution in Italian trend growth over recent decades, mightn’t we do better all assembling in the Piazza San Marco one afternoon and getting down on of knees for half an hour, just to show we were really earnest in our hope.

The key thing about all these ardently solicited structural reforms is that they need time both to implement and to work, and time (as I explained above) is just what Italy now hasn’t got a lot of at this point (debt to GDP will either go up, or come down, and if it starts to go up…..).

Back in June 2005 (when there was still plenty of time) the ECB hosted a conference with the interesting title “What effects is EMU having on the euro area and its member countries?” Among the papers present was one from two OECD economists (Romain Duval and Jørgen Elmeskov). The title of the paper was “The Effects Of EMU On Structural Reforms In Labour And Product Markets“, and the key finding was that:

“As concerns the role of the monetary policy regime, the absence of monetary policy autonomy seems to be associated with lower structural reform activity in large, more closed economies”.

Put in plain English, in a country like Italy, monetary union had slowed down rather than speeding up the much needed structural change. At the time of publication the paper caused quite a stir, but, like so many useful things, was soon forgotten. As if foreseeing the paper’s fate, the authors close with the following lament: “It would be sad if structural reform were eventually driven by a factor that empirically is strongly correlated with reform: crisis.”

Life it seems is inherently sad, and here we are now 6 years later, in the midst of the correlate they foresaw as their downside scenario, and still battling with all the same old problems, where the only light we can see at the end of the tunnel is that of the next express train hurtling down the track towards us.

This post first appeared on my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.